Advertisement

Sinotrans (SEHK:598) Earnings Decline Might Change The Case For Investing In the Logistics Firm

Simply Wall St

Reviewed by Sasha Jovanovic

- Sinotrans Limited reported its earnings for the nine months ended September 30, 2025, showing sales of CNY 75.04 billion and net income of CNY 2.68 billion, both lower than the previous year.

- This decline in both revenue and net income signals continued business headwinds and operational pressures for the company over the past year.

- Next, we’ll explore how Sinotrans’s year-on-year decline in core financials may influence the company’s long-term investment case.

Find companies with promising cash flow potential yet trading below their fair value.

Sinotrans Investment Narrative Recap

To believe in Sinotrans as a shareholder, you need conviction in its ability to adapt through global logistics cycles, leverage e-commerce growth, and expand internationally, despite recent signs of weaker performance. The latest earnings release, with both sales and net income down year-on-year, does not materially change the biggest short-term catalyst, which remains Sinotrans’s push into cross-border e-commerce, but it does put a spotlight on competitive margin pressures in traditional freight forwarding that are currently the largest risk to watch.

Among recent announcements, the approval of unaudited third-quarter results on October 14 provides the most context for the updated earnings figures. These numbers reinforce that cost controls and business model shifts toward higher-value services must continue in order to address declining revenue, especially as Sinotrans seeks to maintain relevance and profitability in a competitive international logistics market.

In contrast, shareholders should be aware that exposure to intense price competition in traditional segments could further erode net margins if...

Read the full narrative on Sinotrans (it's free!)

Sinotrans is projected to achieve CN¥116.2 billion in revenue and CN¥4.0 billion in earnings by 2028. This outlook assumes a 3.4% annual revenue growth rate and a CN¥0.2 billion increase in earnings from the current level of CN¥3.8 billion.

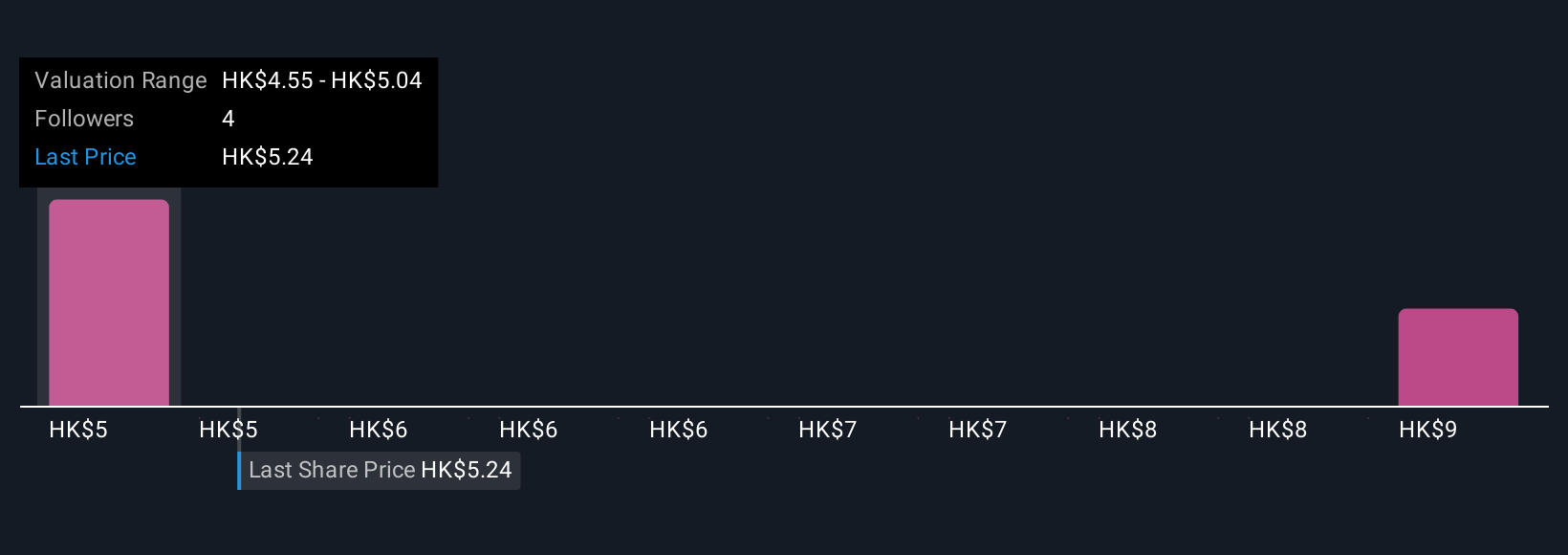

Uncover how Sinotrans' forecasts yield a HK$4.55 fair value, a 15% downside to its current price.

Exploring Other Perspectives

Private investors in the Simply Wall St Community placed Sinotrans’s fair value anywhere from HK$4.55 to HK$9.66, with two distinct perspectives reflected. Amid these diverging estimates, keep in mind that recent pressure on freight rates and margins may shape future results quite differently than current forecasts suggest, explore the range of community insights for a fuller view.

Explore 2 other fair value estimates on Sinotrans - why the stock might be worth as much as 81% more than the current price!

Build Your Own Sinotrans Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Sinotrans research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free Sinotrans research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Sinotrans' overall financial health at a glance.

Ready For A Different Approach?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

- We've found 18 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:598

Sinotrans

Provides integrated logistics services primarily in the People’s Republic of China.

Flawless balance sheet, good value and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.4% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.3% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|4.1% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|62.7% undervalued

DA

Community Contributor