Advertisement

- Hong Kong

- /

- Electronic Equipment and Components

- /

- SEHK:1611

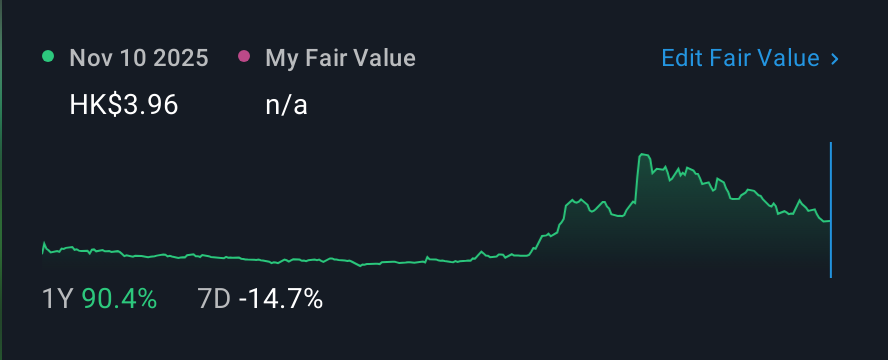

Sinohope Technology Holdings (HKG:1611) shareholder returns have been stellar, earning 163% in 1 year

Unfortunately, investing is risky - companies can and do go bankrupt. On the other hand, if you find a high quality business to buy (at the right price) you can more than double your money! For example, the Sinohope Technology Holdings Limited (HKG:1611) share price had more than doubled in just one year - up 163%. It's up an even more impressive 201% over the last quarter. However, the longer term returns haven't been so impressive, with the stock up just 17% in the last three years.

Since it's been a strong week for Sinohope Technology Holdings shareholders, let's have a look at trend of the longer term fundamentals.

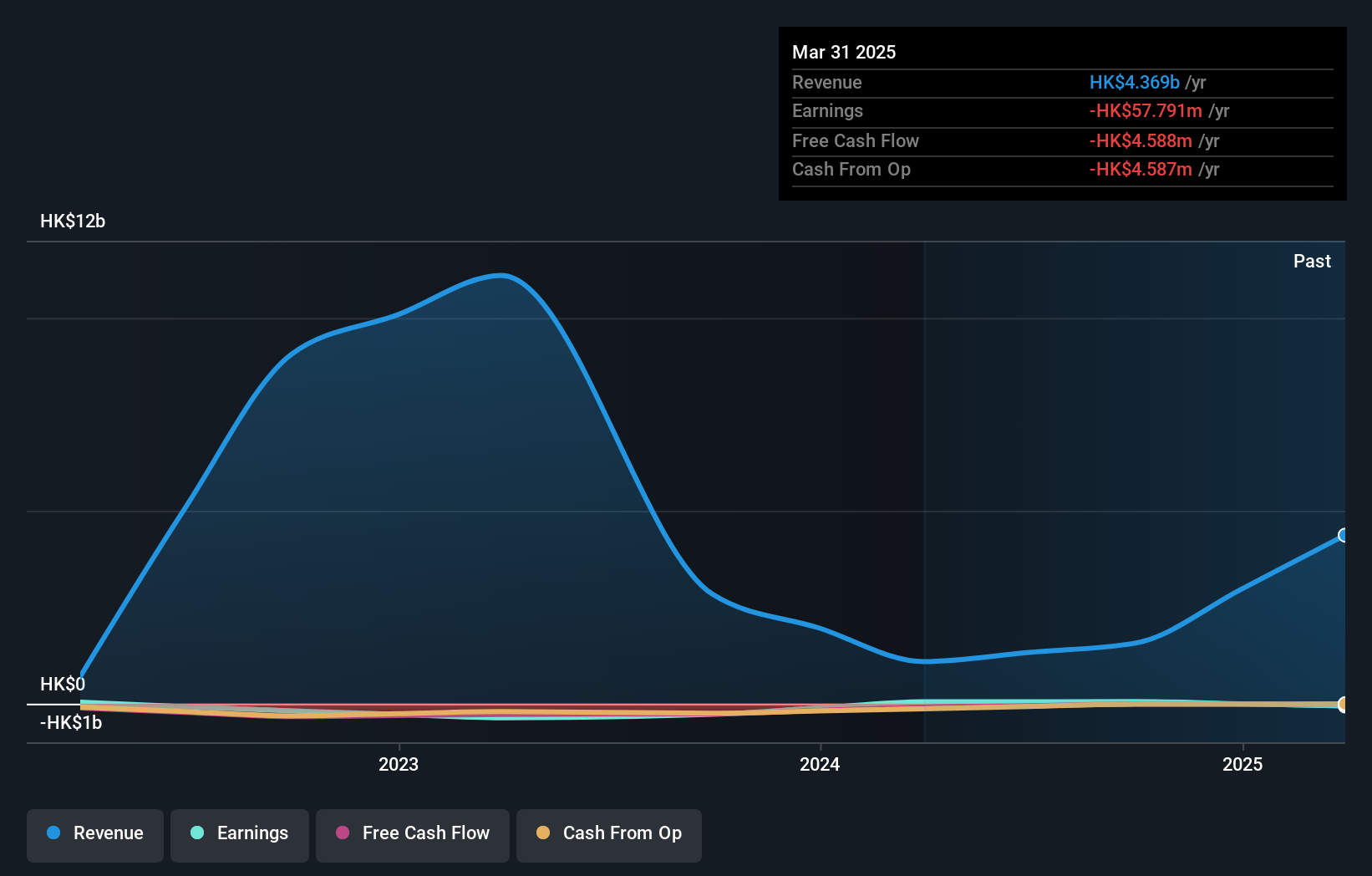

Sinohope Technology Holdings wasn't profitable in the last twelve months, it is unlikely we'll see a strong correlation between its share price and its earnings per share (EPS). Arguably revenue is our next best option. Generally speaking, companies without profits are expected to grow revenue every year, and at a good clip. Some companies are willing to postpone profitability to grow revenue faster, but in that case one would hope for good top-line growth to make up for the lack of earnings.

In the last year Sinohope Technology Holdings saw its revenue grow by 300%. That's well above most other pre-profit companies. Meanwhile, the market has paid attention, sending the share price soaring 163% in response. It's great to see strong revenue growth, but the question is whether it can be sustained. The strong share price rise indicates optimism, so there may be a better opportunity for buyers as the hype fades a bit.

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

We consider it positive that insiders have made significant purchases in the last year. Having said that, most people consider earnings and revenue growth trends to be a more meaningful guide to the business. It might be well worthwhile taking a look at our free report on Sinohope Technology Holdings' earnings, revenue and cash flow.

A Different Perspective

We're pleased to report that Sinohope Technology Holdings shareholders have received a total shareholder return of 163% over one year. That gain is better than the annual TSR over five years, which is 2%. Therefore it seems like sentiment around the company has been positive lately. Someone with an optimistic perspective could view the recent improvement in TSR as indicating that the business itself is getting better with time. It's always interesting to track share price performance over the longer term. But to understand Sinohope Technology Holdings better, we need to consider many other factors. Even so, be aware that Sinohope Technology Holdings is showing 3 warning signs in our investment analysis , and 2 of those make us uncomfortable...

There are plenty of other companies that have insiders buying up shares. You probably do not want to miss this free list of undervalued small cap companies that insiders are buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Hong Kong exchanges.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1611

Sinohope Technology Holdings

An investment holding company, provides cryptocurrency trading and technology solution services in the People’s Republic of China.

Flawless balance sheet with slight risk.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.8% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor