Advertisement

- Hong Kong

- /

- Specialty Stores

- /

- SEHK:6033

Telecom Digital Holdings' (HKG:6033) Upcoming Dividend Will Be Larger Than Last Year's

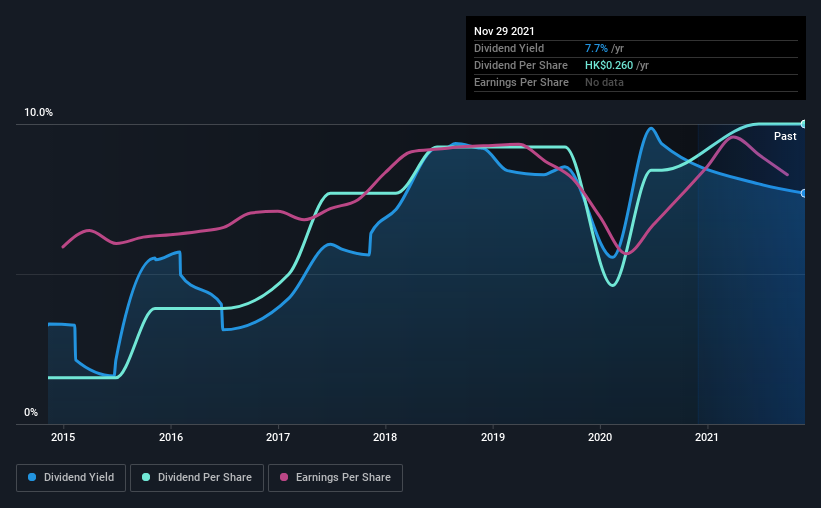

Telecom Digital Holdings Limited's (HKG:6033) dividend will be increasing on the 24th of December to HK$0.07, with investors receiving 17% more than last year. This takes the dividend yield from 7.7% to 8.0%, which shareholders will be pleased with.

Check out our latest analysis for Telecom Digital Holdings

Telecom Digital Holdings Is Paying Out More Than It Is Earning

Impressive dividend yields are good, but this doesn't matter much if the payments can't be sustained. Before this announcement, Telecom Digital Holdings was paying out 93% of earnings, but a comparatively small 60% of free cash flows. Since the dividend is just paying out cash to shareholders, we care more about the cash payout ratio from which we can see plenty is being left over for reinvestment in the business.

Earnings per share could rise by 3.4% over the next year if things go the same way as they have for the last few years. If the dividend continues on its recent course, the payout ratio in 12 months could be 106%, which is a bit high and could start applying pressure to the balance sheet.

Telecom Digital Holdings' Dividend Has Lacked Consistency

Telecom Digital Holdings has been paying dividends for a while, but the track record isn't stellar. If the company cuts once, it definitely isn't argument against the possibility of it cutting in the future. Since 2014, the dividend has gone from HK$0.04 to HK$0.26. This works out to be a compound annual growth rate (CAGR) of approximately 31% a year over that time. Telecom Digital Holdings has grown distributions at a rapid rate despite cutting the dividend at least once in the past. Companies that cut once often cut again, so we would be cautious about buying this stock solely for the dividend income.

The Dividend's Growth Prospects Are Limited

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. Earnings per share has been crawling upwards at 3.4% per year. There are exceptions, but limited earnings growth and a high payout ratio can signal that a company has reached maturity. This isn't the end of the world, but for investors looking for strong dividend growth they may want to look elsewhere.

In Summary

In summary, while it's always good to see the dividend being raised, we don't think Telecom Digital Holdings' payments are rock solid. The payments haven't been particularly stable and we don't see huge growth potential, but with the dividend well covered by cash flows it could prove to be reliable over the short term. We don't think Telecom Digital Holdings is a great stock to add to your portfolio if income is your focus.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. However, there are other things to consider for investors when analysing stock performance. As an example, we've identified 1 warning sign for Telecom Digital Holdings that you should be aware of before investing. Looking for more high-yielding dividend ideas? Try our curated list of strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if Telecom Digital Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:6033

Telecom Digital Holdings

An investment holding company, engages in the telecommunications and related businesses in Hong Kong and the People’s Republic of China.

Medium-low risk established dividend payer.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor