Stock Analysis

- Hong Kong

- /

- Infrastructure

- /

- SEHK:144

China Merchants Port Holdings (HKG:144) Has A Somewhat Strained Balance Sheet

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that China Merchants Port Holdings Company Limited (HKG:144) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for China Merchants Port Holdings

What Is China Merchants Port Holdings's Debt?

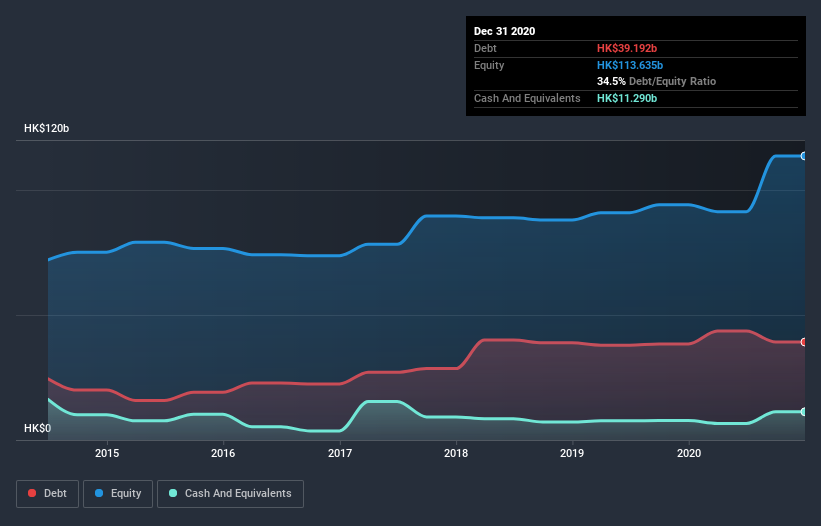

The chart below, which you can click on for greater detail, shows that China Merchants Port Holdings had HK$39.2b in debt in December 2020; about the same as the year before. However, it also had HK$11.3b in cash, and so its net debt is HK$27.9b.

How Strong Is China Merchants Port Holdings' Balance Sheet?

The latest balance sheet data shows that China Merchants Port Holdings had liabilities of HK$15.6b due within a year, and liabilities of HK$40.8b falling due after that. On the other hand, it had cash of HK$11.3b and HK$5.58b worth of receivables due within a year. So it has liabilities totalling HK$39.6b more than its cash and near-term receivables, combined.

This deficit is considerable relative to its market capitalization of HK$44.6b, so it does suggest shareholders should keep an eye on China Merchants Port Holdings' use of debt. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Weak interest cover of 1.7 times and a disturbingly high net debt to EBITDA ratio of 7.2 hit our confidence in China Merchants Port Holdings like a one-two punch to the gut. This means we'd consider it to have a heavy debt load. Fortunately, China Merchants Port Holdings grew its EBIT by 3.5% in the last year, slowly shrinking its debt relative to earnings. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if China Merchants Port Holdings can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, China Merchants Port Holdings actually produced more free cash flow than EBIT. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

China Merchants Port Holdings's net debt to EBITDA and interest cover definitely weigh on it, in our esteem. But its conversion of EBIT to free cash flow tells a very different story, and suggests some resilience. We should also note that Infrastructure industry companies like China Merchants Port Holdings commonly do use debt without problems. Looking at all the angles mentioned above, it does seem to us that China Merchants Port Holdings is a somewhat risky investment as a result of its debt. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For instance, we've identified 4 warning signs for China Merchants Port Holdings that you should be aware of.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

When trading China Merchants Port Holdings or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're helping make it simple.

Find out whether China Merchants Port Holdings is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:144

China Merchants Port Holdings

An investment holding company, operates as a port operator in Mainland China, Brazil, Hong Kong, Taiwan, and internationally.

Fair value second-rate dividend payer.