Advertisement

- Hong Kong

- /

- Consumer Finance

- /

- SEHK:1577

Quanzhou Huixin Micro-credit Co., Ltd. (HKG:1577) Surges 36% Yet Its Low P/E Is No Reason For Excitement

Quanzhou Huixin Micro-credit Co., Ltd. (HKG:1577) shareholders would be excited to see that the share price has had a great month, posting a 36% gain and recovering from prior weakness. But the gains over the last month weren't enough to make shareholders whole, as the share price is still down 4.0% in the last twelve months.

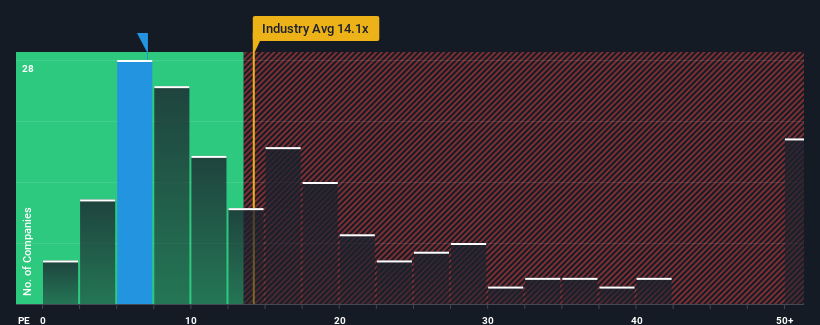

Although its price has surged higher, Quanzhou Huixin Micro-credit may still be sending bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 7x, since almost half of all companies in Hong Kong have P/E ratios greater than 10x and even P/E's higher than 20x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

The recent earnings growth at Quanzhou Huixin Micro-credit would have to be considered satisfactory if not spectacular. One possibility is that the P/E is low because investors think this good earnings growth might actually underperform the broader market in the near future. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

View our latest analysis for Quanzhou Huixin Micro-credit

Does Growth Match The Low P/E?

There's an inherent assumption that a company should underperform the market for P/E ratios like Quanzhou Huixin Micro-credit's to be considered reasonable.

Taking a look back first, we see that the company managed to grow earnings per share by a handy 6.8% last year. This was backed up an excellent period prior to see EPS up by 58% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Comparing that to the market, which is predicted to deliver 20% growth in the next 12 months, the company's momentum is weaker based on recent medium-term annualised earnings results.

In light of this, it's understandable that Quanzhou Huixin Micro-credit's P/E sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on to something they believe will continue to trail the bourse.

The Key Takeaway

Quanzhou Huixin Micro-credit's stock might have been given a solid boost, but its P/E certainly hasn't reached any great heights. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Quanzhou Huixin Micro-credit maintains its low P/E on the weakness of its recent three-year growth being lower than the wider market forecast, as expected. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. Unless the recent medium-term conditions improve, they will continue to form a barrier for the share price around these levels.

It is also worth noting that we have found 4 warning signs for Quanzhou Huixin Micro-credit (1 is a bit unpleasant!) that you need to take into consideration.

If you're unsure about the strength of Quanzhou Huixin Micro-credit's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Quanzhou Huixin Micro-credit might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1577

Quanzhou Huixin Micro-credit

A microfinance company, provides various short-term financing solutions to entrepreneurial individuals, small and medium-sized enterprises, and microenterprises in the People’s Republic of China.

Proven track record with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.3% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.0% undervalued

TI

Community Contributor