Advertisement

- India

- /

- Auto Components

- /

- NSEI:GRPLTD

One GRP Limited (NSE:GRPLTD) Analyst Just Made A Major Cut To Next Year's Estimates

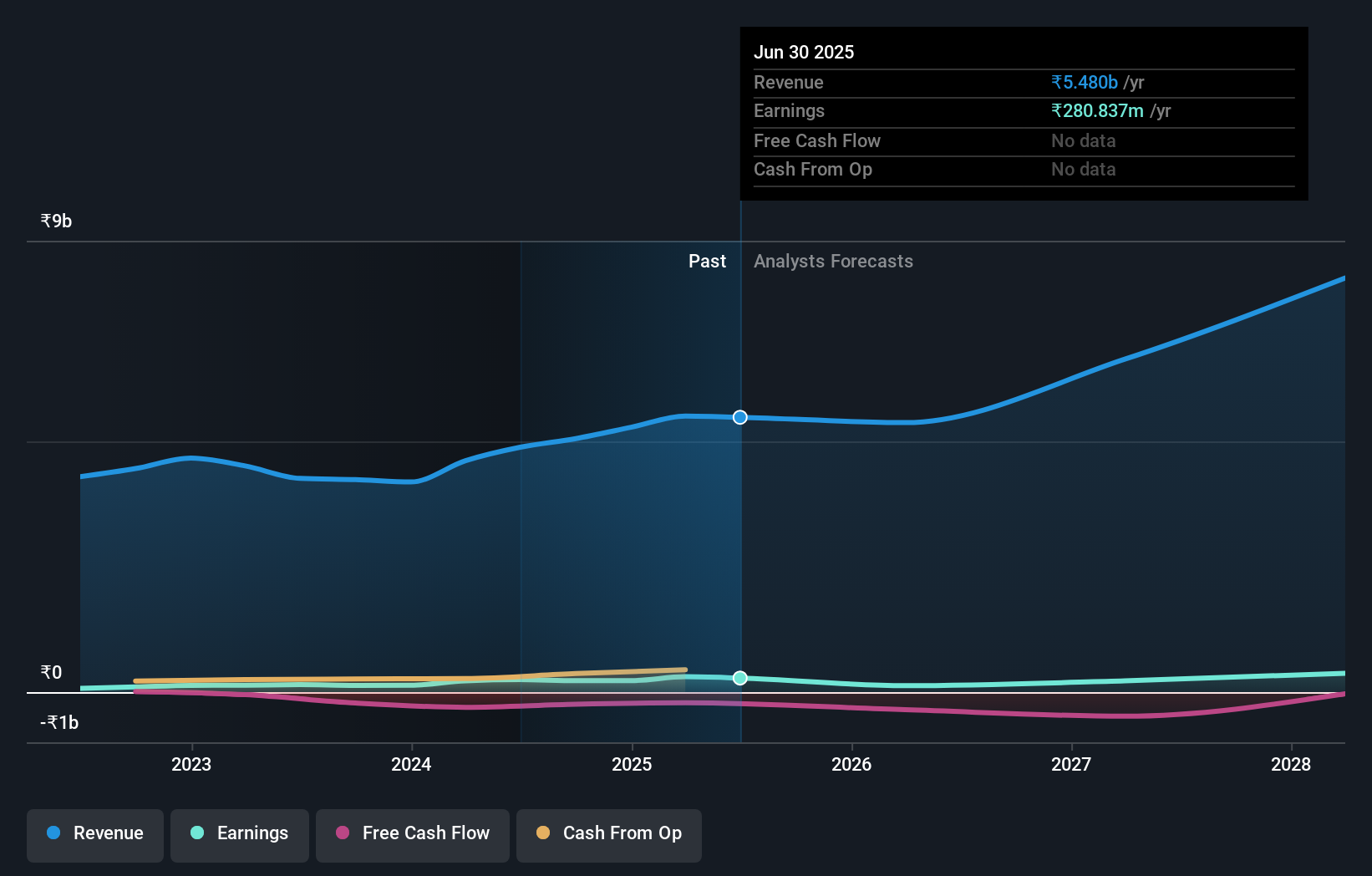

One thing we could say about the covering analyst on GRP Limited (NSE:GRPLTD) - they aren't optimistic, having just made a major negative revision to their near-term (statutory) forecasts for the organization. Both revenue and earnings per share (EPS) forecasts went under the knife, suggesting the analyst has soured majorly on the business.

Following the latest downgrade, GRP's one analyst currently expects revenues in 2026 to be ₹5.4b, approximately in line with the last 12 months. Statutory earnings per share are anticipated to dive 54% to ₹24.20 in the same period. Previously, the analyst had been modelling revenues of ₹6.6b and earnings per share (EPS) of ₹28.10 in 2026. Indeed, we can see that the analyst is a lot more bearish about GRP's prospects, administering a substantial drop in revenue estimates and slashing their EPS estimates to boot.

Check out our latest analysis for GRP

The consensus price target fell 39% to ₹2,131, with the weaker earnings outlook clearly leading analyst valuation estimates.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the GRP's past performance and to peers in the same industry. These estimates imply that sales are expected to slow, with a forecast annualised revenue decline of 1.9% by the end of 2026. This indicates a significant reduction from annual growth of 13% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 9.7% annually for the foreseeable future. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - GRP is expected to lag the wider industry.

The Bottom Line

The most important thing to take away is that the analyst cut their earnings per share estimates, expecting a clear decline in business conditions. Regrettably, they also downgraded their revenue estimates, and the latest forecasts imply the business will grow sales slower than the wider market. With a serious cut to this year's expectations and a falling price target, we wouldn't be surprised if investors were becoming wary of GRP.

Unfortunately, the earnings downgrade - if accurate - may also place pressure on GRP's mountain of debt, which could lead to some belt tightening for shareholders. To see more of our financial analysis, you can click through to our free platform to learn more about its balance sheet and specific concerns we've identified.

We also provide an overview of the GRP Board and CEO remuneration and length of tenure at the company, and whether insiders have been buying the stock, here.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:GRPLTD

GRP

Manufactures and sells reclaimed rubber products for tyre and non-tyre rubber goods in India and internationally.

Adequate balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor