- Hong Kong

- /

- Tech Hardware

- /

- SEHK:1401

Kinetic Development Group And 2 Other Undiscovered Gems In Hong Kong

Reviewed by Simply Wall St

As global markets experience fluctuations, with the Hang Seng Index in Hong Kong recently witnessing a notable decline of 6.53%, investors are increasingly on the lookout for overlooked opportunities that may offer potential amidst broader market volatility. In this context, identifying stocks with strong fundamentals and innovative strategies becomes crucial, as these characteristics can provide resilience and growth potential even in challenging economic climates.

Top 10 Undiscovered Gems With Strong Fundamentals In Hong Kong

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Lion Rock Group | 16.91% | 14.33% | 10.15% | ★★★★★★ |

| C&D Property Management Group | 1.32% | 37.15% | 41.55% | ★★★★★★ |

| Changjiu Holdings | NA | 11.84% | 2.46% | ★★★★★★ |

| COSCO SHIPPING International (Hong Kong) | NA | -3.84% | 16.33% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Xin Point Holdings | 1.77% | 10.88% | 22.83% | ★★★★★☆ |

| S.A.S. Dragon Holdings | 60.96% | 4.62% | 10.02% | ★★★★★☆ |

| Billion Industrial Holdings | 3.63% | 18.00% | -11.38% | ★★★★★☆ |

| Chongqing Machinery & Electric | 27.77% | 8.82% | 11.12% | ★★★★☆☆ |

| Pizu Group Holdings | 48.34% | -4.53% | -19.78% | ★★★★☆☆ |

Let's dive into some prime choices out of from the screener.

Kinetic Development Group (SEHK:1277)

Simply Wall St Value Rating: ★★★★★☆

Overview: Kinetic Development Group Limited is an investment holding company involved in the extraction and sale of coal products in the People’s Republic of China, with a market capitalization of HK$14.25 billion.

Operations: Kinetic Development Group generates revenue primarily through the extraction and sale of coal products in China. The company's financial performance is highlighted by a net profit margin trend worth noting, which reflects its ability to manage costs relative to its revenue streams.

Kinetic Development Group, a small player in Hong Kong's market, has shown impressive growth with earnings up 39.2% over the past year, outpacing the Oil and Gas industry. Its net debt to equity ratio stands at a satisfactory 4.7%, while EBIT covers interest payments 163 times over, indicating strong financial health. Recent earnings reveal sales of CNY 2.53 billion and net income of CNY 1.10 billion for H1 2024, alongside dividend announcements reflecting growing shareholder value.

- Dive into the specifics of Kinetic Development Group here with our thorough health report.

Understand Kinetic Development Group's track record by examining our Past report.

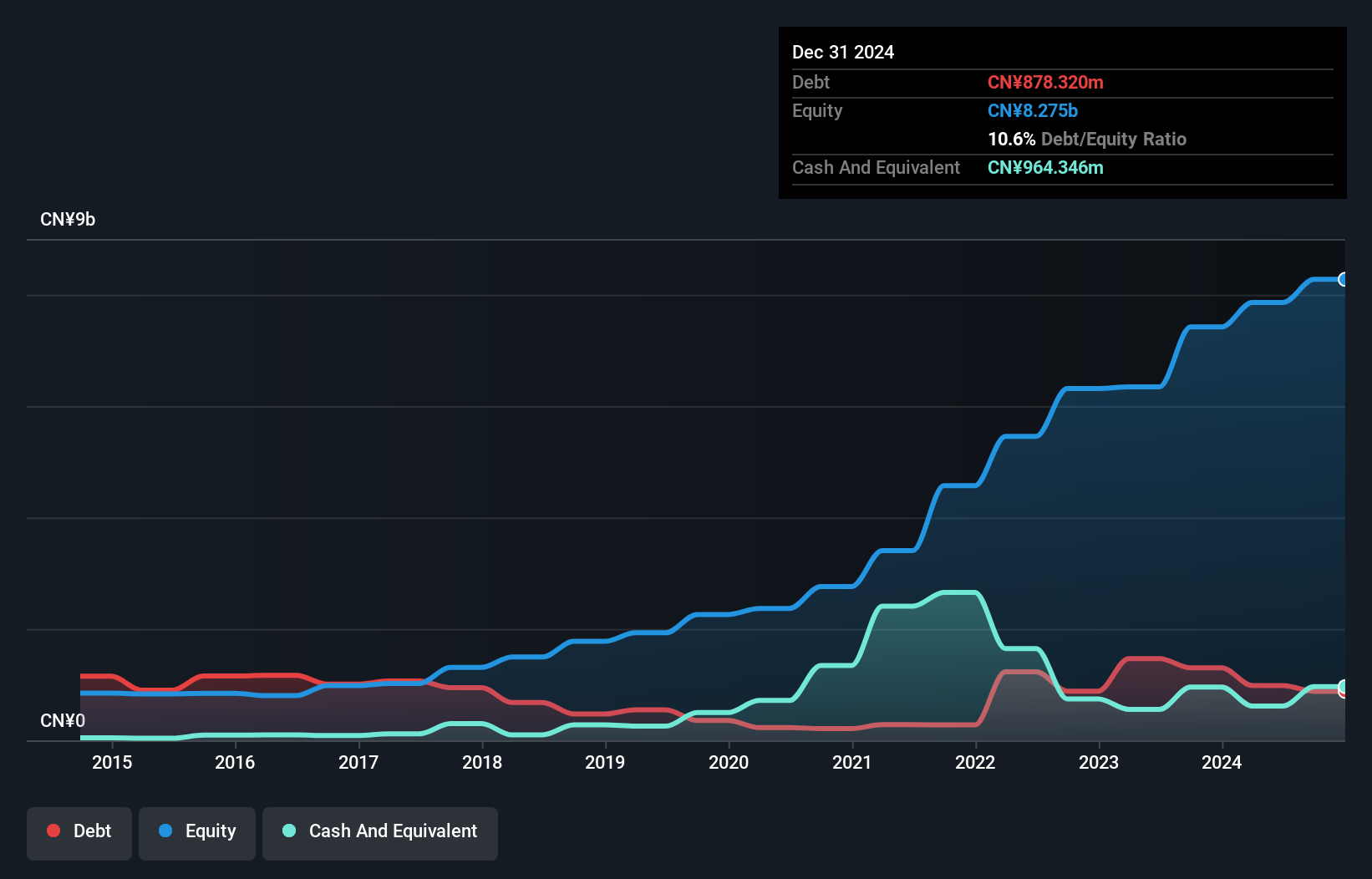

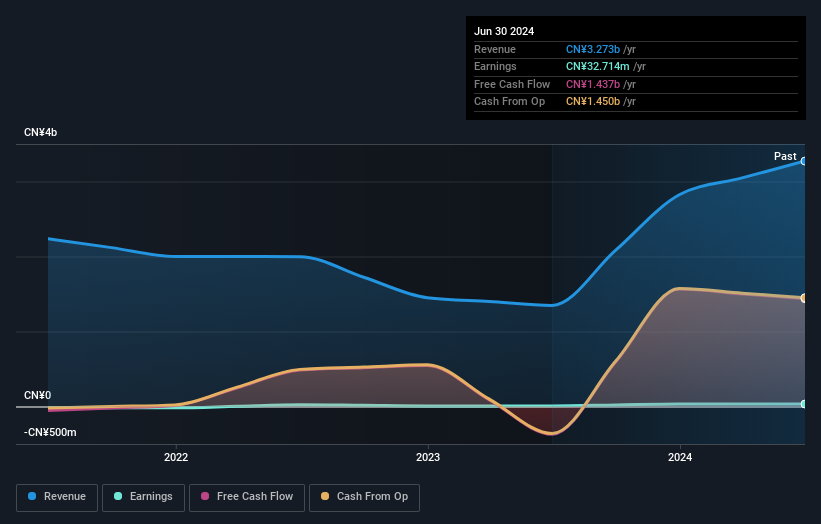

Sprocomm Intelligence (SEHK:1401)

Simply Wall St Value Rating: ★★★★★☆

Overview: Sprocomm Intelligence Limited is an investment holding company involved in the research and development, design, manufacture, and sale of mobile phones across China, India, Algeria, Bangladesh, and other international markets with a market cap of HK$6.07 billion.

Operations: Sprocomm Intelligence generates revenue primarily from the sale of wireless communications equipment, amounting to CN¥3.27 billion.

Sprocomm Intelligence, a small player in the tech sector, has seen its earnings grow by 301% over the past year, outpacing the industry average. Despite this impressive growth, its debt to equity ratio has improved significantly from 73.8% to 37.6% over five years, reflecting better financial health. Recently, Sprocomm reported sales of CN¥1.26 billion for the half-year ending June 2024 and experienced a modest net income increase to CN¥9.86 million compared to last year’s CN¥9.51 million.

- Unlock comprehensive insights into our analysis of Sprocomm Intelligence stock in this health report.

Explore historical data to track Sprocomm Intelligence's performance over time in our Past section.

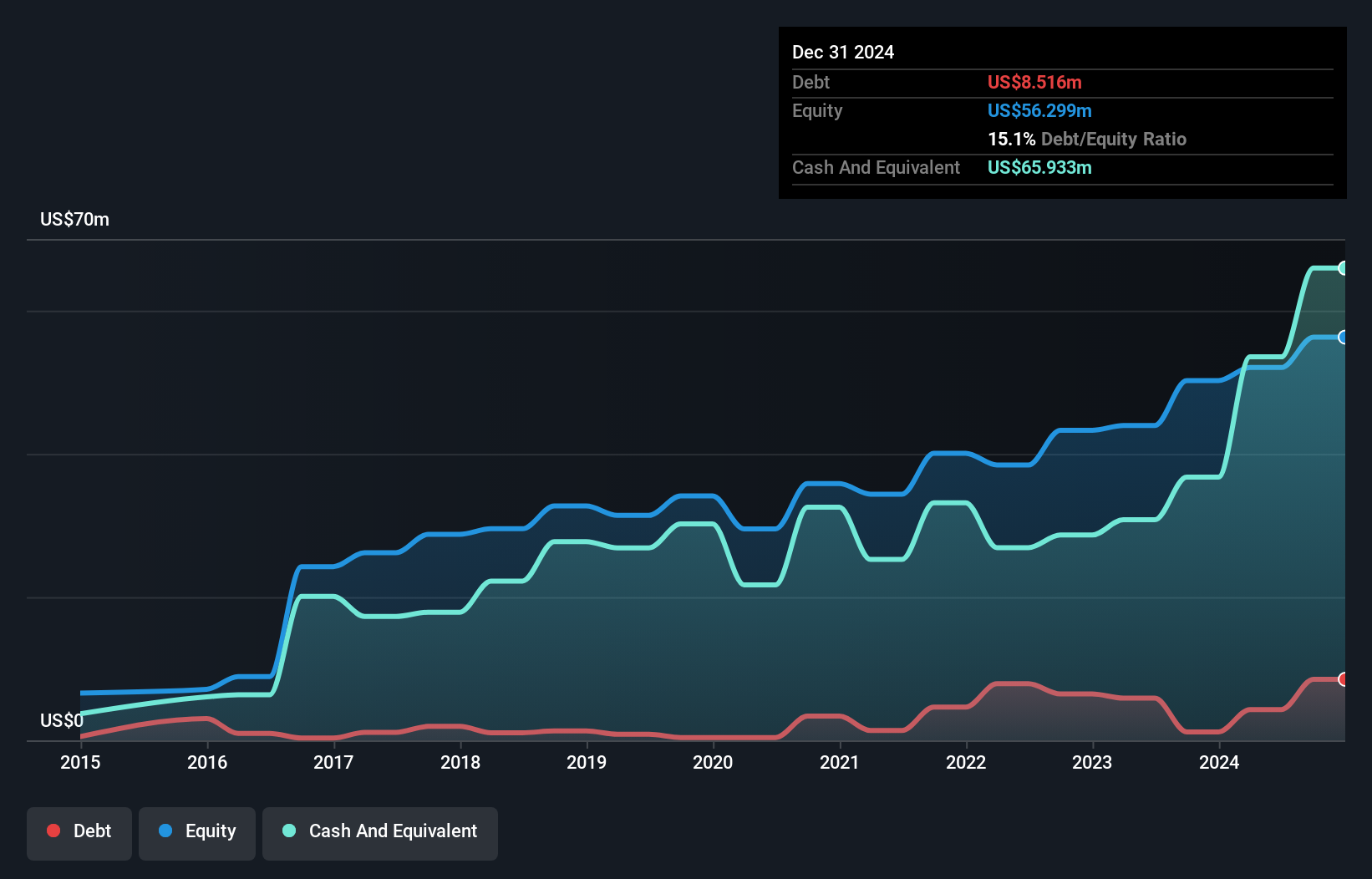

Plover Bay Technologies (SEHK:1523)

Simply Wall St Value Rating: ★★★★★☆

Overview: Plover Bay Technologies Limited, an investment holding company, designs, develops, and markets software-defined wide area network routers with a market capitalization of HK$5.53 billion.

Operations: Revenue streams for Plover Bay Technologies primarily include sales of SD-WAN routers with mobile first connectivity contributing $59.87 million and fixed first connectivity at $15.19 million, alongside software licenses and warranty/support services generating $31.86 million.

Plover Bay Technologies, a dynamic player in the tech sector, has shown impressive earnings growth of 41% over the past year. This company is trading at a significant discount, around 50% below its estimated fair value. Recent financials reveal sales of US$57 million and net income reaching US$19 million for the first half of 2024. The recent appointment of Ms. Chiu as an executive director aims to enhance board diversity and expertise, potentially bolstering future strategic initiatives.

- Get an in-depth perspective on Plover Bay Technologies' performance by reading our health report here.

Evaluate Plover Bay Technologies' historical performance by accessing our past performance report.

Make It Happen

- Delve into our full catalog of 168 SEHK Undiscovered Gems With Strong Fundamentals here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:1401

Sprocomm Intelligence

An investment holding company, engages in the research and development, design, manufacture, and sale of mobile phones in the People’s Republic of China, India, Algeria, Bangladesh, and internationally.

Excellent balance sheet with acceptable track record.