Advertisement

- Hong Kong

- /

- Hospitality

- /

- SEHK:2108

K2 F&B Holdings' (HKG:2108) Returns On Capital Not Reflecting Well On The Business

If you're looking for a multi-bagger, there's a few things to keep an eye out for. Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. Although, when we looked at K2 F&B Holdings (HKG:2108), it didn't seem to tick all of these boxes.

What Is Return On Capital Employed (ROCE)?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. To calculate this metric for K2 F&B Holdings, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

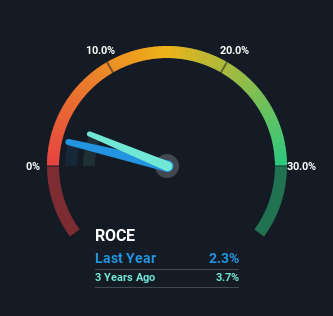

0.023 = S$3.9m ÷ (S$186m - S$13m) (Based on the trailing twelve months to June 2022).

Therefore, K2 F&B Holdings has an ROCE of 2.3%. Ultimately, that's a low return and it under-performs the Hospitality industry average of 2.9%.

View our latest analysis for K2 F&B Holdings

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you want to delve into the historical earnings, revenue and cash flow of K2 F&B Holdings, check out these free graphs here.

How Are Returns Trending?

On the surface, the trend of ROCE at K2 F&B Holdings doesn't inspire confidence. To be more specific, ROCE has fallen from 7.0% over the last five years. On the other hand, the company has been employing more capital without a corresponding improvement in sales in the last year, which could suggest these investments are longer term plays. It's worth keeping an eye on the company's earnings from here on to see if these investments do end up contributing to the bottom line.

The Bottom Line

Bringing it all together, while we're somewhat encouraged by K2 F&B Holdings' reinvestment in its own business, we're aware that returns are shrinking. Since the stock has declined 33% over the last three years, investors may not be too optimistic on this trend improving either. On the whole, we aren't too inspired by the underlying trends and we think there may be better chances of finding a multi-bagger elsewhere.

One final note, you should learn about the 4 warning signs we've spotted with K2 F&B Holdings (including 2 which are potentially serious) .

While K2 F&B Holdings isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

Valuation is complex, but we're here to simplify it.

Discover if K2 F&B Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:2108

K2 F&B Holdings

An investment holding company, owns and operates food centers and food street in Singapore.

Moderate risk and good value.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor