- Hong Kong

- /

- Hospitality

- /

- SEHK:3690

3 SEHK Growth Companies With Up To 30% Insider Ownership

Reviewed by Simply Wall St

The Hong Kong market has seen a significant boost following China's recent announcement of robust stimulus measures, lifting investor sentiment and driving gains across major indices. This positive economic backdrop provides an opportune moment to explore growth companies with substantial insider ownership, as such stocks often indicate strong confidence from those closest to the company's operations.

Top 10 Growth Companies With High Insider Ownership In Hong Kong

| Name | Insider Ownership | Earnings Growth |

| Laopu Gold (SEHK:6181) | 36.4% | 32.7% |

| Akeso (SEHK:9926) | 20.5% | 54.5% |

| Fenbi (SEHK:2469) | 33.1% | 22.4% |

| Zylox-Tonbridge Medical Technology (SEHK:2190) | 18.8% | 69.8% |

| Pacific Textiles Holdings (SEHK:1382) | 11.2% | 37.7% |

| Zhejiang Leapmotor Technology (SEHK:9863) | 15% | 78.9% |

| DPC Dash (SEHK:1405) | 38.1% | 104.2% |

| Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) | 13.9% | 109.2% |

| Beijing Airdoc Technology (SEHK:2251) | 29.1% | 93.4% |

| Lianlian DigiTech (SEHK:2598) | 19.7% | 92.3% |

We're going to check out a few of the best picks from our screener tool.

BYD (SEHK:1211)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: BYD Company Limited, with a market cap of HK$927.40 billion, operates in the automobiles and batteries business across China, Hong Kong, Macau, Taiwan, and internationally.

Operations: BYD's revenue segments include CN¥507.52 billion from Automobiles and Related Products and Other Products, and CN¥154.49 billion from Mobile Handset Components, Assembly Service, and Other Products.

Insider Ownership: 30.1%

BYD has seen robust growth in production and sales volumes, with recent figures showing significant year-over-year increases. The company's revenue and net income for the first half of 2024 also grew substantially. The strategic partnership with Uber to introduce 100,000 new electric vehicles globally highlights BYD's expansion efforts. Despite its high valuation, BYD is trading below its estimated fair value and has strong insider ownership, which aligns management's interests with shareholders’.

- Click here and access our complete growth analysis report to understand the dynamics of BYD.

- According our valuation report, there's an indication that BYD's share price might be on the expensive side.

China Ruyi Holdings (SEHK:136)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: China Ruyi Holdings Limited is an investment holding company involved in content production and online streaming across the People's Republic of China, Hong Kong, Europe, and internationally, with a market cap of HK$28.26 billion.

Operations: The company's revenue segments include CN¥1.63 billion from content production and CN¥3.01 billion from online streaming and gaming businesses.

Insider Ownership: 15.1%

China Ruyi Holdings is forecasted to grow earnings at 17.57% annually, outpacing the Hong Kong market's average. Despite a substantial increase in sales to CNY 1.84 billion for H1 2024, the company reported a net loss of CNY 114.65 million, though this is an improvement from the previous year's loss. Trading at a significant discount to its estimated fair value and with high insider ownership, it shows potential for growth but faces profitability challenges.

- Click here to discover the nuances of China Ruyi Holdings with our detailed analytical future growth report.

- Upon reviewing our latest valuation report, China Ruyi Holdings' share price might be too optimistic.

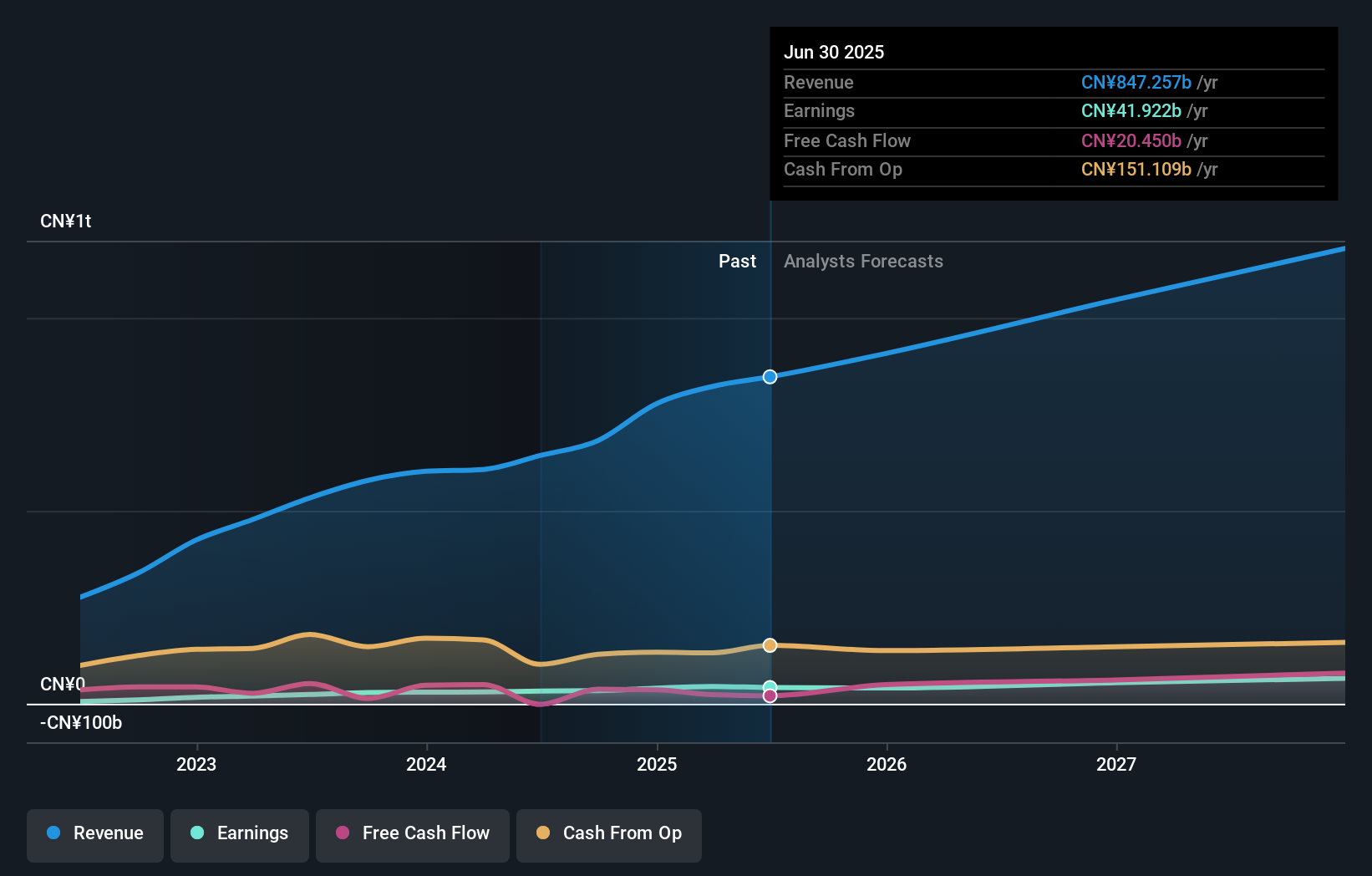

Meituan (SEHK:3690)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Meituan is a technology retail company in the People’s Republic of China with a market cap of approximately HK$1.02 trillion.

Operations: The company's revenue segments include CN¥228.13 billion from Core Local Commerce and CN¥77.56 billion from New Initiatives.

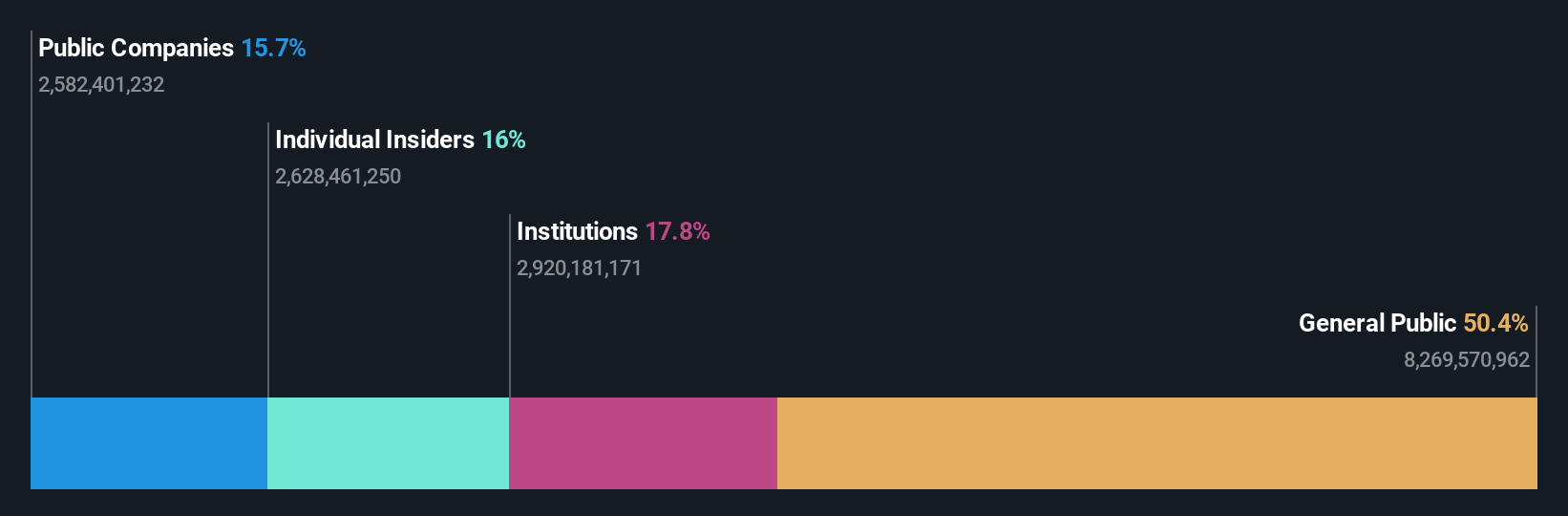

Insider Ownership: 11.8%

Meituan, a growth company with high insider ownership, has demonstrated strong financial performance, reporting half-year sales of CNY 155.53 billion and net income of CNY 16.72 billion. Earnings per share have more than doubled year-over-year. The company's aggressive share repurchase program, totaling HKD 7.17 billion in recent buybacks, underscores management's confidence in its future prospects. Despite this, insider buying has not been substantial recently and the stock trades significantly below its estimated fair value.

- Navigate through the intricacies of Meituan with our comprehensive analyst estimates report here.

- Our valuation report unveils the possibility Meituan's shares may be trading at a premium.

Seize The Opportunity

- Click here to access our complete index of 48 Fast Growing SEHK Companies With High Insider Ownership.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:3690

Meituan

Operates as a technology retail company in the People’s Republic of China.

Solid track record with excellent balance sheet.