Advertisement

Finding a business that has the potential to grow substantially is not easy, but it is possible if we look at a few key financial metrics. One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. Speaking of which, we noticed some great changes in HLE Glascoat's (NSE:HLEGLAS) returns on capital, so let's have a look.

What Is Return On Capital Employed (ROCE)?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. The formula for this calculation on HLE Glascoat is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

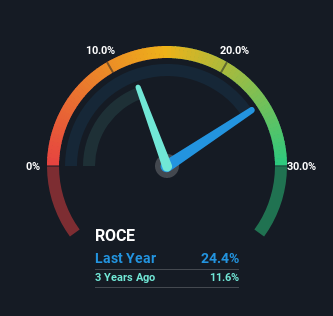

0.24 = ₹1.0b ÷ (₹7.6b - ₹3.4b) (Based on the trailing twelve months to June 2022).

So, HLE Glascoat has an ROCE of 24%. In absolute terms that's a great return and it's even better than the Machinery industry average of 14%.

See our latest analysis for HLE Glascoat

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you'd like to look at how HLE Glascoat has performed in the past in other metrics, you can view this free graph of past earnings, revenue and cash flow.

What Does the ROCE Trend For HLE Glascoat Tell Us?

HLE Glascoat is displaying some positive trends. Over the last five years, returns on capital employed have risen substantially to 24%. The amount of capital employed has increased too, by 610%. So we're very much inspired by what we're seeing at HLE Glascoat thanks to its ability to profitably reinvest capital.

On a side note, HLE Glascoat's current liabilities are still rather high at 45% of total assets. This can bring about some risks because the company is basically operating with a rather large reliance on its suppliers or other sorts of short-term creditors. Ideally we'd like to see this reduce as that would mean fewer obligations bearing risks.

The Key Takeaway

All in all, it's terrific to see that HLE Glascoat is reaping the rewards from prior investments and is growing its capital base. Astute investors may have an opportunity here because the stock has declined 18% in the last year. With that in mind, we believe the promising trends warrant this stock for further investigation.

One more thing to note, we've identified 1 warning sign with HLE Glascoat and understanding this should be part of your investment process.

HLE Glascoat is not the only stock earning high returns. If you'd like to see more, check out our free list of companies earning high returns on equity with solid fundamentals.

Valuation is complex, but we're here to simplify it.

Discover if HLE Glascoat might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:HLEGLAS

HLE Glascoat

Manufactures and sells carbon steel glass lined equipment in India and internationally.

Proven track record with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|36.2% undervalued

JO

Community Contributor

Occidental Petroleum is set to achieve a 16% profit margin improvement

Fair Value US$55.05|18.7% undervalued

DZ

Community Contributor

Argan's Revenue Set to Soar with a 13.31% Growth in the Coming Decade

Fair Value US$284.68|22.0% undervalued

KE

Community Contributor

EU#1 - From German Startup to EU’s Biggest Company

Fair Value €248.62|5.0% overvalued

TO

Community Contributor