Advertisement

- Israel

- /

- Real Estate

- /

- TASE:SRFT

Zvi Sarfati & Sons Investments & Constructions (TLV:SRFT) Has A Somewhat Strained Balance Sheet

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Zvi Sarfati & Sons Investments & Constructions Ltd. (TLV:SRFT) does have debt on its balance sheet. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Zvi Sarfati & Sons Investments & Constructions

How Much Debt Does Zvi Sarfati & Sons Investments & Constructions Carry?

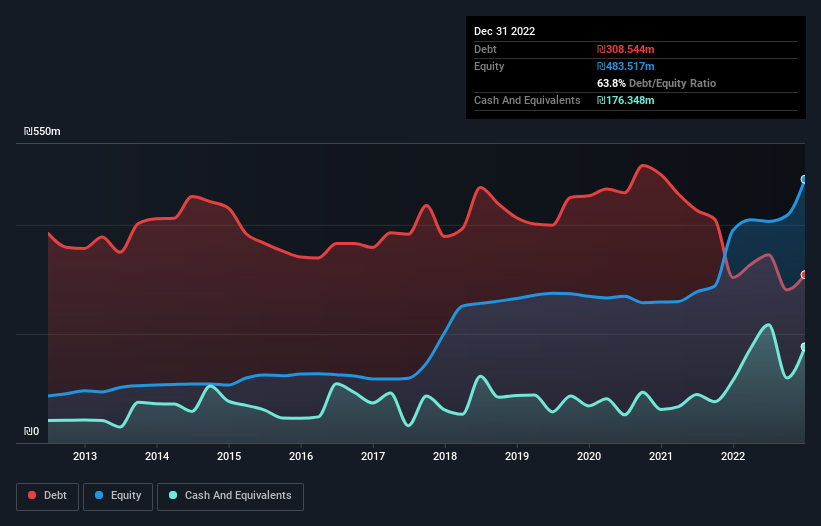

The chart below, which you can click on for greater detail, shows that Zvi Sarfati & Sons Investments & Constructions had ₪308.5m in debt in December 2022; about the same as the year before. However, because it has a cash reserve of ₪176.3m, its net debt is less, at about ₪132.2m.

How Strong Is Zvi Sarfati & Sons Investments & Constructions' Balance Sheet?

According to the last reported balance sheet, Zvi Sarfati & Sons Investments & Constructions had liabilities of ₪659.8m due within 12 months, and liabilities of ₪83.1m due beyond 12 months. On the other hand, it had cash of ₪176.3m and ₪89.9m worth of receivables due within a year. So it has liabilities totalling ₪476.6m more than its cash and near-term receivables, combined.

When you consider that this deficiency exceeds the company's ₪443.8m market capitalization, you might well be inclined to review the balance sheet intently. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Zvi Sarfati & Sons Investments & Constructions has a low net debt to EBITDA ratio of only 0.78. And its EBIT easily covers its interest expense, being 11.5 times the size. So we're pretty relaxed about its super-conservative use of debt. But the bad news is that Zvi Sarfati & Sons Investments & Constructions has seen its EBIT plunge 13% in the last twelve months. We think hat kind of performance, if repeated frequently, could well lead to difficulties for the stock. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Zvi Sarfati & Sons Investments & Constructions's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we always check how much of that EBIT is translated into free cash flow. Happily for any shareholders, Zvi Sarfati & Sons Investments & Constructions actually produced more free cash flow than EBIT over the last three years. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

We feel some trepidation about Zvi Sarfati & Sons Investments & Constructions's difficulty EBIT growth rate, but we've got positives to focus on, too. For example, its conversion of EBIT to free cash flow and interest cover give us some confidence in its ability to manage its debt. We think that Zvi Sarfati & Sons Investments & Constructions's debt does make it a bit risky, after considering the aforementioned data points together. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. Above most other metrics, we think its important to track how fast earnings per share is growing, if at all. If you've also come to that realization, you're in luck, because today you can view this interactive graph of Zvi Sarfati & Sons Investments & Constructions's earnings per share history for free.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if Zvi Sarfati & Sons Investments & Constructions might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TASE:SRFT

Zvi Sarfati & Sons Investments & Constructions

Through its subsidiaries, constructs and sells residential projects, apartments, and commercial spaces and offices in Israel.

Mediocre balance sheet with low risk.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor