Advertisement

- Hong Kong

- /

- Basic Materials

- /

- SEHK:1847

Is YCIH Green High-Performance Concrete (HKG:1847) Using Too Much Debt?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, YCIH Green High-Performance Concrete Company Limited (HKG:1847) does carry debt. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is YCIH Green High-Performance Concrete's Debt?

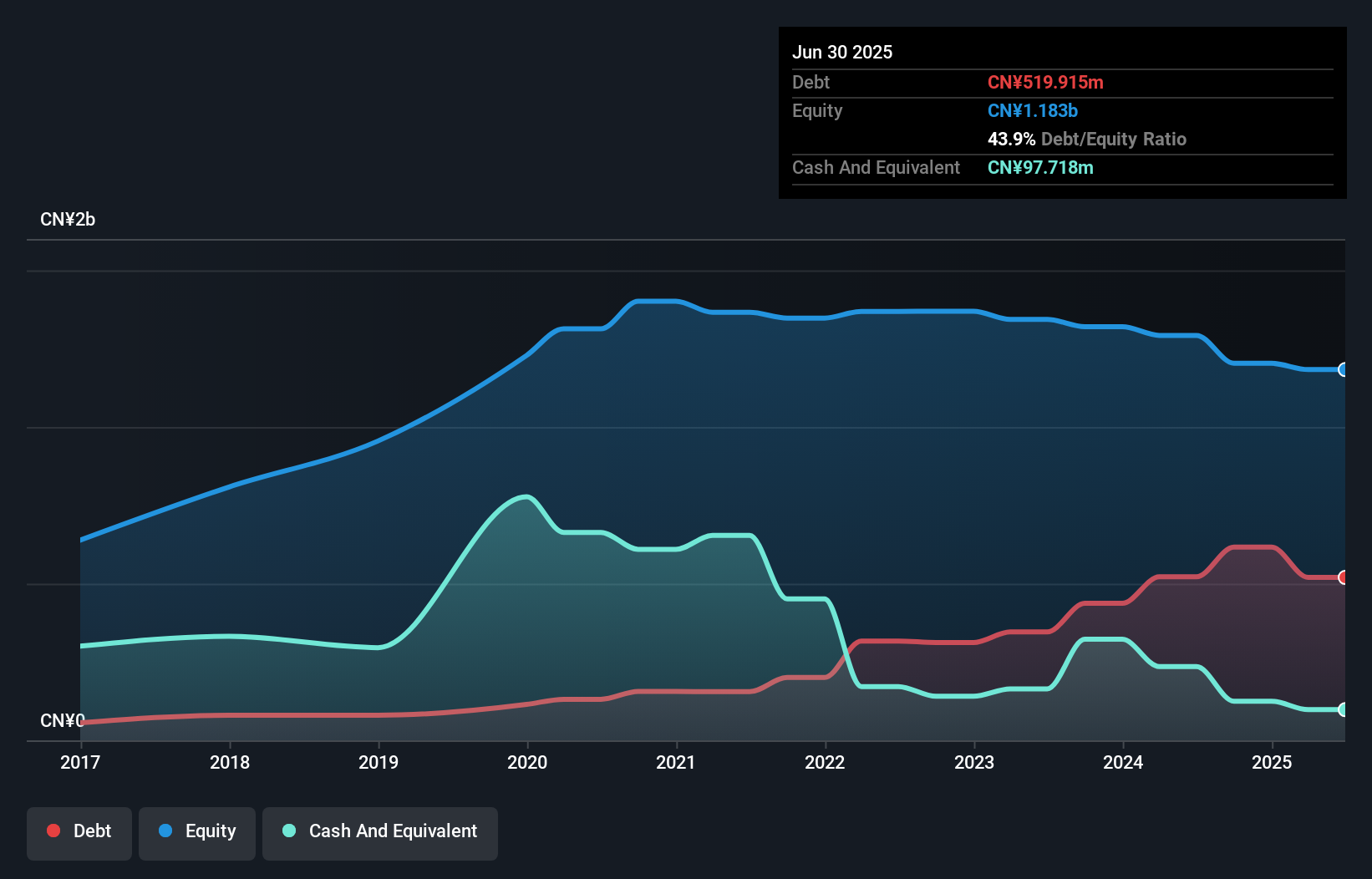

As you can see below, YCIH Green High-Performance Concrete had CN¥519.9m of debt, at June 2025, which is about the same as the year before. You can click the chart for greater detail. However, because it has a cash reserve of CN¥97.7m, its net debt is less, at about CN¥422.2m.

A Look At YCIH Green High-Performance Concrete's Liabilities

The latest balance sheet data shows that YCIH Green High-Performance Concrete had liabilities of CN¥2.55b due within a year, and liabilities of CN¥2.28m falling due after that. Offsetting this, it had CN¥97.7m in cash and CN¥3.19b in receivables that were due within 12 months. So it can boast CN¥743.1m more liquid assets than total liabilities.

This surplus liquidity suggests that YCIH Green High-Performance Concrete's balance sheet could take a hit just as well as Homer Simpson's head can take a punch. On this view, lenders should feel as safe as the beloved of a black-belt karate master. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since YCIH Green High-Performance Concrete will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

See our latest analysis for YCIH Green High-Performance Concrete

Over 12 months, YCIH Green High-Performance Concrete made a loss at the EBIT level, and saw its revenue drop to CN¥912m, which is a fall of 12%. That's not what we would hope to see.

Caveat Emptor

While YCIH Green High-Performance Concrete's falling revenue is about as heartwarming as a wet blanket, arguably its earnings before interest and tax (EBIT) loss is even less appealing. Its EBIT loss was a whopping CN¥126m. That said, we're impressed with the strong balance sheet liquidity. That will give the company some time and space to grow and develop its business as need be. While the stock is probably a bit risky, there may be an opportunity if the business itself improves, allowing the company to stage a recovery. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. These risks can be hard to spot. Every company has them, and we've spotted 2 warning signs for YCIH Green High-Performance Concrete (of which 1 is a bit concerning!) you should know about.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1847

YCIH Green High-Performance Concrete

Operates as a ready-mixed concrete producer in the People's Republic of China.

Mediocre balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.3% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor