Advertisement

- Hong Kong

- /

- Hospitality

- /

- SEHK:2255

Is Haichang Ocean Park Holdings (HKG:2255) Using Debt In A Risky Way?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Haichang Ocean Park Holdings Ltd. (HKG:2255) does carry debt. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Haichang Ocean Park Holdings

What Is Haichang Ocean Park Holdings's Debt?

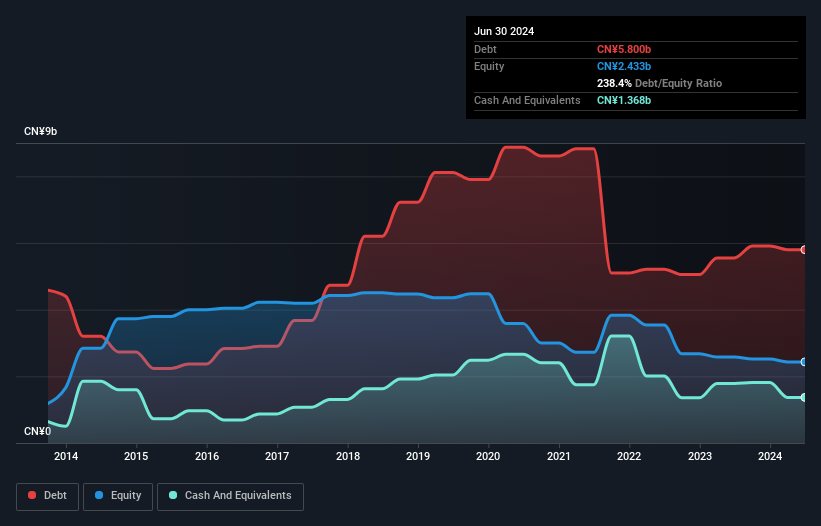

The image below, which you can click on for greater detail, shows that at June 2024 Haichang Ocean Park Holdings had debt of CN¥5.80b, up from CN¥5.55b in one year. On the flip side, it has CN¥1.37b in cash leading to net debt of about CN¥4.43b.

A Look At Haichang Ocean Park Holdings' Liabilities

According to the last reported balance sheet, Haichang Ocean Park Holdings had liabilities of CN¥2.39b due within 12 months, and liabilities of CN¥6.33b due beyond 12 months. On the other hand, it had cash of CN¥1.37b and CN¥99.5m worth of receivables due within a year. So its liabilities total CN¥7.26b more than the combination of its cash and short-term receivables.

Given this deficit is actually higher than the company's market capitalization of CN¥5.55b, we think shareholders really should watch Haichang Ocean Park Holdings's debt levels, like a parent watching their child ride a bike for the first time. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Haichang Ocean Park Holdings can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Over 12 months, Haichang Ocean Park Holdings reported revenue of CN¥1.9b, which is a gain of 45%, although it did not report any earnings before interest and tax. Shareholders probably have their fingers crossed that it can grow its way to profits.

Caveat Emptor

Despite the top line growth, Haichang Ocean Park Holdings still had an earnings before interest and tax (EBIT) loss over the last year. Indeed, it lost CN¥137m at the EBIT level. Considering that alongside the liabilities mentioned above make us nervous about the company. We'd want to see some strong near-term improvements before getting too interested in the stock. Not least because it had negative free cash flow of CN¥805m over the last twelve months. So suffice it to say we consider the stock to be risky. When we look at a riskier company, we like to check how their profits (or losses) are trending over time. Today, we're providing readers this interactive graph showing how Haichang Ocean Park Holdings's profit, revenue, and operating cashflow have changed over the last few years.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're here to simplify it.

Discover if Haichang Ocean Park Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:2255

Haichang Ocean Park Holdings

Engages in developing and constructing theme parks in the People’s Republic of China.

Reasonable growth potential with imperfect balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor