Advertisement

- Israel

- /

- Capital Markets

- /

- TASE:MRIN

Y.D. More Investments (TASE:MRIN) Margin Expansion Reinforces Bullish Narrative Despite Elevated Valuation

Simply Wall St

Reviewed by Simply Wall St

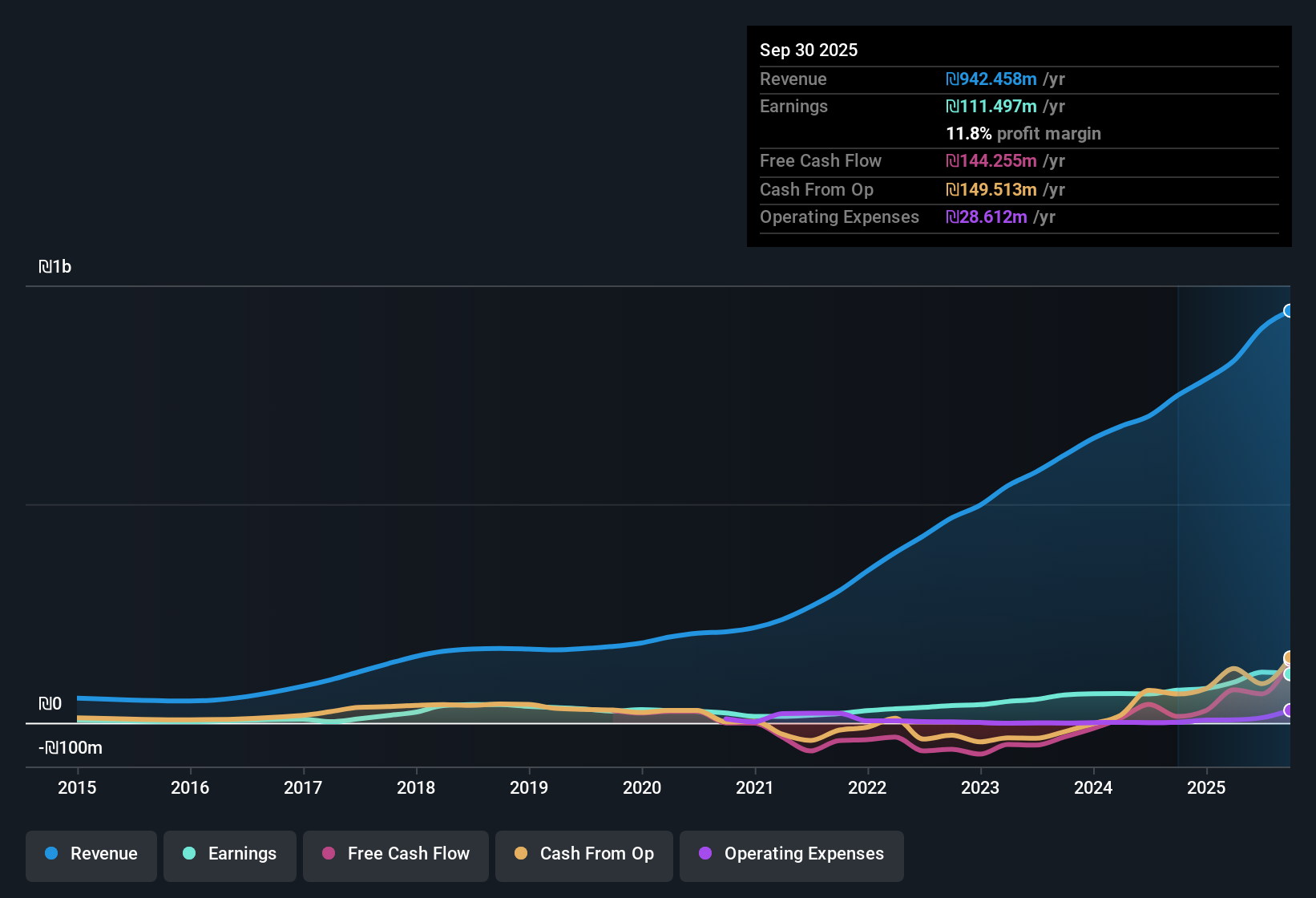

Y.D. More Investments (TASE:MRIN) just released its Q3 2025 results, reporting total revenue of 252.4 million ILS and basic EPS of 0.33 ILS for the quarter. The company has seen revenue climb steadily from 212.4 million ILS in Q3 2024 to 252.4 million ILS this quarter, with trailing twelve month earnings growing 49.7% year-over-year. Margins improved over the last twelve months, highlighting expanding profitability for investors keeping a close eye on the company’s results.

See our full analysis for Y.D. More Investments.Now, let’s see how these numbers stack up against the prevailing market narratives. Some stories may gain support, while others could face new questions.

Curious how numbers become stories that shape markets? Explore Community Narratives

Profit Margins Reach 11.8%

- Net profit margin for Y.D. More Investments has moved up to 11.8% over the last twelve months, compared to 10% a year ago. The trailing twelve months net income (excluding extra items) totaled 111.5 million ILS on total revenue of 942.5 million ILS.

- What is notable is that, despite already strong margin expansion, the prevailing market view notes the company continues to be valued for its high quality of earnings and profitability improvements. However, this momentum is balanced against lingering concerns about valuation.

- The margin trend directly supports the argument that MRIN’s core platform is scaling well and increasing operating leverage, even as costs and market headwinds persist.

- There remains a tension since premium valuation expectations (see next subheading) mean investors are paying for this level of margin growth, so further improvements may be needed to justify the current pricing.

Share Price Far Above DCF Fair Value

- The latest share price stands at 50.77 ILS, more than four times the DCF fair value estimate of 11.06 ILS and well above the Asian Capital Markets industry average Price-to-Earnings ratio of 19.2x, with MRIN trading at 33.3x.

- Critics highlight that even though earnings quality is high, the bearish case gains traction when the stock’s premium valuation is considered, as it could limit future upside.

- MRIN’s PE ratio is not only significantly higher than its industry and peer averages, but the current market price exceeds the latest DCF value by 39.71 ILS per share.

- A wide gap between price and fair value raises concerns that the share price may already reflect the best-case scenario for margin and profit growth.

Dividend Track Record Remains Unstable

- The only risk flagged in the recent results period is an unstable dividend track record, with ongoing questions around dividend sustainability even as net income improved nearly 50% year-on-year.

- Market opinion focuses on the fact that, despite robust earnings and margin gains, consistency in returning capital to shareholders through dividends remains a sticking point.

- The absence of other major risk warnings puts more emphasis on dividend stability, which could impact the stock’s appeal to income-oriented investors.

- For now, the risk is labeled as minor, but a more reliable payout pattern would help strengthen the positive narrative for investors seeking both growth and income.

If you want to see a balanced view of how bulls and bears both see these numbers unfolding, dive into the full consensus narrative for more perspective. 📊 Read the full Y.D. More Investments Consensus Narrative.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Y.D. More Investments's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

While Y.D. More Investments continues to impress with margin expansion, serious valuation concerns and a spotty dividend record raise questions about long-term income potential and price sustainability.

If you prioritize reliable payouts and want to avoid these uncertainties, switch your focus to these 1942 dividend stocks with yields > 3% and discover stocks known for consistent dividend strength and income reliability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TASE:MRIN

Outstanding track record with flawless balance sheet.

Market Insights

Advertisement

Weekly Picks

FA

FAI on Arabian Internet and Communication Services ·

Solutions by stc: 34% Upside in Saudi's Digital Transformation Leader

Fair Value:ر.س342.2335.5% undervalued

10 followersusers have followed this narrative

1 commentusers have commented on this narrative

4 likesusers have liked this narrative

RO

RobertoAllende on NVIDIA ·

The AI Infrastructure Giant Grows Into Its Valuation

Fair Value:US$345.0747.9% undervalued

28 followersusers have followed this narrative

28 commentsusers have commented on this narrative

21 likesusers have liked this narrative

Recently Updated Narratives

TA

Talos on NVIDIA ·

Not a Bubble, But the "Industrial Revolution 4.0" Engine

Fair Value:US$294.9239.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Advanced Micro Devices ·

The "David vs. Goliath" AI Trade – Why Second Place is Worth Billions

Fair Value:US$416.4647.2% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on PayPal Holdings ·

The "Sleeping Giant" Wakes Up – Efficiency & Monetization

Fair Value:US$174.9264.2% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

111 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.1% undervalued

945 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.4% undervalued

146 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative