Shanghai Henlius Biotech (SEHK:2696) shares have seen some movement recently, prompting investors to take a closer look at the company’s recent performance. A quick glance shows mixed returns over the past month and quarter.

Shanghai Henlius Biotech’s share price has cooled off lately, but momentum over the past year has been exceptional. The company delivered a 225% total shareholder return, which signals strong growth sentiment and renewed investor confidence. Even with a recent dip, long-term performance suggests optimism about the company’s prospects remains intact.

If the rapid rise of Henlius got your attention, now is a great moment to broaden your search and discover See the full list for free.

With Henlius shares trading at a significant discount to analyst targets and recent growth in revenue and net income, investors may wonder whether there is still value to be found or if the market has already factored in its future potential.

Advertisement

Price-to-Earnings of 40.3x: Is it justified?

Currently, Shanghai Henlius Biotech trades at a price-to-earnings (P/E) ratio of 40.3x, which puts it above both its peer average and the broader sector. With the last close at HK$67 and a peer P/E ratio averaging 38.9x, investors are left to gauge whether a premium valuation is sustainable given the company’s fundamentals and growth profile.

The price-to-earnings ratio reflects how much investors are willing to pay for each dollar of company earnings. In the biotech sector, higher multiples can sometimes be justified if markets expect breakthroughs or rapid expansion. However, elevated ratios often spark questions about growth momentum versus risk.

For Henlius, the multiple stands out as particularly expensive compared to both market peers (38.9x) and the Asian Biotechs industry average (39.7x). It is also above the estimated fair P/E of 23.4x, suggesting the market may be aggressively pricing in future results or underestimating competitive risks. This gap to a lower fair ratio signals potential for the market to adjust expectations if growth does not accelerate as anticipated.

However, slowing revenue and net income growth, along with a recent decline in share price, could present challenges to the case for continued outperformance.

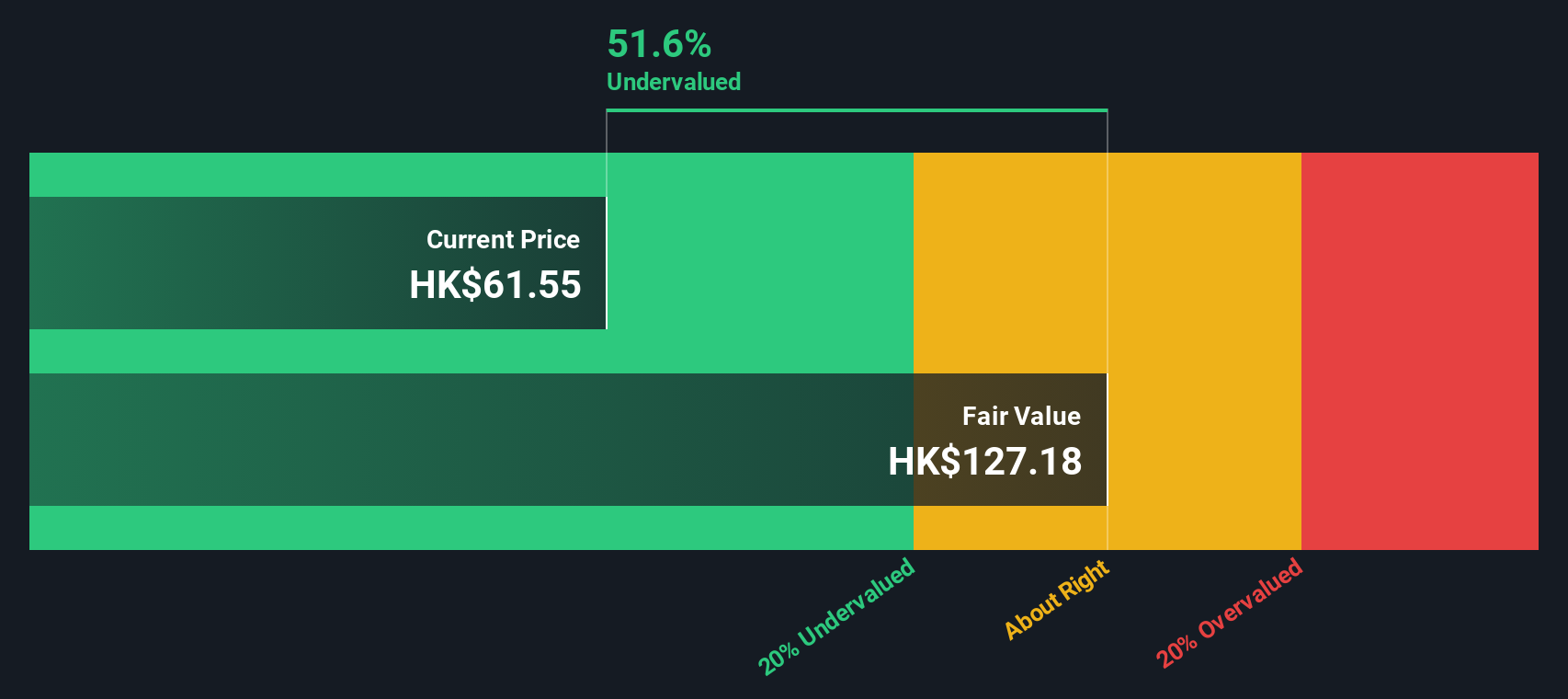

There is another way to look at Shanghai Henlius Biotech’s value. According to our DCF model, the shares are trading 47% below their estimated fair value. This suggests that, despite a high price-to-earnings ratio, the market may be underestimating Henlius’ future cash flow potential.

Investors curious to dig deeper or craft an analysis that reflects their own perspective can build a personalized view in just a few minutes. Do it your way

A great starting point for your Shanghai Henlius Biotech research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Don’t let promising opportunities slip away. Use our tailored screeners to find standout stocks with potential that may not be on your radar yet.

Tap into the future by spotting market innovators among these 26 AI penny stocks, using artificial intelligence to disrupt entire industries and set trends.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks