China Taiping Insurance Holdings Company Limited's (HKG:966) Subdued P/E Might Signal An Opportunity

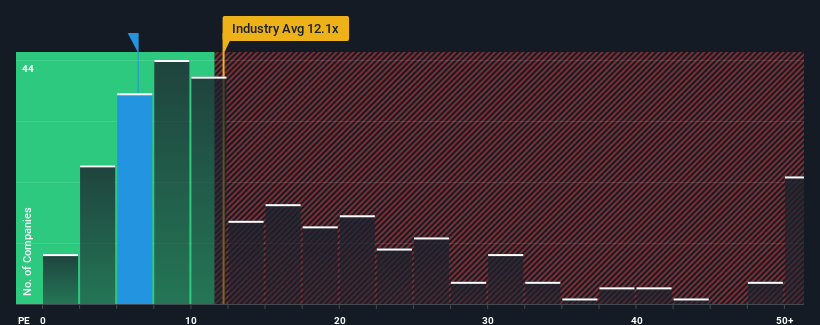

When close to half the companies in Hong Kong have price-to-earnings ratios (or "P/E's") above 10x, you may consider China Taiping Insurance Holdings Company Limited (HKG:966) as an attractive investment with its 6.4x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

China Taiping Insurance Holdings has been struggling lately as its earnings have declined faster than most other companies. The P/E is probably low because investors think this poor earnings performance isn't going to improve at all. If you still like the company, you'd want its earnings trajectory to turn around before making any decisions. Or at the very least, you'd be hoping the earnings slide doesn't get any worse if your plan is to pick up some stock while it's out of favour.

See our latest analysis for China Taiping Insurance Holdings

Does Growth Match The Low P/E?

In order to justify its P/E ratio, China Taiping Insurance Holdings would need to produce sluggish growth that's trailing the market.

Retrospectively, the last year delivered a frustrating 50% decrease to the company's bottom line. As a result, earnings from three years ago have also fallen 34% overall. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Turning to the outlook, the next three years should generate growth of 32% per year as estimated by the ten analysts watching the company. Meanwhile, the rest of the market is forecast to only expand by 16% per year, which is noticeably less attractive.

With this information, we find it odd that China Taiping Insurance Holdings is trading at a P/E lower than the market. It looks like most investors are not convinced at all that the company can achieve future growth expectations.

What We Can Learn From China Taiping Insurance Holdings' P/E?

We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that China Taiping Insurance Holdings currently trades on a much lower than expected P/E since its forecast growth is higher than the wider market. There could be some major unobserved threats to earnings preventing the P/E ratio from matching the positive outlook. It appears many are indeed anticipating earnings instability, because these conditions should normally provide a boost to the share price.

We don't want to rain on the parade too much, but we did also find 2 warning signs for China Taiping Insurance Holdings that you need to be mindful of.

If you're unsure about the strength of China Taiping Insurance Holdings' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:966

China Taiping Insurance Holdings

An investment holding company, underwrites various insurance and reinsurance products in the People’s Republic of China, Hong Kong, Macau, Singapore, and internationally.

Undervalued with proven track record.