- Hong Kong

- /

- Real Estate

- /

- SEHK:1972

Swire Properties' (HKG:1972) Shareholders Will Receive A Bigger Dividend Than Last Year

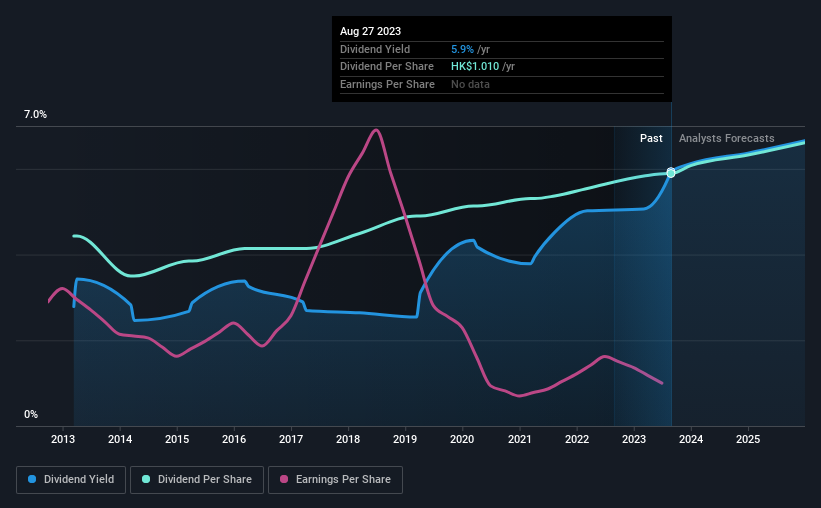

Swire Properties Limited (HKG:1972) has announced that it will be increasing its dividend from last year's comparable payment on the 12th of October to HK$0.33. Based on this payment, the dividend yield for the company will be 5.9%, which is fairly typical for the industry.

Check out our latest analysis for Swire Properties

Swire Properties' Payment Has Solid Earnings Coverage

We like a dividend to be consistent over the long term, so checking whether it is sustainable is important. Based on the last payment, the company wasn't making enough to cover what it was paying to shareholders. Without profits and cash flows increasing, it would be difficult for the company to continue paying the dividend at this level.

Over the next year, EPS is forecast to expand by 75.8%. Under the assumption that the dividend will continue along recent trends, we think the payout ratio could be 61% which would be quite comfortable going to take the dividend forward.

Dividend Volatility

Although the company has a long dividend history, it has been cut at least once in the last 10 years. The annual payment during the last 10 years was HK$0.76 in 2013, and the most recent fiscal year payment was HK$1.01. This means that it has been growing its distributions at 2.9% per annum over that time. It's encouraging to see some dividend growth, but the dividend has been cut at least once, and the size of the cut would eliminate most of the growth anyway, which makes this less attractive as an income investment.

Dividend Growth Potential Is Shaky

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. Over the past five years, it looks as though Swire Properties' EPS has declined at around 32% a year. Dividend payments are likely to come under some pressure unless EPS can pull out of the nosedive it is in. Over the next year, however, earnings are actually predicted to rise, but we would still be cautious until a track record of earnings growth can be built.

We're Not Big Fans Of Swire Properties' Dividend

In summary, investors will like to be receiving a higher dividend, but we have some questions about whether it can be sustained over the long term. The company isn't making enough to be paying as much as it is, and the other factors don't look particularly promising either. Overall, the dividend is not reliable enough to make this a good income stock.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. However, there are other things to consider for investors when analysing stock performance. Case in point: We've spotted 2 warning signs for Swire Properties (of which 1 makes us a bit uncomfortable!) you should know about. Is Swire Properties not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1972

Swire Properties

Develops, owns, and operates mixed-use, primarily commercial properties in Hong Kong, Mainland China, the United States, and internationally.

Reasonable growth potential second-rate dividend payer.