Stock Analysis

- Hong Kong

- /

- Real Estate

- /

- SEHK:173

K Wah International Holdings And Two Other Undervalued Small Caps With Insider Action In Hong Kong

Reviewed by Simply Wall St

Amid a backdrop of fluctuating global markets, Hong Kong's small-cap stocks have shown resilience, with the Hang Seng Index recently experiencing a notable uptick. This environment may present opportunities for investors to explore undervalued entities that could benefit from current economic dynamics. In identifying promising small-cap stocks, factors such as insider buying can be indicative of confidence in the company's prospects by those who know it best.

Top 10 Undervalued Small Caps With Insider Buying In Hong Kong

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Ferretti | 11.3x | 0.8x | 45.56% | ★★★★★☆ |

| Wasion Holdings | 11.3x | 0.8x | 32.80% | ★★★★☆☆ |

| China Overseas Grand Oceans Group | 2.7x | 0.1x | -0.22% | ★★★★☆☆ |

| Nissin Foods | 14.4x | 1.3x | 41.16% | ★★★★☆☆ |

| Kinetic Development Group | 3.9x | 1.7x | 21.92% | ★★★★☆☆ |

| Transport International Holdings | 11.6x | 0.6x | 43.88% | ★★★★☆☆ |

| China Leon Inspection Holding | 10.2x | 0.7x | 24.84% | ★★★★☆☆ |

| Skyworth Group | 5.7x | 0.1x | -315.33% | ★★★☆☆☆ |

| Ever Sunshine Services Group | 6.0x | 0.4x | 7.49% | ★★★☆☆☆ |

| Shenzhen International Holdings | 8.0x | 0.7x | 14.38% | ★★★☆☆☆ |

Let's review some notable picks from our screened stocks.

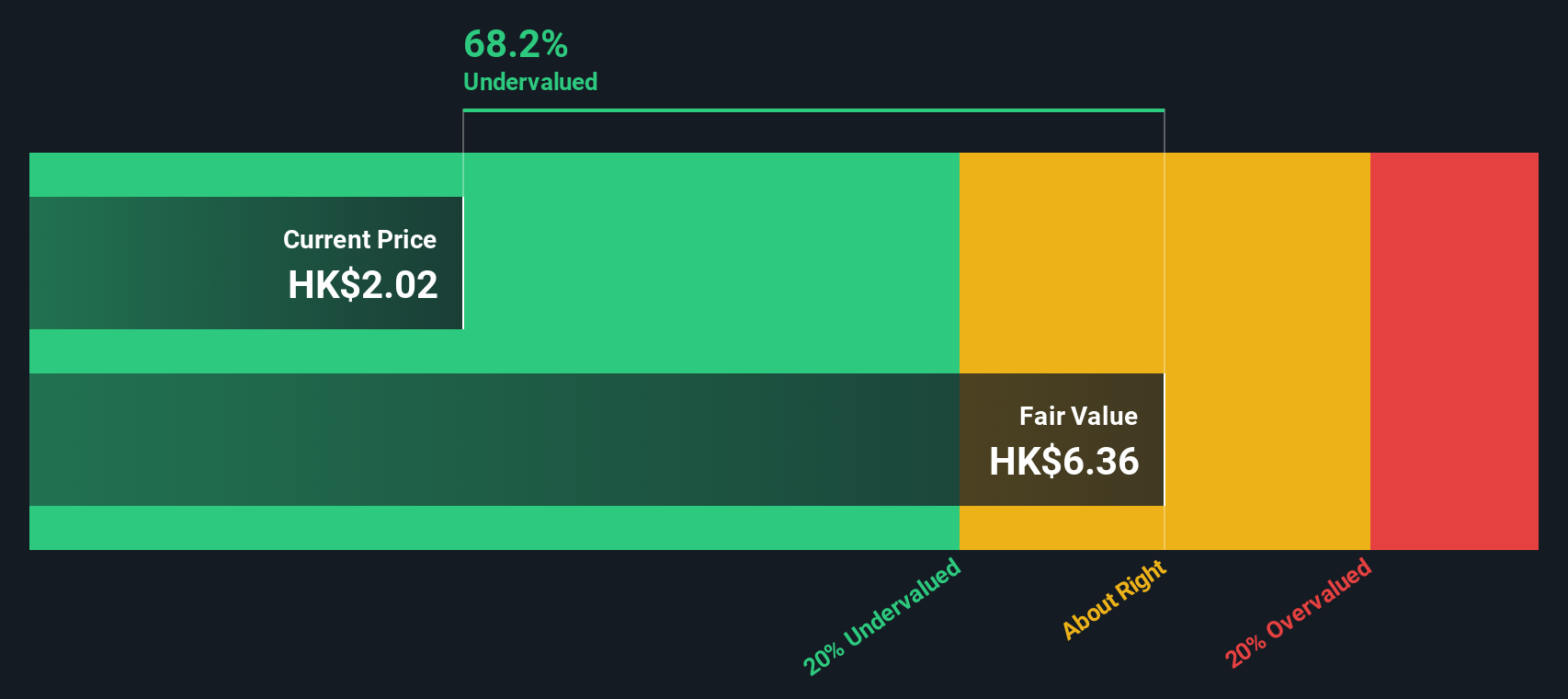

K. Wah International Holdings (SEHK:173)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: K. Wah International Holdings is a company engaged in property development in Hong Kong and Mainland China, as well as property investment, with a market capitalization of approximately HK$5.1 billion.

Operations: The company generates significant revenue from property development in Mainland China, contributing HK$4.45 billion, followed by Hong Kong at HK$918.77 million, with additional earnings from property investment amounting to HK$637.17 million. It reported a gross profit margin of 33.07% as of the latest period, reflecting its cost management in relation to sales revenue generated from these segments.

PE: 7.2x

Recently, K. Wah International Holdings demonstrated insider confidence, with Mo Chi Cheng purchasing 200,000 shares, signaling a strong belief in the company's prospects. This Hong Kong-based entity is noted for its modest market cap and appealing price metrics compared to industry peers. Despite a dividend decrease announced on June 26, 2024, the firm's earnings are expected to grow annually by 8.63%. These elements suggest that K. Wah could be poised for future growth amidst its current market position.

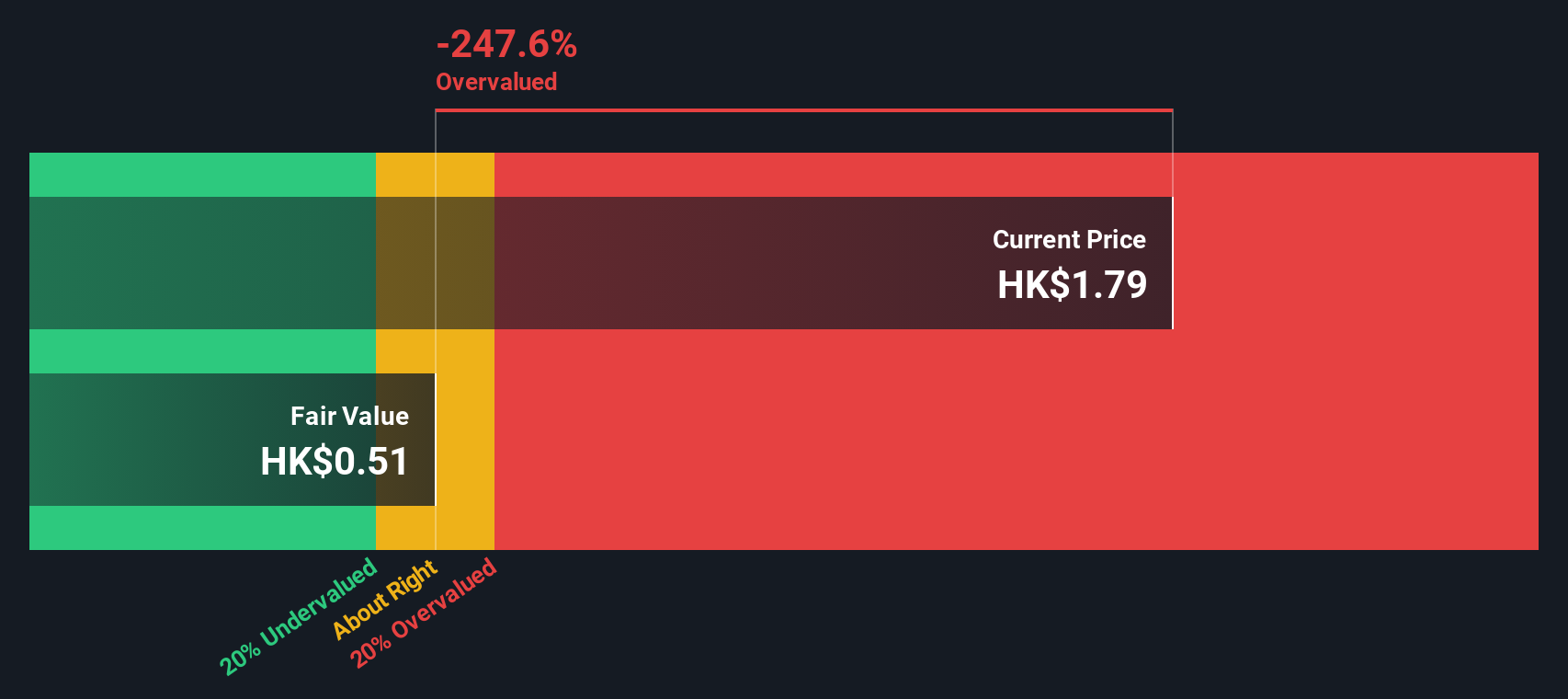

Comba Telecom Systems Holdings (SEHK:2342)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Comba Telecom Systems Holdings specializes in providing wireless telecommunications network system equipment and services, primarily serving operators in the telecommunications sector.

Operations: The company generates significant revenue from wireless telecommunications network system equipment and services, totaling HK$5.82 billion, compared to HK$157.83 million from operator telecommunication services. Its gross profit margin has shown a trend of fluctuation but was noted at 27.79% by the end of the most recent period reported.

PE: 356.8x

Recently, Tung Ling Fok increased their stake in Comba Telecom Systems Holdings by purchasing 1.83 million shares, signaling insider confidence amid a volatile market where the share price has fluctuated significantly over the past three months. Despite low profit margins currently at 0.1%, down from last year's 3%, and financial results impacted by one-off items, the company’s presence at significant industry events like MWC Shanghai suggests ongoing strategic initiatives to bolster its market position. This move aligns with shareholder-approved plans to enhance value through share repurchases funded from cash flows, underscoring a proactive approach to capital management and potential future growth prospects.

China Overseas Grand Oceans Group (SEHK:81)

Simply Wall St Value Rating: ★★★★☆☆

Overview: China Overseas Grand Oceans Group operates primarily in property investment and development, with additional activities in property leasing and other sectors, boasting a market cap of approximately CN¥14.37 billion.

Operations: The company's primary revenue is generated from property investment and development, contributing CN¥56.08 billion, supplemented by property leasing at CN¥0.24 billion. Over recent periods, the gross profit margin has shown a notable increase, peaking at 33.82% in mid-2019 before settling to 13.91% by the end of 2023.

PE: 2.7x

Despite a challenging environment with declining property sales and earnings forecasted to drop by 2.5% annually over the next three years, China Overseas Grand Oceans Group has demonstrated insider confidence through recent share purchases. This action suggests a belief in the company's resilience and potential upside among those closest to its operations. With significant shifts in executive roles and auditor changes signaling strategic adjustments, the firm appears poised for a recalibration of its financial strategies amidst ongoing market pressures.

- Get an in-depth perspective on China Overseas Grand Oceans Group's performance by reading our valuation report here.

Learn about China Overseas Grand Oceans Group's historical performance.

Turning Ideas Into Actions

- Dive into all 18 of the Undervalued SEHK Small Caps With Insider Buying we have identified here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if K. Wah International Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:173

K. Wah International Holdings

An investment holding company, engages in the property development and investment businesses in Hong Kong and Mainland China.

Excellent balance sheet established dividend payer.