Advertisement

- Hong Kong

- /

- Metals and Mining

- /

- SEHK:3939

A Look at Wanguo Gold Group (SEHK:3939) Valuation Following Gold Ridge Mine Feasibility Study Release

Simply Wall St

Reviewed by Simply Wall St

Wanguo Gold Group (SEHK:3939) just released a thorough summary of the Gold Ridge Mine feasibility study in the Solomon Islands, outlining both geology and resource estimates. The project’s scale and development prospects present intriguing implications for shareholders.

See our latest analysis for Wanguo Gold Group.

Wanguo Gold Group’s recent announcement about the Gold Ridge Mine has sparked renewed investor enthusiasm, with the share price rallying 5.08% in just one day and climbing more than 177% year-to-date. Short-term momentum is building on the back of this positive news, while the company’s remarkable 1-year total shareholder return of 175% and multi-year gains suggest sustained confidence in its long-term outlook.

If you’re looking to broaden your investment universe as news shakes up the gold mining sector, it’s a great chance to discover fast growing stocks with high insider ownership

The stage is set for a closer look at Wanguo Gold Group’s valuation. However, does the current surge leave room for upside, or are expectations for future growth already built into the stock price?

Price-to-Earnings of 34.9x: Is it justified?

Wanguo Gold Group trades at a price-to-earnings (P/E) ratio of 34.9x, notably higher than both its sector and peer averages, putting its current valuation in the spotlight.

The price-to-earnings ratio is a widely used measure that values a company relative to its earnings. For gold miners like Wanguo Gold Group, investors often track this multiple to gauge how much future profit growth is already reflected in the share price.

With a P/E of 34.9x, Wanguo Gold Group is priced significantly above the broader Hong Kong Metals and Mining industry average of 15x, and also compared to its peers' average of 20.1x. The stock's ratio also exceeds the estimated Fair Price-to-Earnings Ratio of 20.6x. This suggests that market optimism is elevated, and a re-rating could occur if growth does not meet expectations.

Explore the SWS fair ratio for Wanguo Gold Group

Result: Price-to-Earnings of 34.9x (OVERVALUED)

However, slowing momentum or a downturn in gold prices could quickly reverse sentiment. This serves as a reminder to investors that current optimism may be vulnerable to shifting market conditions.

Find out about the key risks to this Wanguo Gold Group narrative.

Another View: What Does the DCF Say?

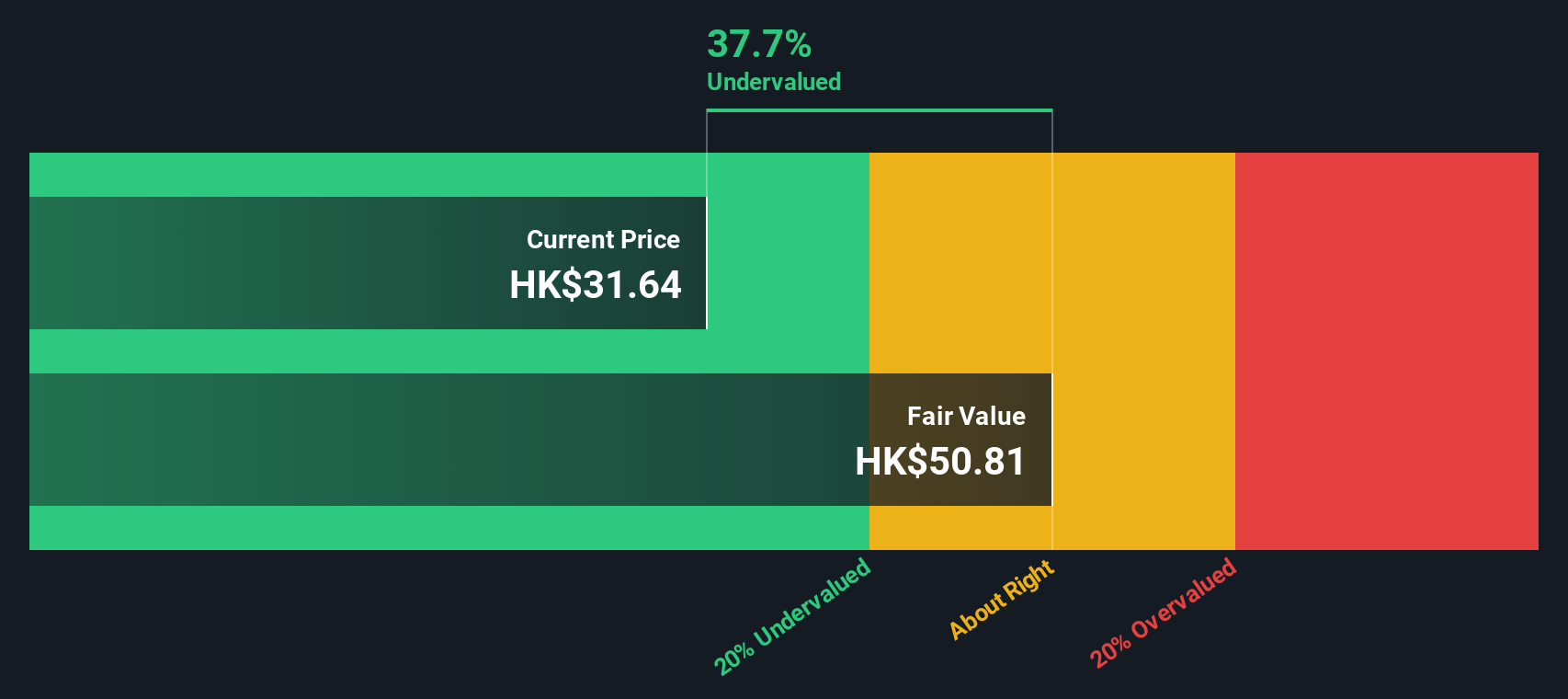

Taking a step back from earnings multiples, our DCF model offers a very different perspective. According to this analysis, Wanguo Gold Group's shares trade 37.6% below their estimated fair value. This suggests the stock could be undervalued by the market at current levels. However, can this significant disconnect really persist?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Wanguo Gold Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 921 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Wanguo Gold Group Narrative

If you have a different perspective or would rather draw your own conclusions from the available data, you can easily create your own Wanguo Gold Group narrative in just a few minutes, starting with Do it your way.

A great starting point for your Wanguo Gold Group research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Unlock the full potential of your portfolio by tapping into the most dynamic opportunities in the market. Let Simply Wall Street's powerful screeners put you ahead of the curve so you do not miss out on tomorrow's leaders.

- Boost your search for breakthrough gains by targeting these 921 undervalued stocks based on cash flows set to outperform based on strong cash flow fundamentals.

- Jump on the artificial intelligence wave and uncover tomorrow’s disruptors among these 26 AI penny stocks harnessing cutting-edge technology for real growth.

- Collect robust, consistent payouts by tracking these 14 dividend stocks with yields > 3% that are delivering yields above 3%, adding steady income to your strategy.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Wanguo Gold Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:3939

Wanguo Gold Group

An investment holding company, engages in mining, ore processing, and sale of concentrate products in the People’s Republic of China and Solomon Islands.

Exceptional growth potential with outstanding track record.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6928.0% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8149.5% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AU

AuCA on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d will expect a 11.2% revenue boost driving future growth

Fair Value:€20916.3% undervalued

23 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3404.9% undervalued

134 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

83 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7923.6% undervalued

919 followersusers have followed this narrative

5 commentsusers have commented on this narrative

21 likesusers have liked this narrative