Advertisement

- Hong Kong

- /

- Real Estate

- /

- SEHK:1862

Health Check: How Prudently Does Jingrui Holdings (HKG:1862) Use Debt?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Jingrui Holdings Limited (HKG:1862) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Jingrui Holdings

How Much Debt Does Jingrui Holdings Carry?

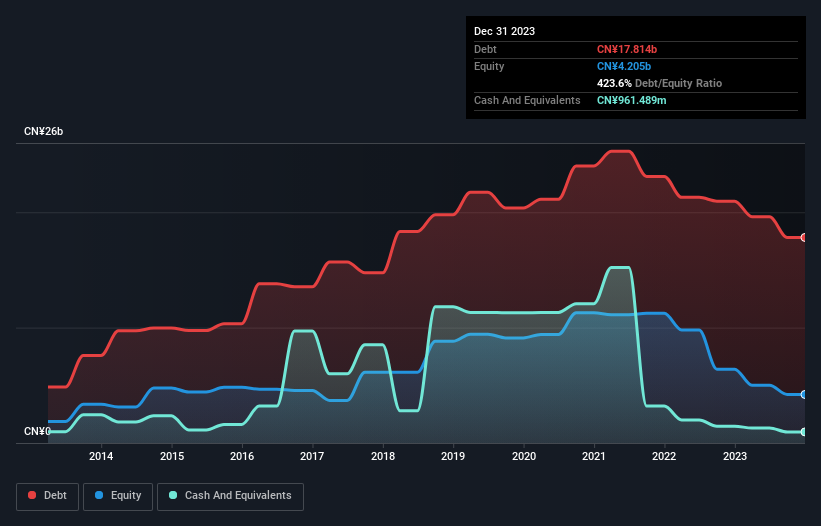

As you can see below, Jingrui Holdings had CN¥17.8b of debt at December 2023, down from CN¥21.0b a year prior. However, because it has a cash reserve of CN¥961.5m, its net debt is less, at about CN¥16.9b.

How Healthy Is Jingrui Holdings' Balance Sheet?

The latest balance sheet data shows that Jingrui Holdings had liabilities of CN¥29.7b due within a year, and liabilities of CN¥5.60b falling due after that. Offsetting these obligations, it had cash of CN¥961.5m as well as receivables valued at CN¥7.51b due within 12 months. So it has liabilities totalling CN¥26.8b more than its cash and near-term receivables, combined.

The deficiency here weighs heavily on the CN¥39.5m company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we'd watch its balance sheet closely, without a doubt. After all, Jingrui Holdings would likely require a major re-capitalisation if it had to pay its creditors today. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Jingrui Holdings's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Over 12 months, Jingrui Holdings made a loss at the EBIT level, and saw its revenue drop to CN¥7.3b, which is a fall of 7.8%. That's not what we would hope to see.

Caveat Emptor

Over the last twelve months Jingrui Holdings produced an earnings before interest and tax (EBIT) loss. Its EBIT loss was a whopping CN¥605m. Reflecting on this and the significant total liabilities, it's hard to know what to say about the stock because of our intense dis-affinity for it. Like every long-shot we're sure it has a glossy presentation outlining its blue-sky potential. But the reality is that it is low on liquid assets relative to liabilities, and it lost CN¥1.7b in the last year. So we think buying this stock is risky. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For example - Jingrui Holdings has 3 warning signs we think you should be aware of.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1862

Jingrui Holdings

An investment holding company, engages in development, investment, and management of real estate properties in the People’s Republic of China.

Moderate risk and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor