Advertisement

- Hong Kong

- /

- Capital Markets

- /

- SEHK:1469

Get Nice Financial Group (HKG:1469) Will Pay A Larger Dividend Than Last Year At HK$0.03

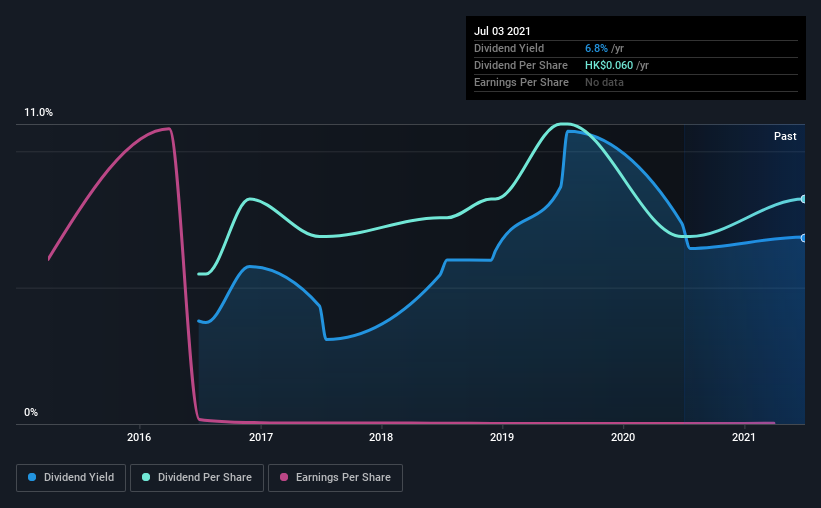

Get Nice Financial Group Limited (HKG:1469) has announced that it will be increasing its dividend on the 10th of September to HK$0.03. This will take the annual payment from 6.8% to 6.8% of the stock price, which is above what most companies in the industry pay.

See our latest analysis for Get Nice Financial Group

Get Nice Financial Group Is Paying Out More Than It Is Earning

Impressive dividend yields are good, but this doesn't matter much if the payments can't be sustained. Before this announcement, Get Nice Financial Group was paying out 70% of earnings, but a comparatively small of free cash flows. Since the dividend is just paying out cash to shareholders, we care more about the cash payout ratio from which we can see plenty is being left over for reinvestment in the business.

Looking forward, EPS could fall by 69.9% if the company can't turn things around from the last few years. Assuming the dividend continues along recent trends, we believe the payout ratio could reach 236%, which could put the dividend under pressure if earnings don't start to improve.

Get Nice Financial Group's Dividend Has Lacked Consistency

Even in its relatively short history, the company has reduced the dividend at least once. This makes us cautious about the consistency of the dividend over a full economic cycle. Since 2016, the first annual payment was HK$0.04, compared to the most recent full-year payment of HK$0.06. This works out to be a compound annual growth rate (CAGR) of approximately 8.4% a year over that time. A reasonable rate of dividend growth is good to see, but we're wary that the dividend history is not as solid as we'd like, having been cut at least once.

Dividend Growth Potential Is Shaky

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. Get Nice Financial Group's earnings per share has shrunk at 70% a year over the past five years. A sharp decline in earnings per share is not great from from a dividend perspective. Even conservative payout ratios can come under pressure if earnings fall far enough.

Our Thoughts On Get Nice Financial Group's Dividend

Overall, we always like to see the dividend being raised, but we don't think Get Nice Financial Group will make a great income stock. The company is generating plenty of cash, which could maintain the dividend for a while, but the track record hasn't been great. This company is not in the top tier of income providing stocks.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. Just as an example, we've come across 2 warning signs for Get Nice Financial Group you should be aware of, and 1 of them is concerning. If you are a dividend investor, you might also want to look at our curated list of high performing dividend stock.

If you’re looking to trade a wide range of investments, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:1469

Get Nice Financial Group

An investment holding company, provides financial services in Hong Kong.

Flawless balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor