Advertisement

Here's Why Shareholders May Want To Be Cautious With Increasing Shenguan Holdings (Group) Limited's (HKG:829) CEO Pay Packet

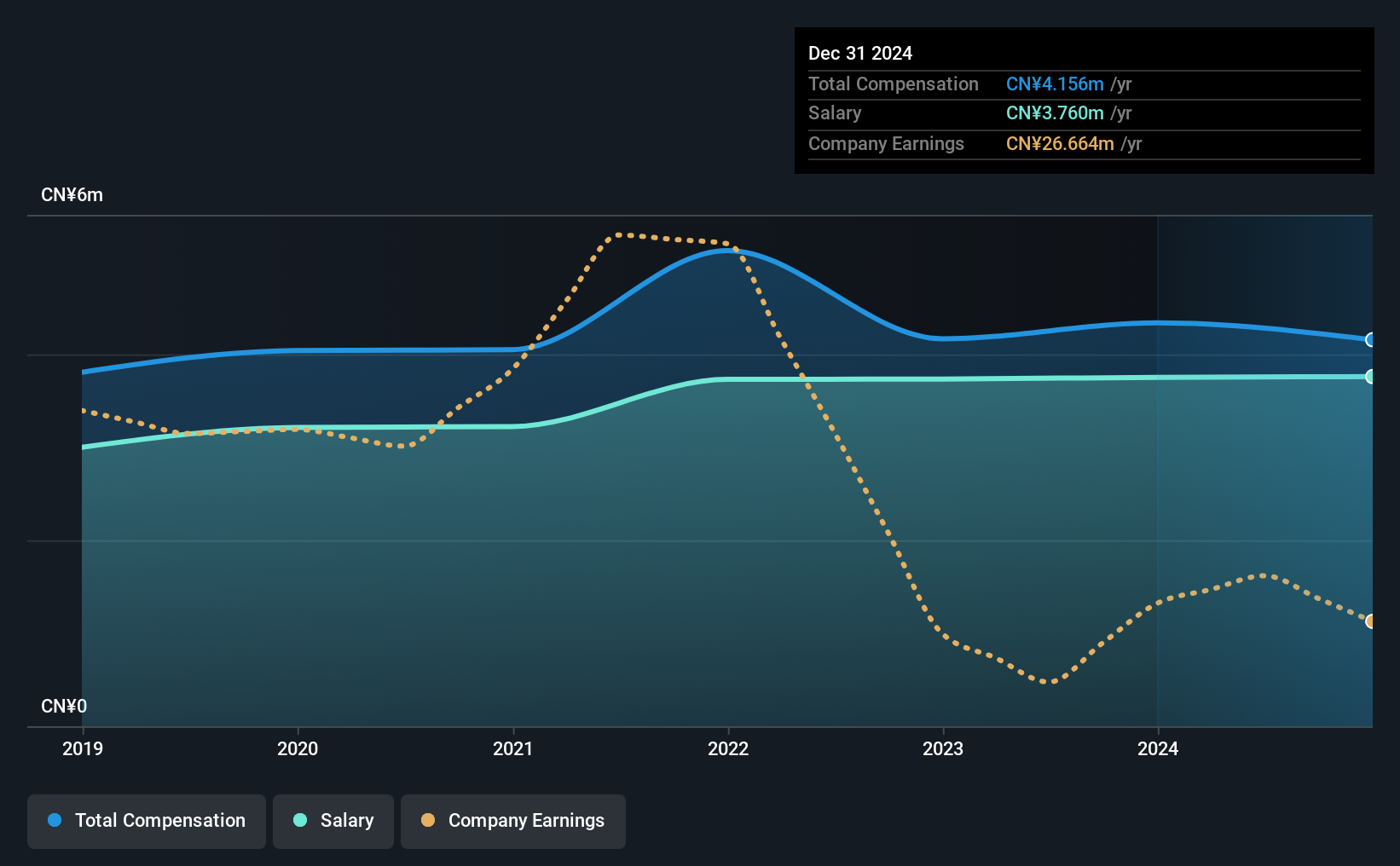

Key Insights

- Shenguan Holdings (Group)'s Annual General Meeting to take place on 6th of June

- CEO Yaxian Zhou's total compensation includes salary of CN¥3.76m

- The total compensation is 248% higher than the average for the industry

- Over the past three years, Shenguan Holdings (Group)'s EPS fell by 40% and over the past three years, the total shareholder return was 2.0%

Share price growth at Shenguan Holdings (Group) Limited (HKG:829) has remained rather flat over the last few years and it may be because earnings has struggled to grow at all. These concerns will be at the front of shareholders' minds as they go into the AGM coming up on 6th of June. One way that shareholders can influence managerial decisions is through voting on CEO and executive remuneration packages, which studies show could impact company performance. In our analysis below, we show why shareholders may consider holding off a raise for the CEO's compensation until company performance improves.

See our latest analysis for Shenguan Holdings (Group)

How Does Total Compensation For Yaxian Zhou Compare With Other Companies In The Industry?

Our data indicates that Shenguan Holdings (Group) Limited has a market capitalization of HK$1.0b, and total annual CEO compensation was reported as CN¥4.2m for the year to December 2024. We note that's a small decrease of 4.2% on last year. In particular, the salary of CN¥3.76m, makes up a huge portion of the total compensation being paid to the CEO.

For comparison, other companies in the Hong Kong Food industry with market capitalizations below HK$1.6b, reported a median total CEO compensation of CN¥1.2m. This suggests that Yaxian Zhou is paid more than the median for the industry. Moreover, Yaxian Zhou also holds HK$102m worth of Shenguan Holdings (Group) stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | CN¥3.8m | CN¥3.8m | 90% |

| Other | CN¥396k | CN¥585k | 10% |

| Total Compensation | CN¥4.2m | CN¥4.3m | 100% |

On an industry level, roughly 81% of total compensation represents salary and 19% is other remuneration. Shenguan Holdings (Group) pays out 90% of remuneration in the form of a salary, significantly higher than the industry average. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

Shenguan Holdings (Group) Limited's Growth

Over the last three years, Shenguan Holdings (Group) Limited has shrunk its earnings per share by 40% per year. In the last year, its revenue is down 8.4%.

The decline in EPS is a bit concerning. This is compounded by the fact revenue is actually down on last year. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has Shenguan Holdings (Group) Limited Been A Good Investment?

Shenguan Holdings (Group) Limited has not done too badly by shareholders, with a total return of 2.0%, over three years. It would be nice to see that metric improve in the future. In light of that, investors might probably want to see an improvement on their returns before they feel generous about increasing the CEO remuneration.

To Conclude...

The flat share price growth combined with the the fact that earnings have failed to grow makes us wonder whether the share price will have any further strong momentum. Shareholders should make the most of the coming opportunity to question the board on key concerns they may have and revisit their investment thesis with regards to the company.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. We've identified 2 warning signs for Shenguan Holdings (Group) that investors should be aware of in a dynamic business environment.

Switching gears from Shenguan Holdings (Group), if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:829

Shenguan Holdings (Group)

An investment holding company, engages in the manufacture and sale of edible collagen sausage casing products in Mainland China, Asia, and internationally.

Mediocre balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.8% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor