Advertisement

Subdued Growth No Barrier To WellCell Holdings Co., Limited (HKG:2477) With Shares Advancing 28%

WellCell Holdings Co., Limited (HKG:2477) shares have had a really impressive month, gaining 28% after a shaky period beforehand. This latest share price bounce rounds out a remarkable 547% gain over the last twelve months.

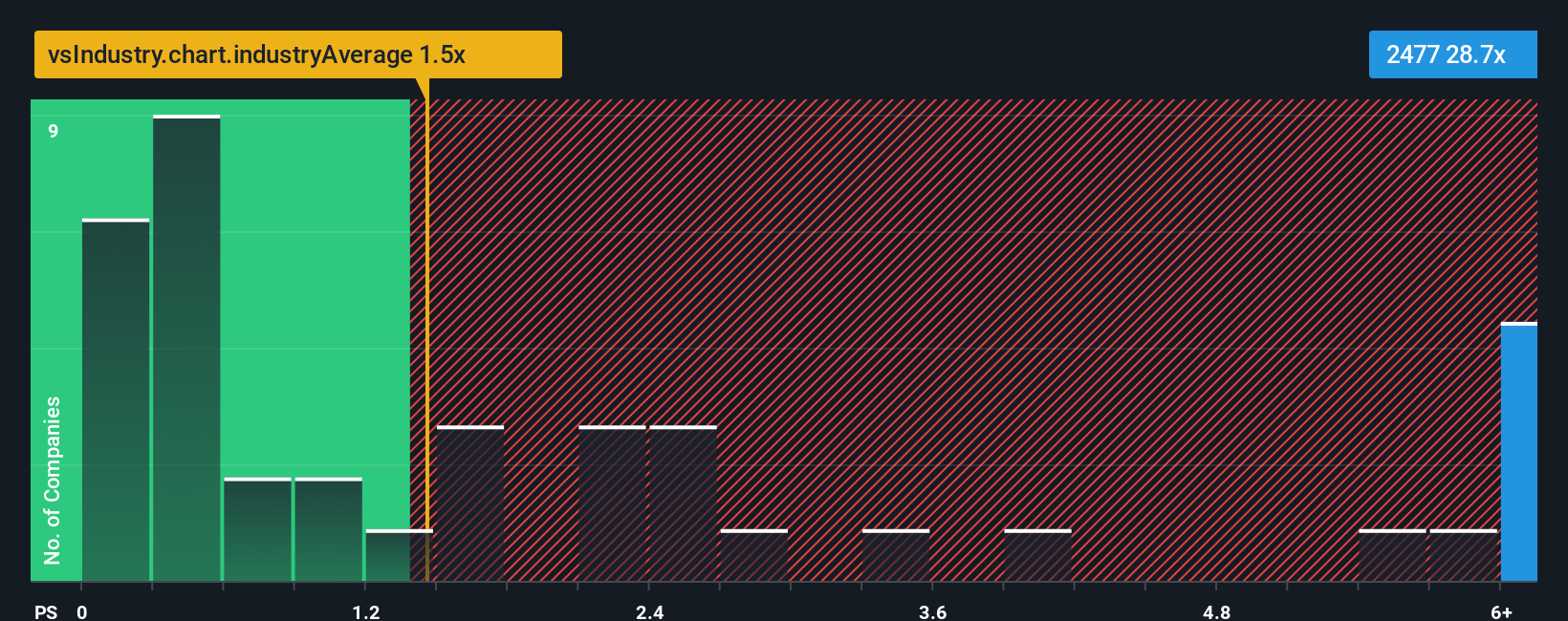

After such a large jump in price, given around half the companies in Hong Kong's IT industry have price-to-sales ratios (or "P/S") below 1.5x, you may consider WellCell Holdings as a stock to avoid entirely with its 28.7x P/S ratio. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for WellCell Holdings

How WellCell Holdings Has Been Performing

The revenue growth achieved at WellCell Holdings over the last year would be more than acceptable for most companies. It might be that many expect the respectable revenue performance to beat most other companies over the coming period, which has increased investors’ willingness to pay up for the stock. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Although there are no analyst estimates available for WellCell Holdings, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.Do Revenue Forecasts Match The High P/S Ratio?

In order to justify its P/S ratio, WellCell Holdings would need to produce outstanding growth that's well in excess of the industry.

Retrospectively, the last year delivered a decent 8.7% gain to the company's revenues. This was backed up an excellent period prior to see revenue up by 37% in total over the last three years. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Weighing that recent medium-term revenue trajectory against the broader industry's one-year forecast for expansion of 9.1% shows it's about the same on an annualised basis.

With this in mind, we find it intriguing that WellCell Holdings' P/S exceeds that of its industry peers. It seems most investors are ignoring the fairly average recent growth rates and are willing to pay up for exposure to the stock. Nevertheless, they may be setting themselves up for future disappointment if the P/S falls to levels more in line with recent growth rates.

The Final Word

The strong share price surge has lead to WellCell Holdings' P/S soaring as well. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

Our examination of WellCell Holdings revealed its three-year revenue trends aren't impacting its high P/S as much as we would have predicted, given they look similar to current industry expectations. Right now we are uncomfortable with the high P/S as this revenue performance isn't likely to support such positive sentiment for long. Unless there is a significant improvement in the company's medium-term trends, it will be difficult to prevent the P/S ratio from declining to a more reasonable level.

It is also worth noting that we have found 2 warning signs for WellCell Holdings that you need to take into consideration.

If you're unsure about the strength of WellCell Holdings' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if WellCell Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:2477

WellCell Holdings

Through its subsidiaries, operates as a telecommunication network support, and information and communication technology (ICT) integration services provider in the People’s Republic of China.

Adequate balance sheet with very low risk.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor