Advertisement

- India

- /

- Auto Components

- /

- NSEI:ASAL

Even With A 36% Surge, Cautious Investors Are Not Rewarding Automotive Stampings and Assemblies Limited's (NSE:ASAL) Performance Completely

Automotive Stampings and Assemblies Limited (NSE:ASAL) shareholders have had their patience rewarded with a 36% share price jump in the last month. The last month tops off a massive increase of 117% in the last year.

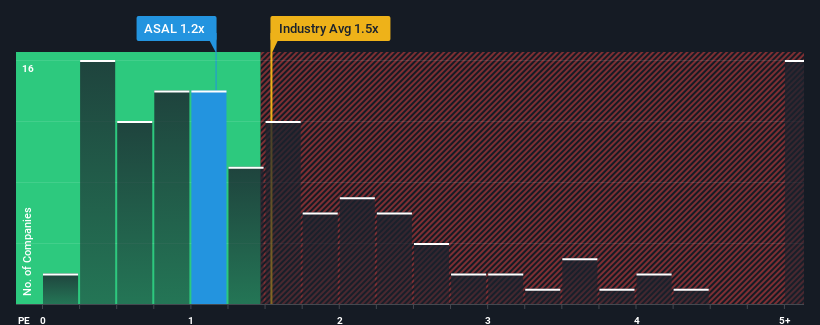

In spite of the firm bounce in price, you could still be forgiven for feeling indifferent about Automotive Stampings and Assemblies' P/S ratio of 1.2x, since the median price-to-sales (or "P/S") ratio for the Auto Components industry in India is also close to 1.5x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

View our latest analysis for Automotive Stampings and Assemblies

What Does Automotive Stampings and Assemblies' P/S Mean For Shareholders?

Revenue has risen at a steady rate over the last year for Automotive Stampings and Assemblies, which is generally not a bad outcome. Perhaps the expectation moving forward is that the revenue growth will track in line with the wider industry for the near term, which has kept the P/S subdued. If not, then at least existing shareholders probably aren't too pessimistic about the future direction of the share price.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Automotive Stampings and Assemblies' earnings, revenue and cash flow.Is There Some Revenue Growth Forecasted For Automotive Stampings and Assemblies?

Automotive Stampings and Assemblies' P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

Taking a look back first, we see that the company managed to grow revenues by a handy 4.4% last year. This was backed up an excellent period prior to see revenue up by 212% in total over the last three years. So we can start by confirming that the company has done a great job of growing revenues over that time.

When compared to the industry's one-year growth forecast of 10%, the most recent medium-term revenue trajectory is noticeably more alluring

With this information, we find it interesting that Automotive Stampings and Assemblies is trading at a fairly similar P/S compared to the industry. It may be that most investors are not convinced the company can maintain its recent growth rates.

What We Can Learn From Automotive Stampings and Assemblies' P/S?

Automotive Stampings and Assemblies' stock has a lot of momentum behind it lately, which has brought its P/S level with the rest of the industry. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

We didn't quite envision Automotive Stampings and Assemblies' P/S sitting in line with the wider industry, considering the revenue growth over the last three-year is higher than the current industry outlook. There could be some unobserved threats to revenue preventing the P/S ratio from matching this positive performance. While recent revenue trends over the past medium-term suggest that the risk of a price decline is low, investors appear to see the likelihood of revenue fluctuations in the future.

Plus, you should also learn about these 4 warning signs we've spotted with Automotive Stampings and Assemblies (including 2 which are potentially serious).

If these risks are making you reconsider your opinion on Automotive Stampings and Assemblies, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:ASAL

Automotive Stampings and Assemblies

Designs, develops, manufactures, assembles, and sells sheet metal stampings, welded assemblies, and modules for passenger and commercial vehicles, and tractors in India.

Low risk with imperfect balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|24.9% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.3% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.5% undervalued

DA

Community Contributor