- Hong Kong

- /

- Real Estate

- /

- SEHK:173

3 SEHK Stocks That Could Be Up To 38.9% Below Intrinsic Value Estimates

Reviewed by Simply Wall St

The Hong Kong market has experienced a mix of caution and optimism recently, with the Hang Seng Index advancing despite global economic uncertainties. In this environment, identifying undervalued stocks can be particularly rewarding for investors looking to capitalize on potential market inefficiencies. A good stock in such conditions often exhibits strong fundamentals and is trading below its intrinsic value, offering a margin of safety.

Top 10 Undervalued Stocks Based On Cash Flows In Hong Kong

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Best Pacific International Holdings (SEHK:2111) | HK$2.37 | HK$4.34 | 45.4% |

| ANTA Sports Products (SEHK:2020) | HK$71.65 | HK$135.96 | 47.3% |

| BYD Electronic (International) (SEHK:285) | HK$30.25 | HK$53.35 | 43.3% |

| Tencent Holdings (SEHK:700) | HK$381.80 | HK$761.31 | 49.8% |

| Inspur Digital Enterprise Technology (SEHK:596) | HK$3.22 | HK$5.70 | 43.5% |

| WuXi XDC Cayman (SEHK:2268) | HK$19.82 | HK$39.19 | 49.4% |

| Pacific Textiles Holdings (SEHK:1382) | HK$1.52 | HK$2.85 | 46.6% |

| iDreamSky Technology Holdings (SEHK:1119) | HK$2.17 | HK$4.14 | 47.6% |

| Jinke Smart Services Group (SEHK:9666) | HK$7.75 | HK$13.96 | 44.5% |

| Chervon Holdings (SEHK:2285) | HK$18.94 | HK$35.81 | 47.1% |

Let's dive into some prime choices out of the screener.

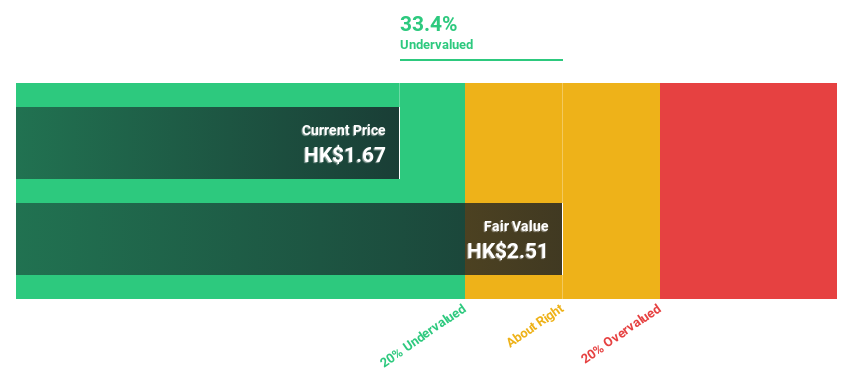

Zhou Hei Ya International Holdings (SEHK:1458)

Overview: Zhou Hei Ya International Holdings Company Limited (SEHK:1458) is an investment holding company that produces, markets, and retails casual braised food in the People’s Republic of China, with a market cap of HK$3.29 billion.

Operations: The company's revenue segments include the production, marketing, and retailing of casual braised duck-related food, generating CN¥2.59 billion.

Estimated Discount To Fair Value: 11.2%

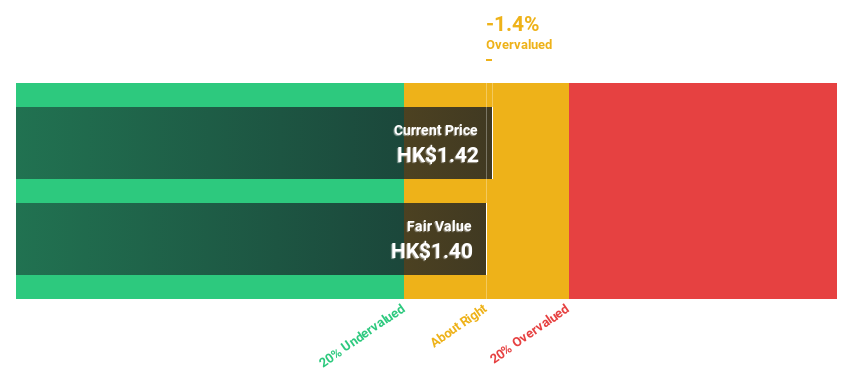

Zhou Hei Ya International Holdings reported half-year sales of CNY 1.26 billion, down from CNY 1.41 billion a year ago, with net income dropping to CNY 32.91 million from CNY 101.74 million. The company's recent earnings guidance aligns with these results, citing increased operational expenses and fair value changes in associates as key factors. Despite lower profit margins and no interim dividend, the stock trades below its estimated fair value of HK$1.68 at HK$1.49, indicating potential undervaluation based on cash flows.

- According our earnings growth report, there's an indication that Zhou Hei Ya International Holdings might be ready to expand.

- Dive into the specifics of Zhou Hei Ya International Holdings here with our thorough financial health report.

K. Wah International Holdings (SEHK:173)

Overview: K. Wah International Holdings Limited, with a market cap of HK$5.52 billion, is an investment holding company involved in property development and investment in Hong Kong and Mainland China.

Operations: K. Wah International Holdings Limited generates revenue from property development in Hong Kong (HK$669.98 million), property development in Mainland China (HK$2.81 billion), and property investment (HK$634.10 million).

Estimated Discount To Fair Value: 31.4%

K. Wah International Holdings reported half-year sales of HK$1.21 billion, down from HK$3.10 billion a year ago, with net income falling to HK$153.79 million from HK$481.91 million. Despite this decline, the stock trades at 31% below its estimated fair value and is significantly undervalued based on discounted cash flow analysis (HK$1.74 vs fair value of HK$2.54). However, the company has an unstable dividend track record and recent earnings have decreased substantially.

- In light of our recent growth report, it seems possible that K. Wah International Holdings' financial performance will exceed current levels.

- Navigate through the intricacies of K. Wah International Holdings with our comprehensive financial health report here.

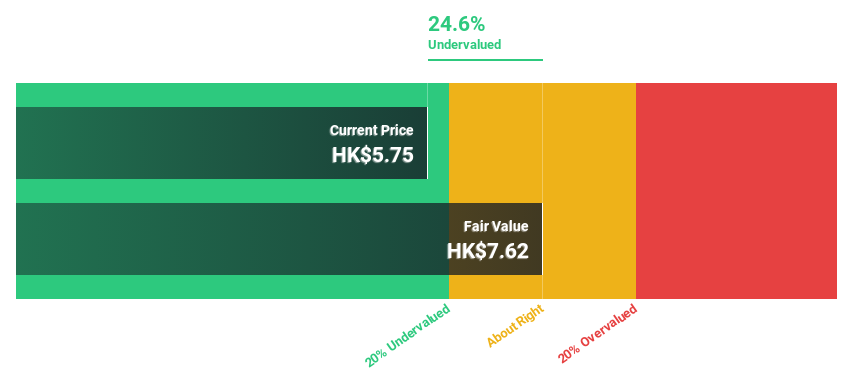

CIMC Enric Holdings (SEHK:3899)

Overview: CIMC Enric Holdings Limited provides transportation, storage, and processing equipment and services for the clean energy, chemicals, environmental, and liquid food sectors worldwide with a market cap of HK$12.78 billion.

Operations: The company's revenue segments include CN¥16.49 billion from Clean Energy, CN¥4.59 billion from Liquid Food, and CN¥3.31 billion from Chemical and Environmental sectors.

Estimated Discount To Fair Value: 38.9%

CIMC Enric Holdings is trading at HK$6.36, significantly below its estimated fair value of HK$10.40, suggesting it is highly undervalued based on discounted cash flow analysis. Despite a recent dip in net income to CNY 486.14 million for the first half of 2024 from CNY 568.67 million a year ago, earnings are forecast to grow significantly at 21.2% per year, outpacing the Hong Kong market's average growth rate of 10.9%.

- Our expertly prepared growth report on CIMC Enric Holdings implies its future financial outlook may be stronger than recent results.

- Click here and access our complete balance sheet health report to understand the dynamics of CIMC Enric Holdings.

Turning Ideas Into Actions

- Click here to access our complete index of 35 Undervalued SEHK Stocks Based On Cash Flows.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if K. Wah International Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:173

K. Wah International Holdings

An investment holding company, engages in the property development and investment businesses in Hong Kong and Mainland China.

Excellent balance sheet with reasonable growth potential.