Advertisement

- Hong Kong

- /

- Paper and Forestry Products

- /

- SEHK:723

Is There More Growth In Store For Reliance Global Holdings' (HKG:723) Returns On Capital?

What are the early trends we should look for to identify a stock that could multiply in value over the long term? Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. Speaking of which, we noticed some great changes in Reliance Global Holdings' (HKG:723) returns on capital, so let's have a look.

What is Return On Capital Employed (ROCE)?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. To calculate this metric for Reliance Global Holdings, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

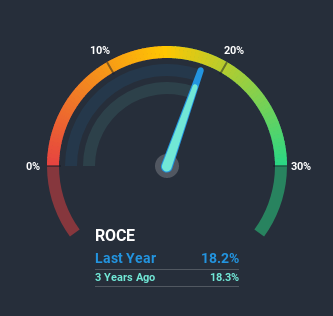

0.18 = HK$50m ÷ (HK$557m - HK$284m) (Based on the trailing twelve months to September 2020).

Therefore, Reliance Global Holdings has an ROCE of 18%. On its own, that's a standard return, however it's much better than the 8.9% generated by the Forestry industry.

Check out our latest analysis for Reliance Global Holdings

Historical performance is a great place to start when researching a stock so above you can see the gauge for Reliance Global Holdings' ROCE against it's prior returns. If you're interested in investigating Reliance Global Holdings' past further, check out this free graph of past earnings, revenue and cash flow.

What Can We Tell From Reliance Global Holdings' ROCE Trend?

Reliance Global Holdings has broken into the black (profitability) and we're sure it's a sight for sore eyes. The company was generating losses five years ago, but has managed to turn it around and as we saw earlier is now earning 18%, which is always encouraging. On top of that, what's interesting is that the amount of capital being employed has remained steady, so the business hasn't needed to put any additional money to work to generate these higher returns. That being said, while an increase in efficiency is no doubt appealing, it'd be helpful to know if the company does have any investment plans going forward. Because in the end, a business can only get so efficient.

On a side note, we noticed that the improvement in ROCE appears to be partly fueled by an increase in current liabilities. The current liabilities has increased to 51% of total assets, so the business is now more funded by the likes of its suppliers or short-term creditors. And with current liabilities at those levels, that's pretty high.

The Bottom Line

To bring it all together, Reliance Global Holdings has done well to increase the returns it's generating from its capital employed. Although the company may be facing some issues elsewhere since the stock has plunged 80% in the last five years. Regardless, we think the underlying fundamentals warrant this stock for further investigation.

One final note, you should learn about the 2 warning signs we've spotted with Reliance Global Holdings (including 1 which is a bit concerning) .

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

When trading Reliance Global Holdings or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:723

Reliance Global Holdings

An investment holding company, engages in the forest-related business in China, Hong Kong, rest of Asia, Europe, and the Middle East.

Flawless balance sheet with low risk.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|27.7% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.2% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.4% undervalued

DA

Community Contributor