Advertisement

Here's Why Bajaj Auto (NSE:BAJAJ-AUTO) Can Manage Its Debt Responsibly

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Bajaj Auto Limited (NSE:BAJAJ-AUTO) does carry debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

What Is Bajaj Auto's Debt?

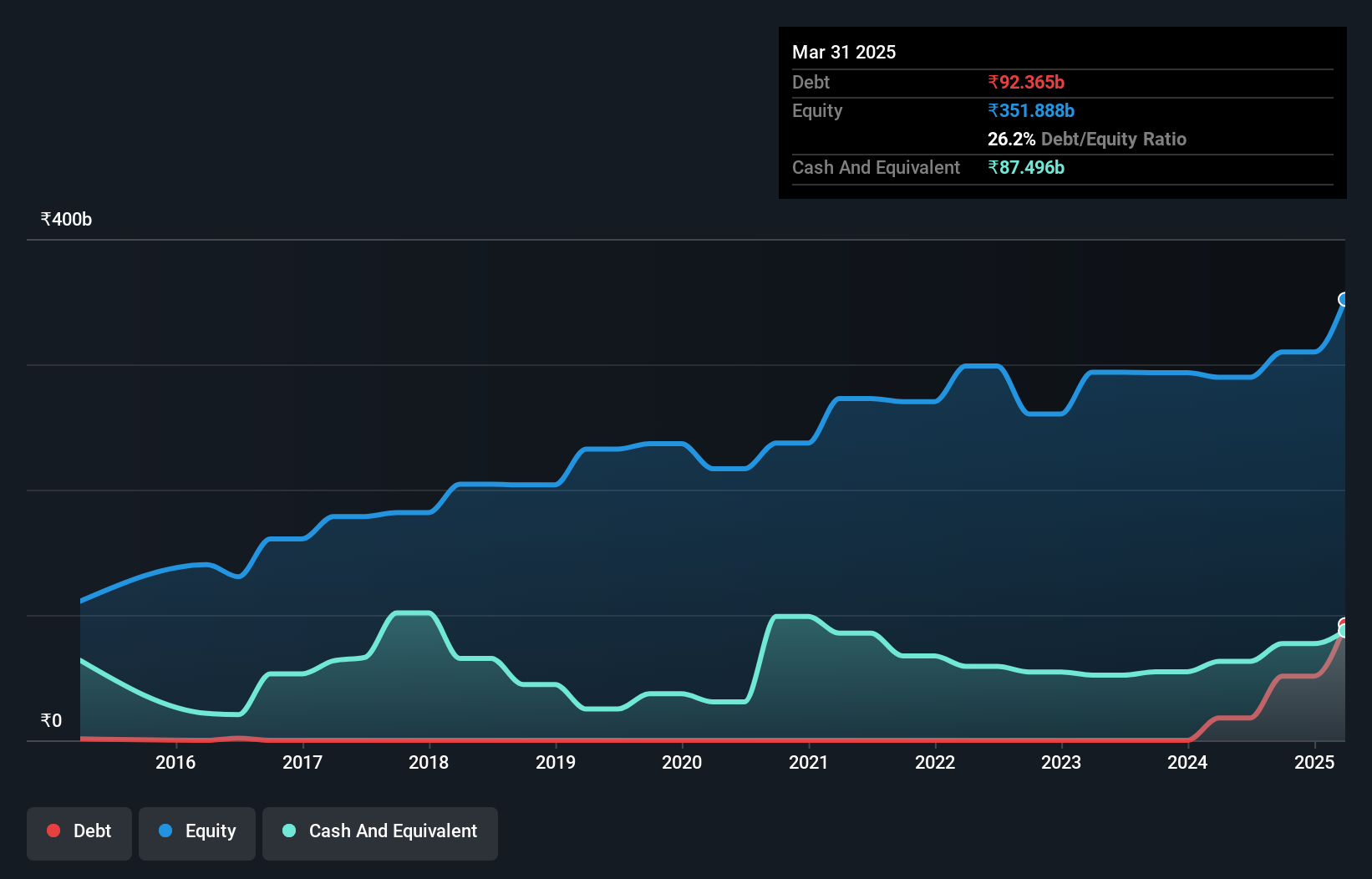

You can click the graphic below for the historical numbers, but it shows that as of March 2025 Bajaj Auto had ₹92.4b of debt, an increase on ₹17.9b, over one year. However, because it has a cash reserve of ₹87.5b, its net debt is less, at about ₹4.87b.

How Strong Is Bajaj Auto's Balance Sheet?

We can see from the most recent balance sheet that Bajaj Auto had liabilities of ₹115.8b falling due within a year, and liabilities of ₹74.3b due beyond that. On the other hand, it had cash of ₹87.5b and ₹55.9b worth of receivables due within a year. So it has liabilities totalling ₹46.7b more than its cash and near-term receivables, combined.

Having regard to Bajaj Auto's size, it seems that its liquid assets are well balanced with its total liabilities. So while it's hard to imagine that the ₹2.34t company is struggling for cash, we still think it's worth monitoring its balance sheet. But either way, Bajaj Auto has virtually no net debt, so it's fair to say it does not have a heavy debt load!

View our latest analysis for Bajaj Auto

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Bajaj Auto has very little debt (net of cash), and boasts a debt to EBITDA ratio of 0.041 and EBIT of 29.6 times the interest expense. So relative to past earnings, the debt load seems trivial. Also good is that Bajaj Auto grew its EBIT at 17% over the last year, further increasing its ability to manage debt. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Bajaj Auto's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Looking at the most recent three years, Bajaj Auto recorded free cash flow of 27% of its EBIT, which is weaker than we'd expect. That weak cash conversion makes it more difficult to handle indebtedness.

Our View

The good news is that Bajaj Auto's demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. But truth be told we feel its conversion of EBIT to free cash flow does undermine this impression a bit. Taking all this data into account, it seems to us that Bajaj Auto takes a pretty sensible approach to debt. That means they are taking on a bit more risk, in the hope of boosting shareholder returns. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For example Bajaj Auto has 2 warning signs (and 1 which is a bit unpleasant) we think you should know about.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we're here to simplify it.

Discover if Bajaj Auto might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:BAJAJ-AUTO

Bajaj Auto

Engages in the development, manufacture, and distribution of automobiles in India and internationally.

Proven track record average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor