- Hong Kong

- /

- Entertainment

- /

- SEHK:3888

Kingsoft Corporation Limited Just Recorded A 128% EPS Beat: Here's What Analysts Are Forecasting Next

Last week saw the newest third-quarter earnings release from Kingsoft Corporation Limited (HKG:3888), an important milestone in the company's journey to build a stronger business. It looks like a credible result overall - although revenues of CN¥1.4b were what the analysts expected, Kingsoft surprised by delivering a (statutory) profit of CN¥0.48 per share, an impressive 128% above what was forecast. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

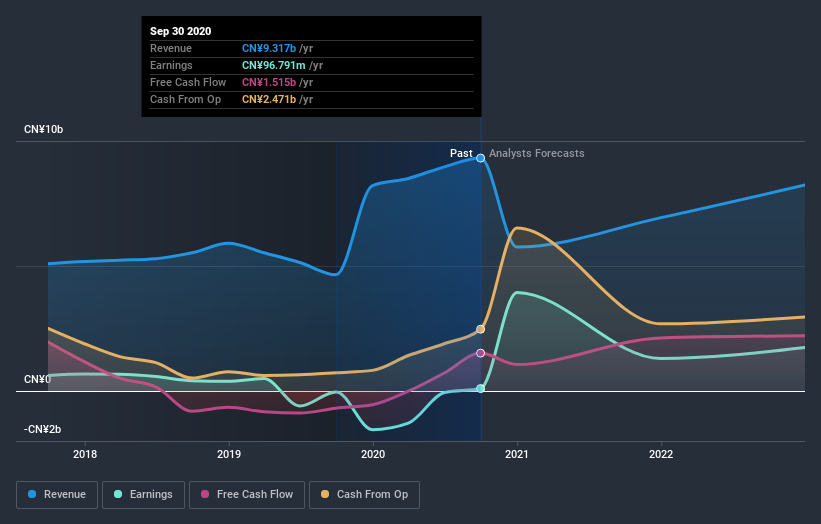

See our latest analysis for Kingsoft

Taking into account the latest results, the current consensus, from the 17 analysts covering Kingsoft, is for revenues of CN¥6.93b in 2021, which would reflect a sizeable 26% reduction in Kingsoft's sales over the past 12 months. Statutory earnings per share are predicted to shoot up 1,283% to CN¥0.95. Before this earnings report, the analysts had been forecasting revenues of CN¥7.09b and earnings per share (EPS) of CN¥1.03 in 2021. It's pretty clear that pessimism has reared its head after the latest results, leading to a weaker revenue outlook and a small dip in earnings per share estimates.

The average price target climbed 5.0% to CN¥41.84despite the reduced earnings forecasts, suggesting that this earnings impact could be a positive for the stock, once it passes. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. Currently, the most bullish analyst values Kingsoft at CN¥60.00 per share, while the most bearish prices it at CN¥16.54. As you can see the range of estimates is wide, with the lowest valuation coming in at less than half the most bullish estimate, suggesting there are some strongly diverging views on how analysts think this business will perform. As a result it might not be a great idea to make decisions based on the consensus price target, which is after all just an average of this wide range of estimates.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Kingsoft's past performance and to peers in the same industry. These estimates imply that sales are expected to slow, with a forecast revenue decline of 26%, a significant reduction from annual growth of 13% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 27% next year. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - Kingsoft is expected to lag the wider industry.

The Bottom Line

The most important thing to take away is that the analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. Unfortunately, they also downgraded their revenue estimates, and our data indicates revenues are expected to perform worse than the wider industry. Even so, earnings per share are more important to the intrinsic value of the business. There was also a nice increase in the price target, with the analysts clearly feeling that the intrinsic value of the business is improving.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. We have estimates - from multiple Kingsoft analysts - going out to 2022, and you can see them free on our platform here.

Don't forget that there may still be risks. For instance, we've identified 2 warning signs for Kingsoft (1 can't be ignored) you should be aware of.

When trading Kingsoft or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Kingsoft might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About SEHK:3888

Kingsoft

Engages in the entertainment and office software and services businesses in Mainland China, Hong Kong, and internationally.

Flawless balance sheet with solid track record.