Advertisement

- Israel

- /

- Oil and Gas

- /

- TASE:TOEN

We Wouldn't Be Too Quick To Buy Tomer Energy Royalties (2012) Ltd (TLV:TOEN) Before It Goes Ex-Dividend

Tomer Energy Royalties (2012) Ltd (TLV:TOEN) stock is about to trade ex-dividend in 3 days. The ex-dividend date is usually set to be one business day before the record date which is the cut-off date on which you must be present on the company's books as a shareholder in order to receive the dividend. It is important to be aware of the ex-dividend date because any trade on the stock needs to have been settled on or before the record date. In other words, investors can purchase Tomer Energy Royalties (2012)'s shares before the 29th of October in order to be eligible for the dividend, which will be paid on the 7th of November.

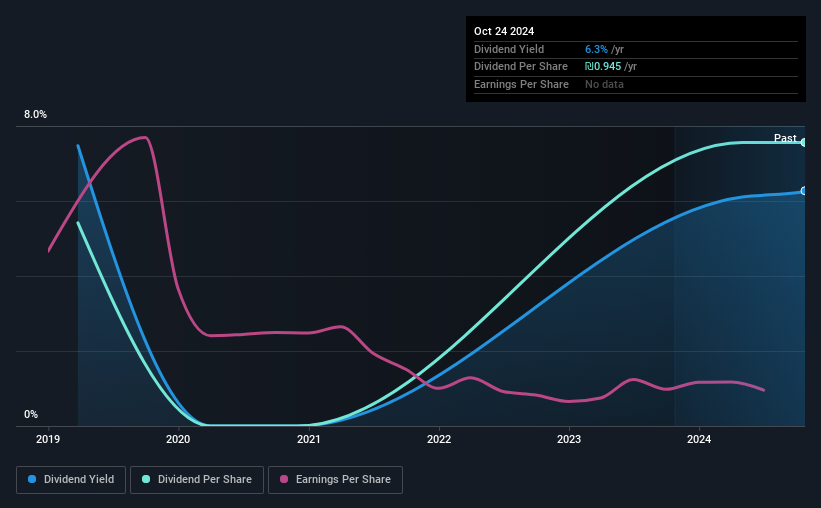

The company's upcoming dividend is US$0.12499 a share, following on from the last 12 months, when the company distributed a total of US$0.25 per share to shareholders. Last year's total dividend payments show that Tomer Energy Royalties (2012) has a trailing yield of 6.3% on the current share price of ₪15.07. We love seeing companies pay a dividend, but it's also important to be sure that laying the golden eggs isn't going to kill our golden goose! That's why we should always check whether the dividend payments appear sustainable, and if the company is growing.

View our latest analysis for Tomer Energy Royalties (2012)

Dividends are usually paid out of company profits, so if a company pays out more than it earned then its dividend is usually at greater risk of being cut. Tomer Energy Royalties (2012) distributed an unsustainably high 132% of its profit as dividends to shareholders last year. Without extenuating circumstances, we'd consider the dividend at risk of a cut. Yet cash flows are even more important than profits for assessing a dividend, so we need to see if the company generated enough cash to pay its distribution. Tomer Energy Royalties (2012) paid a dividend despite reporting negative free cash flow last year. That's typically a bad combination and - if this were more than a one-off - not sustainable.

It's disappointing to see that the dividend was not covered by profits, but cash is more important from a dividend sustainability perspective, and Tomer Energy Royalties (2012) fortunately did generate enough cash to fund its dividend. If executives were to continue paying more in dividends than the company reported in profits, we'd view this as a warning sign. Extraordinarily few companies are capable of persistently paying a dividend that is greater than their profits.

Click here to see how much of its profit Tomer Energy Royalties (2012) paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

When earnings decline, dividend companies become much harder to analyse and own safely. If business enters a downturn and the dividend is cut, the company could see its value fall precipitously. Tomer Energy Royalties (2012)'s earnings per share have fallen at approximately 27% a year over the previous five years. When earnings per share fall, the maximum amount of dividends that can be paid also falls.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. In the past six years, Tomer Energy Royalties (2012) has increased its dividend at approximately 5.7% a year on average. The only way to pay higher dividends when earnings are shrinking is either to pay out a larger percentage of profits, spend cash from the balance sheet, or borrow the money. Tomer Energy Royalties (2012) is already paying out 132% of its profits, and with shrinking earnings we think it's unlikely that this dividend will grow quickly in the future.

Final Takeaway

Is Tomer Energy Royalties (2012) an attractive dividend stock, or better left on the shelf? It's looking like an unattractive opportunity, with its earnings per share declining, while, paying out an uncomfortably high percentage of both its profits (132%) and cash flow as dividends. Unless there are grounds to believe a turnaround is imminent, this is one of the least attractive dividend stocks under this analysis. Overall it doesn't look like the most suitable dividend stock for a long-term buy and hold investor.

Although, if you're still interested in Tomer Energy Royalties (2012) and want to know more, you'll find it very useful to know what risks this stock faces. To help with this, we've discovered 4 warning signs for Tomer Energy Royalties (2012) (3 are a bit concerning!) that you ought to be aware of before buying the shares.

A common investing mistake is buying the first interesting stock you see. Here you can find a full list of high-yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Tomer Energy Royalties (2012) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TASE:TOEN

Tomer Energy Royalties (2012)

A special-purpose yield company, holds the right to receive overriding royalties in respect of oil and/or gas, and/or other valuable materials derived from the shares of various oil and gas companies and entities in Israel.

Slight second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|35.9% undervalued

JO

Community Contributor

Occidental Petroleum is set to achieve a 16% profit margin improvement

Fair Value US$55.05|15.6% undervalued

DZ

Community Contributor

Argan's Revenue Set to Soar with a 13.31% Growth in the Coming Decade

Fair Value US$284.68|23.4% undervalued

KE

Community Contributor

EU#1 - From German Startup to EU’s Biggest Company

Fair Value €248.62|2.5% overvalued

TO

Community Contributor