Advertisement

- Hong Kong

- /

- Infrastructure

- /

- SEHK:576

Zhejiang Expressway Co., Ltd.'s (HKG:576) Prospects Need A Boost To Lift Shares

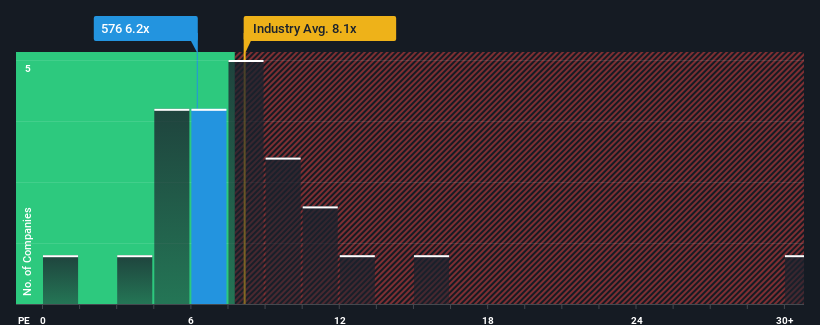

Zhejiang Expressway Co., Ltd.'s (HKG:576) price-to-earnings (or "P/E") ratio of 6.2x might make it look like a buy right now compared to the market in Hong Kong, where around half of the companies have P/E ratios above 12x and even P/E's above 23x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

We've discovered 1 warning sign about Zhejiang Expressway. View them for free.Zhejiang Expressway could be doing better as its earnings have been going backwards lately while most other companies have been seeing positive earnings growth. The P/E is probably low because investors think this poor earnings performance isn't going to get any better. If you still like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

See our latest analysis for Zhejiang Expressway

Is There Any Growth For Zhejiang Expressway?

There's an inherent assumption that a company should underperform the market for P/E ratios like Zhejiang Expressway's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 8.9% decrease to the company's bottom line. This means it has also seen a slide in earnings over the longer-term as EPS is down 12% in total over the last three years. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Turning to the outlook, the next three years should generate growth of 1.6% each year as estimated by the five analysts watching the company. With the market predicted to deliver 15% growth per annum, the company is positioned for a weaker earnings result.

With this information, we can see why Zhejiang Expressway is trading at a P/E lower than the market. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Final Word

Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

As we suspected, our examination of Zhejiang Expressway's analyst forecasts revealed that its inferior earnings outlook is contributing to its low P/E. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. It's hard to see the share price rising strongly in the near future under these circumstances.

Having said that, be aware Zhejiang Expressway is showing 1 warning sign in our investment analysis, you should know about.

You might be able to find a better investment than Zhejiang Expressway. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang Expressway might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:576

Zhejiang Expressway

An investment holding company, invests, develops, maintains, and operates roads in the People’s Republic of China.

Excellent balance sheet established dividend payer.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor