Advertisement

Kingboard Holdings' (HKG:148) Dividend Will Be Reduced To HK$0.36

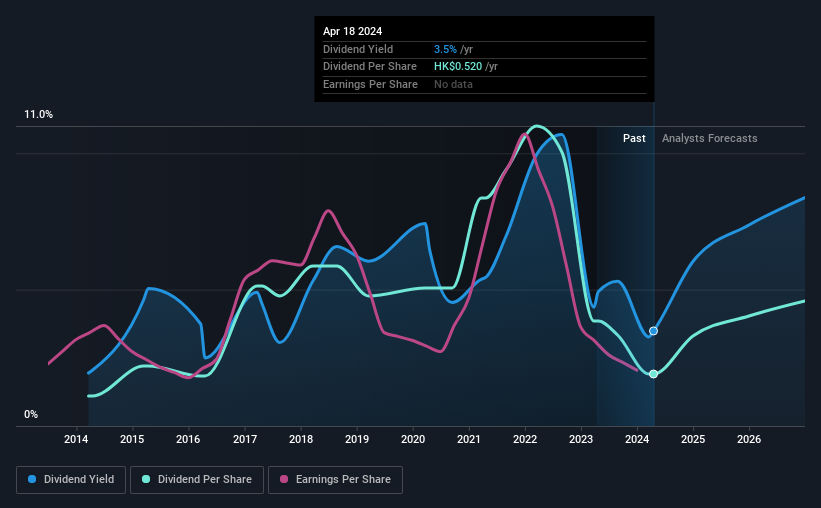

Kingboard Holdings Limited (HKG:148) is reducing its dividend from last year's comparable payment to HK$0.36 on the 5th of July. This means that the annual payment will be 3.5% of the current stock price, which is in line with the average for the industry.

View our latest analysis for Kingboard Holdings

Kingboard Holdings' Dividend Is Well Covered By Earnings

Unless the payments are sustainable, the dividend yield doesn't mean too much. However, prior to this announcement, Kingboard Holdings' dividend was comfortably covered by both cash flow and earnings. This means that most of its earnings are being retained to grow the business.

Looking forward, could fall by 20.0% if the company can't turn things around from the last few years. However, if the dividend continues along recent trends, we estimate the payout ratio could reach 76%, meaning that most of the company's earnings is being paid out to shareholders.

Dividend Volatility

The company's dividend history has been marked by instability, with at least one cut in the last 10 years. The annual payment during the last 10 years was HK$0.30 in 2014, and the most recent fiscal year payment was HK$0.52. This implies that the company grew its distributions at a yearly rate of about 5.7% over that duration. It's good to see the dividend growing at a decent rate, but the dividend has been cut at least once in the past. Kingboard Holdings might have put its house in order since then, but we remain cautious.

Dividend Growth Potential Is Shaky

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. Kingboard Holdings' earnings per share has shrunk at 20% a year over the past five years. Dividend payments are likely to come under some pressure unless EPS can pull out of the nosedive it is in.

In Summary

Overall, it's not great to see that the dividend has been cut, but this might be explained by the payments being a bit high previously. In the past, the payments have been unstable, but over the short term the dividend could be reliable, with the company generating enough cash to cover it. We would probably look elsewhere for an income investment.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. As an example, we've identified 2 warning signs for Kingboard Holdings that you should be aware of before investing. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Kingboard Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:148

Kingboard Holdings

An investment holding company, manufactures and sells laminates, printed circuit boards (PCBs), magnetic products, and chemicals in the People’s Republic of China, rest of Asia, Europe, and the United States.

Flawless balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|66.7% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|4.8% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.5% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor