- Hong Kong

- /

- Healthcare Services

- /

- SEHK:1099

We Think Sinopharm Group (HKG:1099) Is Taking Some Risk With Its Debt

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Sinopharm Group Co., Ltd. (HKG:1099) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Sinopharm Group

How Much Debt Does Sinopharm Group Carry?

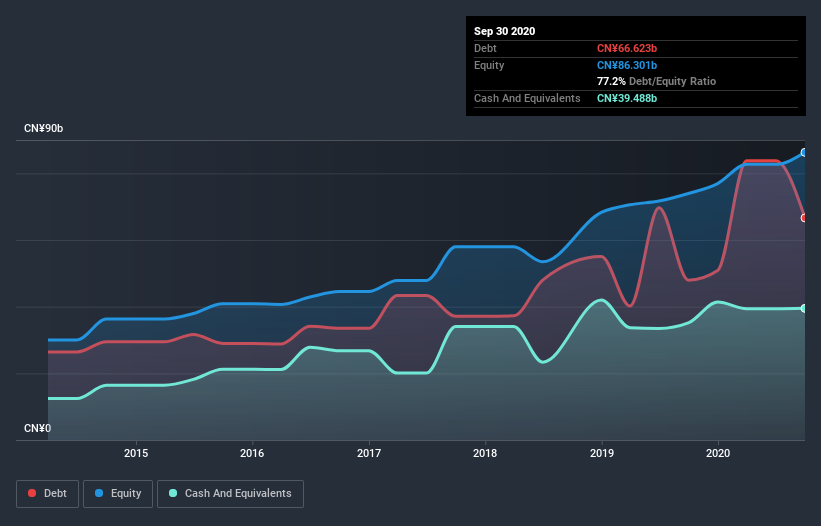

You can click the graphic below for the historical numbers, but it shows that as of September 2020 Sinopharm Group had CN¥65.5b of debt, an increase on CN¥48.0b, over one year. However, it also had CN¥39.5b in cash, and so its net debt is CN¥26.0b.

A Look At Sinopharm Group's Liabilities

Zooming in on the latest balance sheet data, we can see that Sinopharm Group had liabilities of CN¥219.7b due within 12 months and liabilities of CN¥18.2b due beyond that. On the other hand, it had cash of CN¥39.5b and CN¥182.9b worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by CN¥15.5b.

Sinopharm Group has a market capitalization of CN¥45.6b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

With net debt sitting at just 1.3 times EBITDA, Sinopharm Group is arguably pretty conservatively geared. And this view is supported by the solid interest coverage, with EBIT coming in at 7.3 times the interest expense over the last year. The good news is that Sinopharm Group has increased its EBIT by 6.5% over twelve months, which should ease any concerns about debt repayment. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Sinopharm Group can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it's worth checking how much of that EBIT is backed by free cash flow. Over the last three years, Sinopharm Group recorded negative free cash flow, in total. Debt is usually more expensive, and almost always more risky in the hands of a company with negative free cash flow. Shareholders ought to hope for an improvement.

Our View

Sinopharm Group's struggle to convert EBIT to free cash flow had us second guessing its balance sheet strength, but the other data-points we considered were relatively redeeming. For example, its net debt to EBITDA is relatively strong. We should also note that Healthcare industry companies like Sinopharm Group commonly do use debt without problems. Looking at all the angles mentioned above, it does seem to us that Sinopharm Group is a somewhat risky investment as a result of its debt. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For instance, we've identified 1 warning sign for Sinopharm Group that you should be aware of.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

When trading Sinopharm Group or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:1099

Sinopharm Group

Engages in the wholesale and retail of pharmaceutical and medical devices and healthcare products in the People’s Republic of China.

Undervalued with excellent balance sheet and pays a dividend.