Advertisement

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Neto M.E Holdings Ltd (TLV:NTO) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Neto M.E Holdings

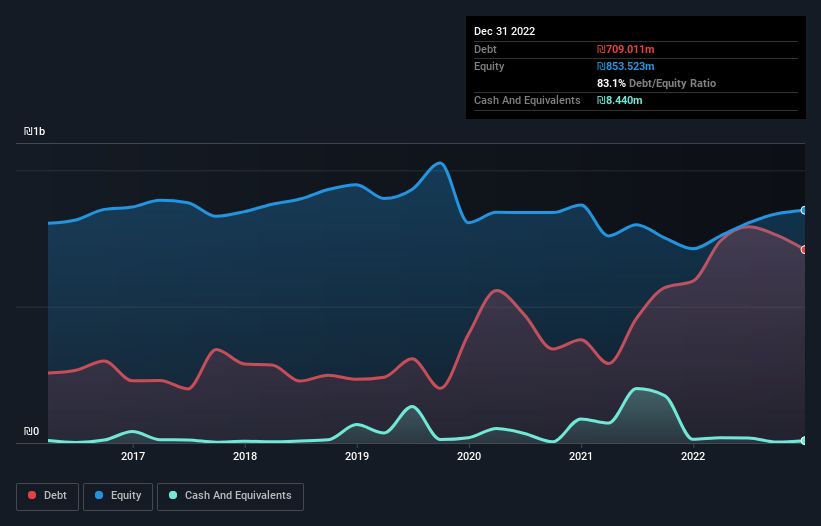

What Is Neto M.E Holdings's Net Debt?

You can click the graphic below for the historical numbers, but it shows that as of December 2022 Neto M.E Holdings had ₪709.0m of debt, an increase on ₪593.2m, over one year. And it doesn't have much cash, so its net debt is about the same.

How Strong Is Neto M.E Holdings' Balance Sheet?

According to the last reported balance sheet, Neto M.E Holdings had liabilities of ₪971.5m due within 12 months, and liabilities of ₪92.9m due beyond 12 months. On the other hand, it had cash of ₪8.44m and ₪1.10b worth of receivables due within a year. So it actually has ₪44.6m more liquid assets than total liabilities.

This short term liquidity is a sign that Neto M.E Holdings could probably pay off its debt with ease, as its balance sheet is far from stretched.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Neto M.E Holdings's debt is 3.1 times its EBITDA, and its EBIT cover its interest expense 6.8 times over. Taken together this implies that, while we wouldn't want to see debt levels rise, we think it can handle its current leverage. Shareholders should be aware that Neto M.E Holdings's EBIT was down 27% last year. If that earnings trend continues then paying off its debt will be about as easy as herding cats on to a roller coaster. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Neto M.E Holdings will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we always check how much of that EBIT is translated into free cash flow. Over the last three years, Neto M.E Holdings reported free cash flow worth 6.4% of its EBIT, which is really quite low. That limp level of cash conversion undermines its ability to manage and pay down debt.

Our View

Neto M.E Holdings's EBIT growth rate was a real negative on this analysis, although the other factors we considered cast it in a significantly better light. For example, its level of total liabilities is relatively strong. Taking the abovementioned factors together we do think Neto M.E Holdings's debt poses some risks to the business. So while that leverage does boost returns on equity, we wouldn't really want to see it increase from here. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 4 warning signs for Neto M.E Holdings you should be aware of, and 2 of them are a bit unpleasant.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Valuation is complex, but we're here to simplify it.

Discover if Neto M.E Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TASE:NTO

Neto M.E Holdings

Produces, processes, imports, markets, and distributes a range of food products in Israel.

Flawless balance sheet with acceptable track record.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor