Advertisement

- Hong Kong

- /

- Retail Distributors

- /

- SEHK:8451

Not Many Are Piling Into Sunlight (1977) Holdings Limited (HKG:8451) Stock Yet As It Plummets 32%

Sunlight (1977) Holdings Limited (HKG:8451) shares have retraced a considerable 32% in the last month, reversing a fair amount of their solid recent performance. The drop over the last 30 days has capped off a tough year for shareholders, with the share price down 40% in that time.

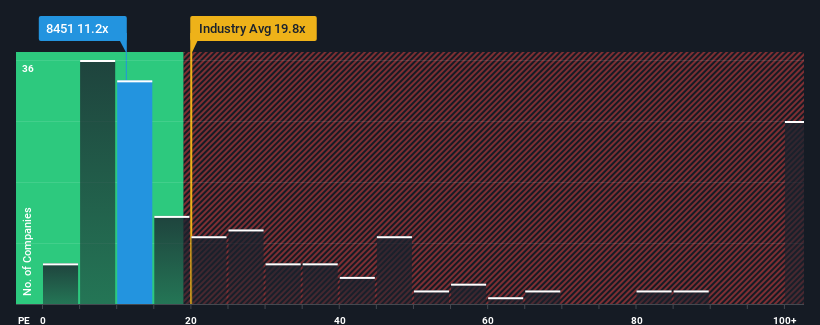

In spite of the heavy fall in price, you could still be forgiven for feeling indifferent about Sunlight (1977) Holdings' P/E ratio of 11.2x, since the median price-to-earnings (or "P/E") ratio in Hong Kong is also close to 9x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/E.

Sunlight (1977) Holdings certainly has been doing a great job lately as it's been growing earnings at a really rapid pace. The P/E is probably moderate because investors think this strong earnings growth might not be enough to outperform the broader market in the near future. If that doesn't eventuate, then existing shareholders have reason to be feeling optimistic about the future direction of the share price.

Check out our latest analysis for Sunlight (1977) Holdings

Does Growth Match The P/E?

In order to justify its P/E ratio, Sunlight (1977) Holdings would need to produce growth that's similar to the market.

If we review the last year of earnings growth, the company posted a terrific increase of 94%. The strong recent performance means it was also able to grow EPS by 356% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Weighing that recent medium-term earnings trajectory against the broader market's one-year forecast for expansion of 21% shows it's noticeably more attractive on an annualised basis.

With this information, we find it interesting that Sunlight (1977) Holdings is trading at a fairly similar P/E to the market. Apparently some shareholders believe the recent performance is at its limits and have been accepting lower selling prices.

What We Can Learn From Sunlight (1977) Holdings' P/E?

Sunlight (1977) Holdings' plummeting stock price has brought its P/E right back to the rest of the market. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

Our examination of Sunlight (1977) Holdings revealed its three-year earnings trends aren't contributing to its P/E as much as we would have predicted, given they look better than current market expectations. When we see strong earnings with faster-than-market growth, we assume potential risks are what might be placing pressure on the P/E ratio. It appears some are indeed anticipating earnings instability, because the persistence of these recent medium-term conditions would normally provide a boost to the share price.

Don't forget that there may be other risks. For instance, we've identified 2 warning signs for Sunlight (1977) Holdings (1 shouldn't be ignored) you should be aware of.

If these risks are making you reconsider your opinion on Sunlight (1977) Holdings, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:8451

Sunlight (1977) Holdings

An investment holding company, supplies tissue products and hygiene related products for corporate customers in Singapore.

Flawless balance sheet with questionable track record.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor