The Hong Kong market has seen significant gains recently, buoyed by China's robust stimulus measures aimed at revitalizing the economy. Amid this positive backdrop, investors are increasingly looking at growth companies with high insider ownership as potential opportunities. In the current environment, stocks with substantial insider ownership often signal strong confidence from those closest to the company's operations and future prospects. This can be particularly appealing for investors seeking alignment between management and shareholder interests in a thriving market.

Top 10 Growth Companies With High Insider Ownership In Hong Kong

| Name | Insider Ownership | Earnings Growth |

| Laopu Gold (SEHK:6181) | 36.4% | 32.7% |

| Akeso (SEHK:9926) | 20.5% | 54.5% |

| Fenbi (SEHK:2469) | 33.1% | 22.4% |

| Zylox-Tonbridge Medical Technology (SEHK:2190) | 18.8% | 69.8% |

| Pacific Textiles Holdings (SEHK:1382) | 11.2% | 37.7% |

| Zhejiang Leapmotor Technology (SEHK:9863) | 15% | 78.9% |

| DPC Dash (SEHK:1405) | 38.1% | 104.2% |

| Kindstar Globalgene Technology (SEHK:9960) | 16.5% | 88% |

| Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) | 13.9% | 109.2% |

| Beijing Airdoc Technology (SEHK:2251) | 29.1% | 93.4% |

Below we spotlight a couple of our favorites from our exclusive screener.

Kingdee International Software Group (SEHK:268)

Simply Wall St Growth Rating: ★★★★☆☆

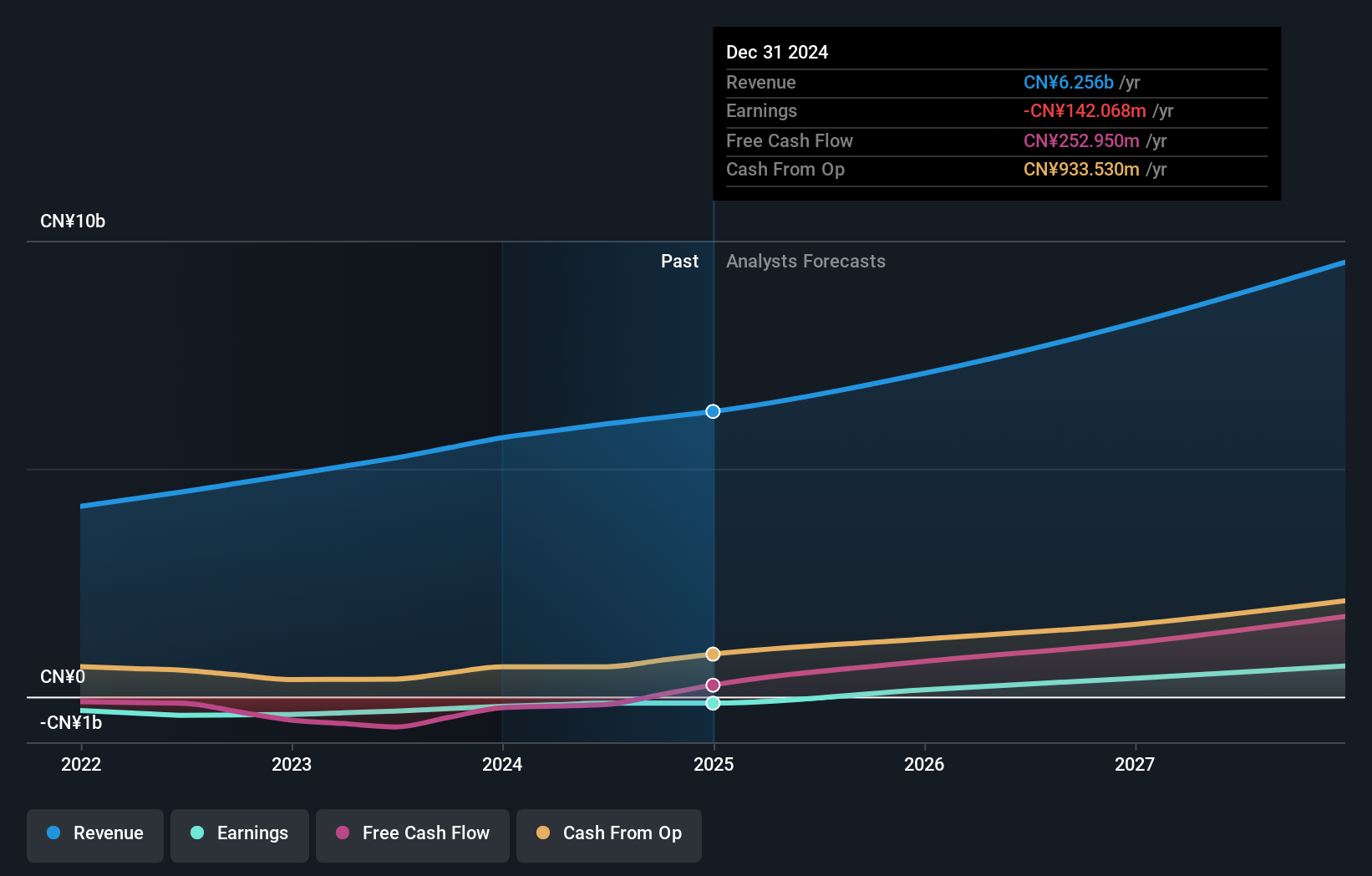

Overview: Kingdee International Software Group Company Limited, with a market cap of HK$28.80 billion, operates in the enterprise resource planning business as an investment holding company.

Operations: The company's revenue segments include CN¥4.86 billion from its Cloud Service Business and CN¥1.13 billion from its ERP Business and Others.

Insider Ownership: 19.9%

Revenue Growth Forecast: 13.9% p.a.

Kingdee International Software Group, a growth company with high insider ownership in Hong Kong, reported H1 2024 sales of CNY 2.87 billion, up from CNY 2.57 billion a year ago. Despite a net loss reduction to CNY 217.85 million from CNY 283.54 million, shareholders faced dilution over the past year. Revenue is forecast to grow at 13.9% per year and earnings at 45.85% annually, outpacing the market's average growth rate as it aims for profitability within three years.

- Click here to discover the nuances of Kingdee International Software Group with our detailed analytical future growth report.

- Our valuation report unveils the possibility Kingdee International Software Group's shares may be trading at a discount.

Meituan (SEHK:3690)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Meituan operates as a technology retail company in the People’s Republic of China with a market cap of approximately HK$979.52 billion.

Operations: Meituan generates revenue primarily from two segments: Core Local Commerce (CN¥228.13 billion) and New Initiatives (CN¥77.56 billion).

Insider Ownership: 11.8%

Revenue Growth Forecast: 12.9% p.a.

Meituan, a growth company with high insider ownership in Hong Kong, has shown substantial earnings growth of 175.5% over the past year and is forecast to grow earnings by 26% annually, outpacing the market's average. The company reported H1 2024 sales of CNY 155.53 billion and net income of CNY 16.72 billion. Recent share buybacks totaling HKD 7.17 billion reflect strong internal confidence despite trading at a significant discount to its estimated fair value.

- Navigate through the intricacies of Meituan with our comprehensive analyst estimates report here.

- The valuation report we've compiled suggests that Meituan's current price could be inflated.

Beijing Fourth Paradigm Technology (SEHK:6682)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Beijing Fourth Paradigm Technology Co., Ltd. is an investment holding company that offers platform-centric artificial intelligence (AI) solutions in the People's Republic of China, with a market cap of HK$18.27 billion.

Operations: Revenue segments (in millions of CN¥): Sage Ai Platform: 3000.20, Sagegpt Aigs Services: 448.10, Shift Intelligent Solutions: 1154.20

Insider Ownership: 22.8%

Revenue Growth Forecast: 19.6% p.a.

Beijing Fourth Paradigm Technology, with significant insider ownership, is forecast to become profitable within three years and grow earnings by 102.47% annually. Despite a slower revenue growth rate of 19.6% per year compared to other high-growth firms, the company has been added to the S&P Global BMI Index and reported a narrowed net loss of CNY 151.6 million for H1 2024, down from CNY 456.07 million a year ago.

- Delve into the full analysis future growth report here for a deeper understanding of Beijing Fourth Paradigm Technology.

- According our valuation report, there's an indication that Beijing Fourth Paradigm Technology's share price might be on the expensive side.

Turning Ideas Into Actions

- Unlock our comprehensive list of 47 Fast Growing SEHK Companies With High Insider Ownership by clicking here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Kingdee International Software Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:268

Kingdee International Software Group

An investment holding company, engages in the enterprise resource planning business.

Excellent balance sheet with reasonable growth potential.