Advertisement

- Hong Kong

- /

- Real Estate

- /

- SEHK:1528

Should You Use Red Star Macalline Group's (HKG:1528) Statutory Earnings To Analyse It?

Broadly speaking, profitable businesses are less risky than unprofitable ones. However, sometimes companies receive a one-off boost (or reduction) to their profit, and it's not always clear whether statutory profits are a good guide, going forward. In this article, we'll look at how useful this year's statutory profit is, when analysing Red Star Macalline Group (HKG:1528).

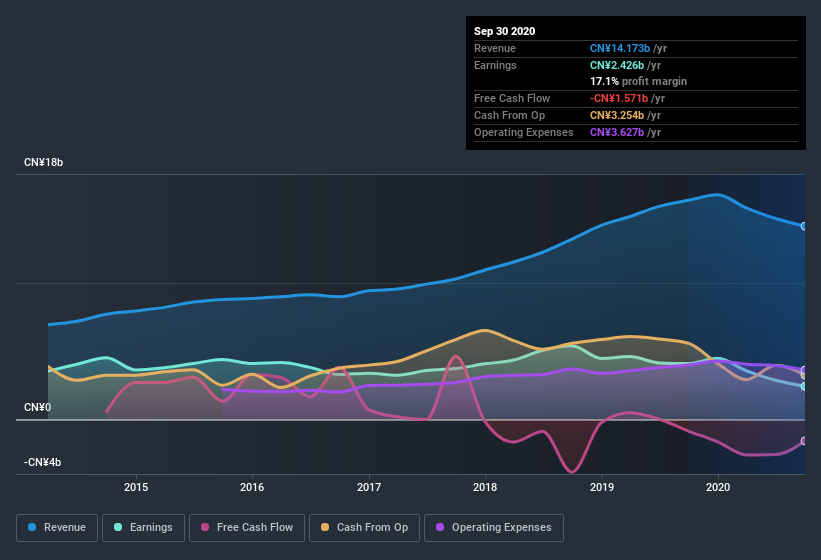

While Red Star Macalline Group was able to generate revenue of CN¥14.2b in the last twelve months, we think its profit result of CN¥2.43b was more important. The chart below shows how it has grown revenue over the last three years, but that profit has declined.

Check out our latest analysis for Red Star Macalline Group

Of course, when it comes to statutory profit, the devil is often in the detail, and we can get a better sense for a company by diving deeper into the financial statements. This article will focus on the impact unusual items have had on Red Star Macalline Group's statutory earnings. That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

How Do Unusual Items Influence Profit?

For anyone who wants to understand Red Star Macalline Group's profit beyond the statutory numbers, it's important to note that during the last twelve months statutory profit gained from CN¥717m worth of unusual items. We can't deny that higher profits generally leave us optimistic, but we'd prefer it if the profit were to be sustainable. When we crunched the numbers on thousands of publicly listed companies, we found that a boost from unusual items in a given year is often not repeated the next year. And that's as you'd expect, given these boosts are described as 'unusual'. If Red Star Macalline Group doesn't see that contribution repeat, then all else being equal we'd expect its profit to drop over the current year.

Our Take On Red Star Macalline Group's Profit Performance

Arguably, Red Star Macalline Group's statutory earnings have been distorted by unusual items boosting profit. Therefore, it seems possible to us that Red Star Macalline Group's true underlying earnings power is actually less than its statutory profit. Sadly, its EPS was down over the last twelve months. At the end of the day, it's essential to consider more than just the factors above, if you want to understand the company properly. So while earnings quality is important, it's equally important to consider the risks facing Red Star Macalline Group at this point in time. To that end, you should learn about the 4 warning signs we've spotted with Red Star Macalline Group (including 1 which is a bit concerning).

This note has only looked at a single factor that sheds light on the nature of Red Star Macalline Group's profit. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

If you’re looking to trade Red Star Macalline Group, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:1528

Reasonable growth potential and fair value.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.8% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor