- Hong Kong

- /

- Real Estate

- /

- SEHK:535

Undervalued Small Caps With Insider Buying In Hong Kong October 2024

Reviewed by Simply Wall St

As global markets navigate the complexities of rising U.S. Treasury yields and mixed economic signals, Hong Kong's small-cap sector presents intriguing opportunities amid broader market fluctuations. With the Hang Seng Index experiencing a slight decline, investors may find potential in small-cap stocks that demonstrate strong fundamentals and insider confidence, particularly those that can weather current economic challenges while capitalizing on local market dynamics.

Top 5 Undervalued Small Caps With Insider Buying In Hong Kong

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Vesync | 6.9x | 1.0x | 0.55% | ★★★★★☆ |

| Edianyun | NA | 0.6x | 39.42% | ★★★★★☆ |

| Lion Rock Group | 5.5x | 0.4x | 49.10% | ★★★★☆☆ |

| Gemdale Properties and Investment | NA | 0.2x | 42.84% | ★★★★☆☆ |

| Shanghai Chicmax Cosmetic | 16.8x | 2.1x | -142.90% | ★★★☆☆☆ |

| Cheerwin Group | 11.7x | 1.5x | 44.50% | ★★★☆☆☆ |

| China Lesso Group Holdings | 6.0x | 0.4x | -523.40% | ★★★☆☆☆ |

| Lee & Man Paper Manufacturing | 7.2x | 0.4x | -47.49% | ★★★☆☆☆ |

| Emperor International Holdings | NA | 0.8x | 30.76% | ★★★☆☆☆ |

We're going to check out a few of the best picks from our screener tool.

China Lesso Group Holdings (SEHK:2128)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: China Lesso Group Holdings is a leading industrial group that manufactures and sells building materials and interior decoration products, with a focus on the plastics and rubber segment, which generated CN¥29.13 billion in revenue.

Operations: The company generates revenue primarily from its Plastics & Rubber segment, with recent figures showing CN¥29.13 billion in revenue. The cost of goods sold (COGS) for this period was CN¥21.55 billion, leading to a gross profit margin of 26.04%. Operating expenses amounted to CN¥3.44 billion, while non-operating expenses were reported at CN¥2.23 billion, impacting the net income margin which stood at 6.58%.

PE: 6.0x

China Lesso Group Holdings, a smaller player in Hong Kong's market, is drawing attention for its potential value. Despite facing a decline in sales and net income for the first half of 2024, with sales dropping to CNY 13.56 billion from CNY 15.30 billion and net income falling to CNY 1.04 billion from CNY 1.49 billion year-over-year, insider confidence is evident as an individual purchased four million shares valued at approximately CNY 10 million this year, reflecting belief in future growth prospects despite high debt levels and reliance on external borrowing for funding.

- Unlock comprehensive insights into our analysis of China Lesso Group Holdings stock in this valuation report.

Learn about China Lesso Group Holdings' historical performance.

Lee & Man Paper Manufacturing (SEHK:2314)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Lee & Man Paper Manufacturing is engaged in the production of packaging paper, tissue paper, and pulp, with a market capitalization of HK$11.02 billion.

Operations: The company generates revenue primarily from packaging paper and tissue paper, with packaging paper contributing the largest share. Over recent periods, the gross profit margin has shown a downward trend, declining to 10.03% as of December 2023. Operating expenses have remained significant relative to gross profit, impacting overall profitability.

PE: 7.2x

Lee & Man Paper Manufacturing has shown insider confidence with Ho Chung Lee purchasing 483,000 shares for HK$1.1 million, increasing their holdings by over 122% recently. The company repurchased 13.5 million shares from January to May 2024 for HK$28.1 million, signaling management's belief in its potential. Despite relying on external borrowing, the company's net income surged to HK$805.69 million for the first half of 2024 from HK$359.9 million a year ago, reflecting strong operational improvements and positioning it attractively within Hong Kong's small-cap landscape.

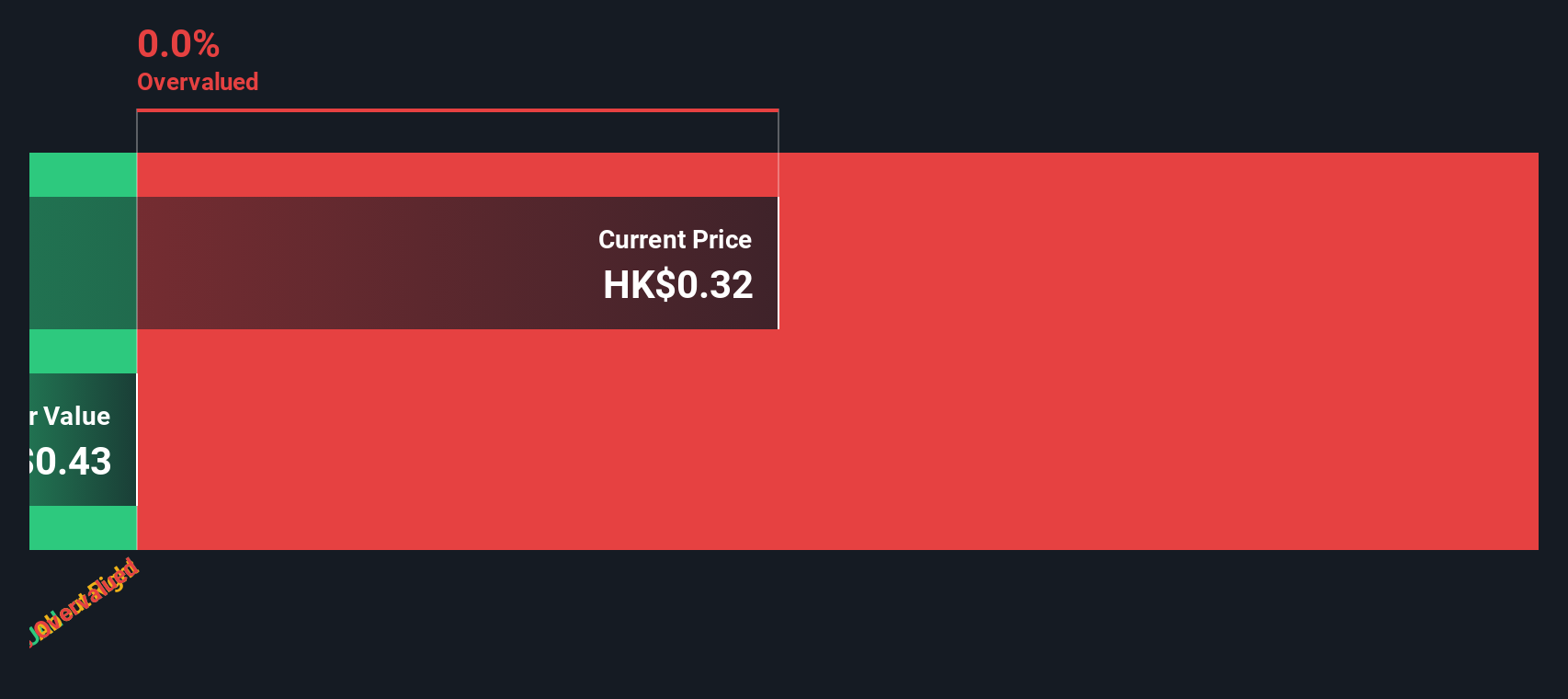

Gemdale Properties and Investment (SEHK:535)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Gemdale Properties and Investment is engaged in property development and property investment and management, with a focus on real estate projects, and has a market capitalization of CN¥5.69 billion.

Operations: The company generates revenue primarily from Property Development and Property Investment and Management, with the former contributing significantly more. Over recent periods, the gross profit margin has shown fluctuations, reaching 0.1057% by December 2023 after being negative earlier in March 2023 at -0.0004%. Operating expenses have been rising alongside non-operating expenses, impacting net income margins which turned negative in early 2024.

PE: -1.9x

Gemdale Properties and Investment, a smaller player in Hong Kong's market, has seen significant insider confidence with Non-Executive Director Lian Huat Loh purchasing 10 million shares recently. Despite earnings declining by 29.5% annually over the past five years and a volatile share price in recent months, the company's contracted sales from January to September 2024 reached RMB 14.18 billion. However, they reported a net loss of CNY 2.18 billion for the first half of 2024 compared to net income last year, highlighting financial challenges alongside growth opportunities in sales performance.

Make It Happen

- Investigate our full lineup of 9 Undervalued SEHK Small Caps With Insider Buying right here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:535

Gemdale Properties and Investment

An investment holding company, engages in the property investment, development, and management activities in Mainland China.

Good value with mediocre balance sheet.