- Hong Kong

- /

- Transportation

- /

- SEHK:62

Hong Kong Market Highlights Three Undervalued Small Caps With Insider Buying

Reviewed by Simply Wall St

In recent trading sessions, the Hong Kong market has mirrored the cautious sentiment observed globally, with small-cap stocks showing resilience amidst broader fluctuations. This backdrop sets an intriguing stage for investors to consider undervalued small caps in Hong Kong, particularly those with recent insider buying which may signal confidence in long-term value despite current market uncertainties.

Top 10 Undervalued Small Caps With Insider Buying In Hong Kong

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Ferretti | 11.2x | 0.8x | 45.80% | ★★★★★☆ |

| Ever Sunshine Services Group | 5.6x | 0.4x | 22.22% | ★★★★★☆ |

| Wasion Holdings | 11.4x | 0.8x | 32.65% | ★★★★☆☆ |

| Nissin Foods | 14.2x | 1.3x | 42.29% | ★★★★☆☆ |

| Kinetic Development Group | 4.0x | 1.7x | 20.43% | ★★★★☆☆ |

| China Leon Inspection Holding | 9.7x | 0.7x | 28.19% | ★★★★☆☆ |

| Transport International Holdings | 11.6x | 0.6x | 44.01% | ★★★★☆☆ |

| Skyworth Group | 5.6x | 0.1x | -307.28% | ★★★☆☆☆ |

| Shenzhen International Holdings | 8.0x | 0.7x | 14.45% | ★★★☆☆☆ |

| Jinke Smart Services Group | NA | 0.8x | 34.07% | ★★★☆☆☆ |

We're going to check out a few of the best picks from our screener tool.

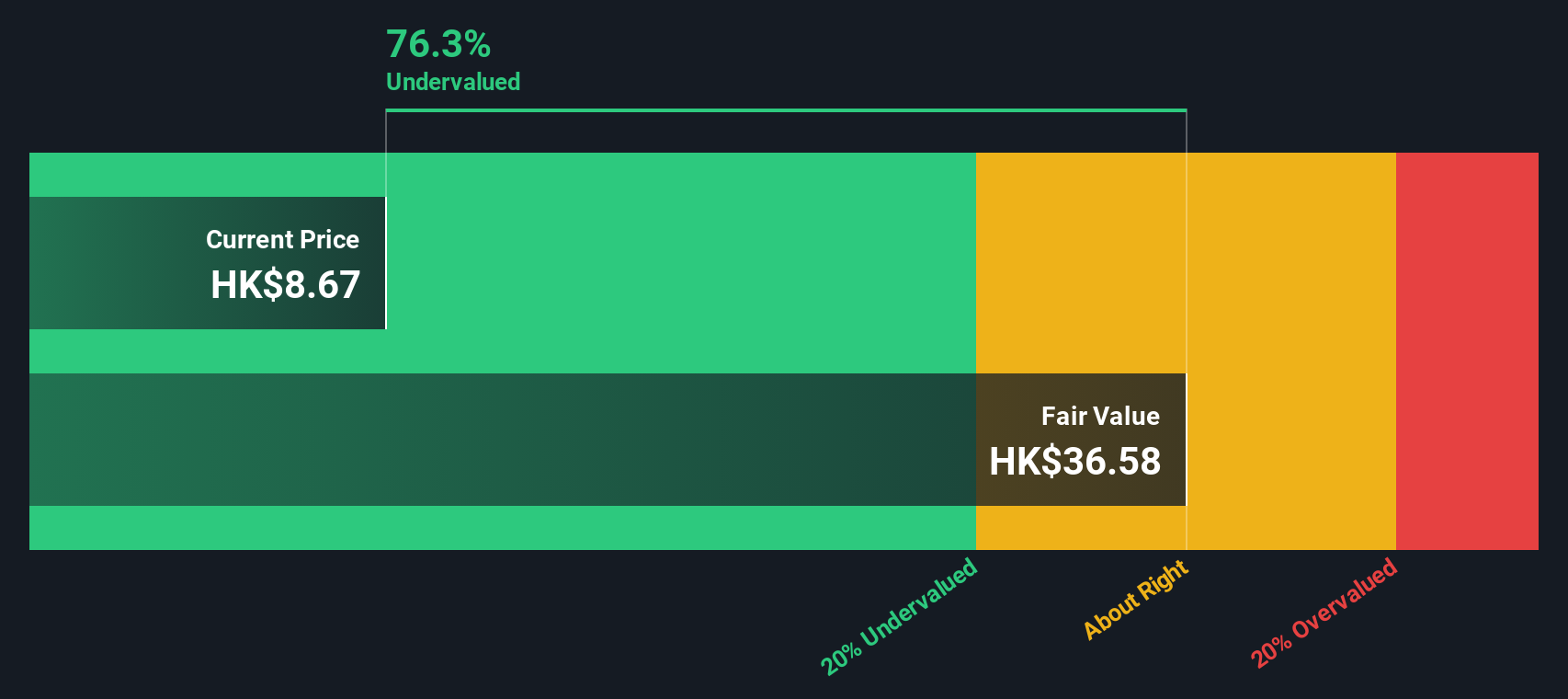

Shenzhen International Holdings (SEHK:152)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Shenzhen International Holdings operates in logistics, including parks and services, port-related services, toll roads, and environmental protection businesses.

Operations: Analyzing Shenzhen International Holdings' financial data reveals a notable trend in gross profit margin, which has shown variability over selected periods, peaking at 0.50% in mid-2014 and adjusting to 0.37% by the end of 2023. The company's revenue streams diversify across logistics parks, services, port-related services, toll roads, and environmental protection businesses contributing significantly to its financial structure with total revenues reaching HK$20.52 billion by late 2023.

PE: 8.0x

Shenzhen International Holdings, a smaller market player in Hong Kong, recently saw insider confidence demonstrated through significant purchases by Zhengyu Liu, who acquired 693,000 shares for HK$3.97 million. This move aligns with the company's positive outlook, underscored by a recent board reshuffle enhancing governance and strategic planning capabilities. Additionally, the firm's commitment to growth is evident from its approved dividend increase and substantial investment in infrastructure projects set to enhance long-term value. These developments suggest a promising trajectory for Shenzhen International Holdings amidst its industry peers.

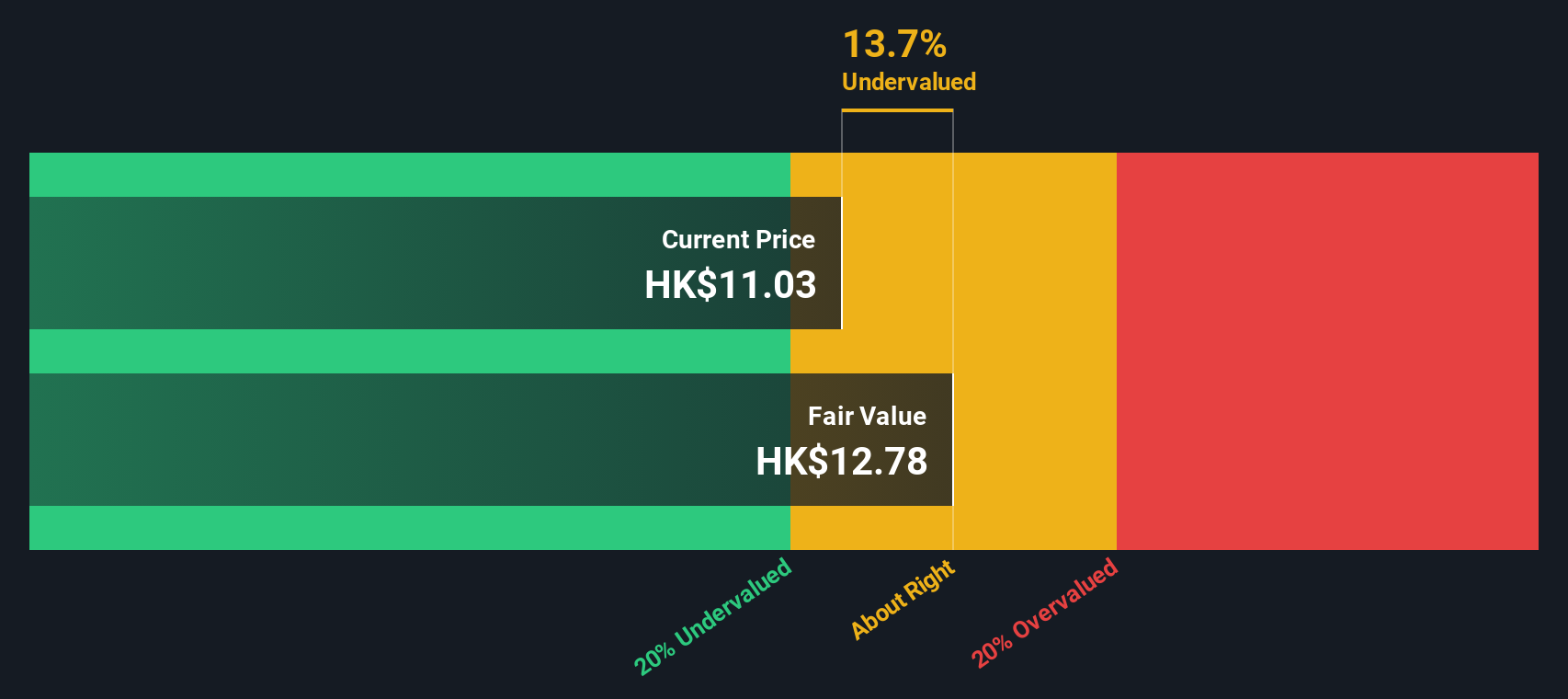

Wasion Holdings (SEHK:3393)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Wasion Holdings is a company primarily engaged in the manufacturing of advanced metering products and providing solutions for electricity, water, and gas utilities, with a market capitalization of approximately CN¥4.37 billion.

Operations: Advanced Distribution Operations, Power Advanced Metering Infrastructure, and Communication and Fluid Advanced Metering Infrastructure collectively generated revenues of CN¥7.37 billion. The company's gross profit margin improved to 35.59% by the end of the period covered.

PE: 11.4x

Wasion Holdings, a lesser-known entity in Hong Kong's vibrant market, recently saw insider confidence bolstered as Wei Ji acquired 500,000 shares for HK$3.17 million on May 10, 2024. This purchase underscores belief in the company’s potential despite its reliance on external borrowing—a higher risk funding method. Additionally, Wasion announced a dividend increase to HK$0.28 per share at their AGM, reflecting a positive financial stance and commitment to shareholder returns. Forecasted earnings growth of 25.8% annually hints at promising prospects ahead for this firm.

- Dive into the specifics of Wasion Holdings here with our thorough valuation report.

Understand Wasion Holdings' track record by examining our Past report.

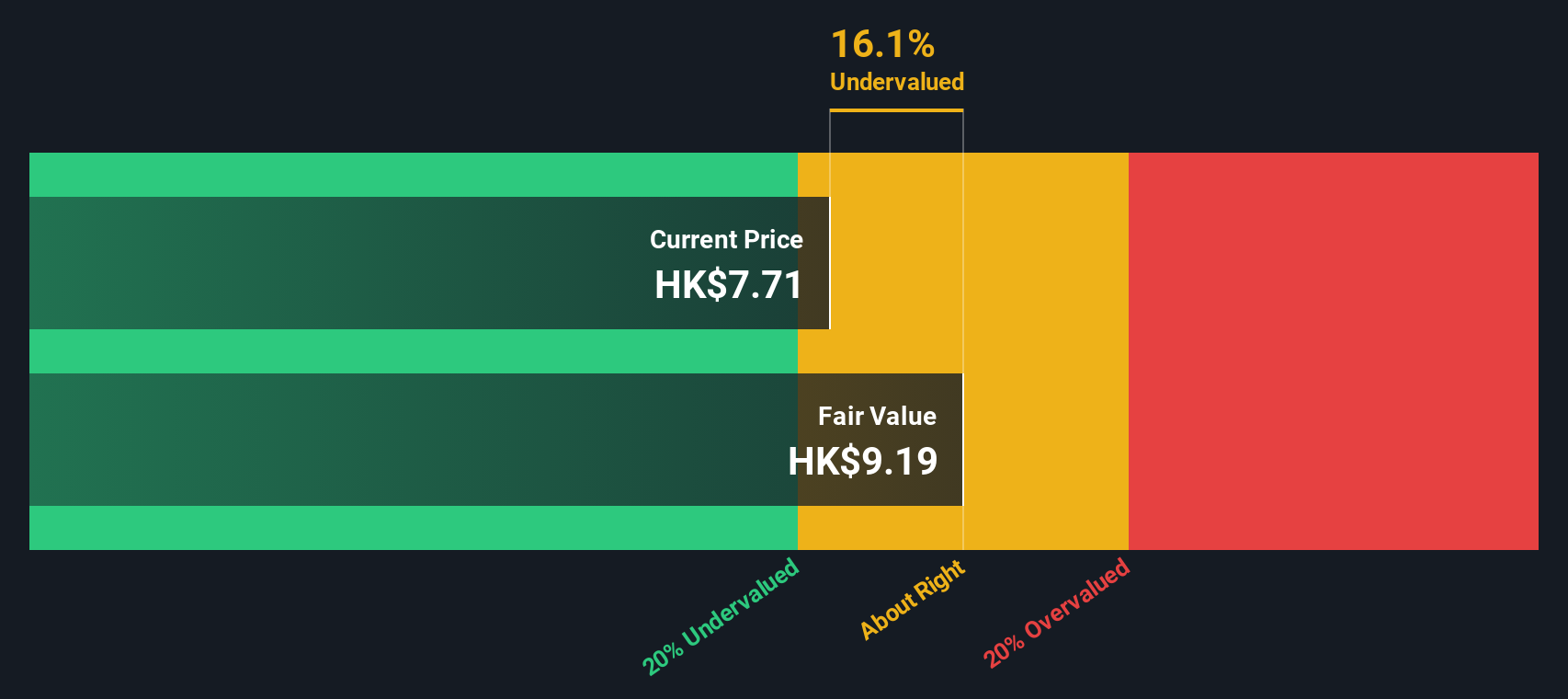

Transport International Holdings (SEHK:62)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Transport International Holdings operates primarily in franchised bus services, alongside engagements in property holdings and development, with a smaller contribution from other business activities.

Operations: Franchised Bus Operation is the primary revenue generator with HK$7.57 billion, significantly overshadowing Property Holdings and Development's contribution of HK$87.36 million. The company has observed a gross profit margin increase from 22.29% to 27.93% over the periods reviewed, reflecting an improvement in cost management relative to revenue generated from core operations.

PE: 11.6x

Recently, Transport International Holdings has shown notable insider confidence, with Non-Executive Director Winnie J. Ng purchasing 124,000 shares for HK$1.11 million. This move, indicating a significant 68% increase in their stake, underscores a strong belief in the company's prospects despite its challenges such as declining earnings and higher-risk funding structures. The firm's commitment to maintaining dividends, evidenced by the recent HK$0.50 per share payout affirmed at their AGM, further demonstrates resilience and potential for growth amidst operational adjustments like the strategic board reshuffle on June 20th.

- Click here to discover the nuances of Transport International Holdings with our detailed analytical valuation report.

Learn about Transport International Holdings' historical performance.

Seize The Opportunity

- Embark on your investment journey to our 17 Undervalued SEHK Small Caps With Insider Buying selection here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Transport International Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:62

Transport International Holdings

An investment holding company, provides franchised and non-franchised public transportation services in the People’s Republic of China.

Adequate balance sheet low.