Advertisement

Microware Group (HKG:1985) Will Pay A Smaller Dividend Than Last Year

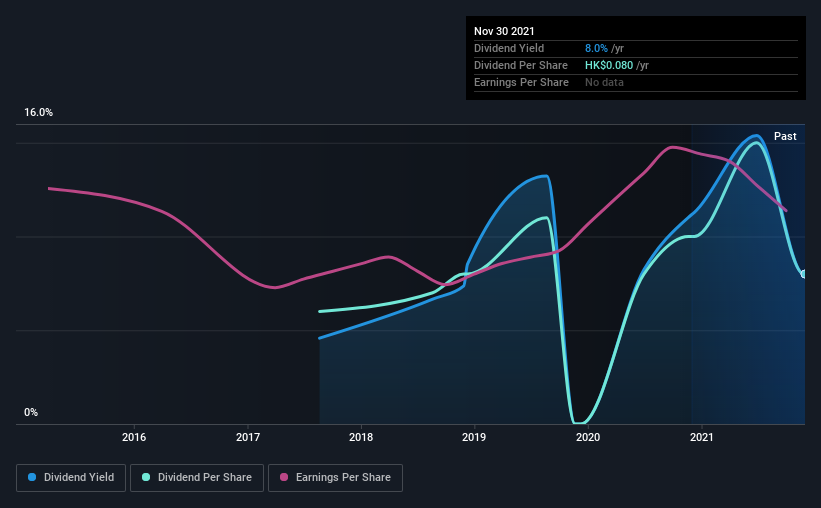

Microware Group Limited (HKG:1985) is reducing its dividend to HK$0.04 on the 30th of December. However, the dividend yield of 14% is still a decent boost to shareholder returns.

Check out our latest analysis for Microware Group

Microware Group Doesn't Earn Enough To Cover Its Payments

We like to see robust dividend yields, but that doesn't matter if the payment isn't sustainable. Prior to this announcement, Microware Group's dividend made up quite a large proportion of earnings but only 29% of free cash flows. This leaves plenty of cash for reinvestment into the business.

Earnings per share could rise by 9.4% over the next year if things go the same way as they have for the last few years. If the dividend continues on its recent course, the payout ratio in 12 months could be 111%, which is a bit high and could start applying pressure to the balance sheet.

Microware Group's Dividend Has Lacked Consistency

The track record isn't the longest, but we are already seeing a bit of instability in the payments. Since 2017, the dividend has gone from HK$0.06 to HK$0.08. This implies that the company grew its distributions at a yearly rate of about 7.5% over that duration. We like to see dividends have grown at a reasonable rate, but with at least one substantial cut in the payments, we're not certain this dividend stock would be ideal for someone intending to live on the income.

We Could See Microware Group's Dividend Growing

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. It's encouraging to see Microware Group has been growing its earnings per share at 9.4% a year over the past five years. Recently, the company has been able to grow earnings at a decent rate, but with the payout ratio on the higher end we don't think the dividend has many prospects for growth.

Microware Group Looks Like A Great Dividend Stock

Overall, we think that Microware Group could be a great option for a dividend investment, although we would have preferred if the dividend wasn't cut this year. Reducing the amount it is paying as a dividend can protect the company's balance sheet, keeping the dividend sustainable for longer. All in all, this checks a lot of the boxes we look for when choosing an income stock.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. However, there are other things to consider for investors when analysing stock performance. Taking the debate a bit further, we've identified 2 warning signs for Microware Group that investors need to be conscious of moving forward. If you are a dividend investor, you might also want to look at our curated list of high performing dividend stock.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:1985

Microware Group

An investment holding company, provides information technology (IT) infrastructure solutions and IT managed services in Hong Kong.

Excellent balance sheet with slight risk.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor