- Hong Kong

- /

- Healthcare Services

- /

- SEHK:9860

SEHK Growth Leaders With High Insider Ownership And Earnings Growth Up To 89%

Reviewed by Simply Wall St

As global markets navigate through varying economic signals, the Hong Kong stock market has shown resilience, with the Hang Seng Index recently posting gains amidst mixed broader Asian market performances. In this context, companies with high insider ownership can be particularly compelling, as they often indicate a strong alignment between company management and shareholder interests, potentially leading to enhanced corporate governance and performance in challenging times.

Top 10 Growth Companies With High Insider Ownership In Hong Kong

| Name | Insider Ownership | Earnings Growth |

| iDreamSky Technology Holdings (SEHK:1119) | 20.1% | 104.1% |

| Fenbi (SEHK:2469) | 32.5% | 43% |

| Zylox-Tonbridge Medical Technology (SEHK:2190) | 18.7% | 79.3% |

| Adicon Holdings (SEHK:9860) | 22.3% | 28.3% |

| Tian Tu Capital (SEHK:1973) | 33.9% | 70.5% |

| DPC Dash (SEHK:1405) | 38.2% | 89.7% |

| Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) | 13.9% | 100.1% |

| Zhejiang Leapmotor Technology (SEHK:9863) | 15% | 76.5% |

| Beijing Airdoc Technology (SEHK:2251) | 28.2% | 83.9% |

| Ocumension Therapeutics (SEHK:1477) | 23.1% | 93.7% |

Underneath we present a selection of stocks filtered out by our screen.

DPC Dash (SEHK:1405)

Simply Wall St Growth Rating: ★★★★★☆

Overview: DPC Dash Ltd operates a chain of fast-food restaurants across the People’s Republic of China, with a market capitalization of approximately HK$8.36 billion.

Operations: The company generates CN¥3.05 billion in revenue from its fast-food restaurant operations across China.

Insider Ownership: 38.2%

Earnings Growth Forecast: 89.7% p.a.

DPC Dash, trading at 60.9% below its estimated fair value, shows promise with a high insider ownership trend where insiders substantially bought more shares than sold in the past three months. The company has seen earnings growth of 22.2% annually over the past five years and is forecasted to grow revenue by 24.4% annually, outpacing Hong Kong's market average of 7.8%. Despite recent losses reducing significantly from CNY 222.63 million to CNY 26.6 million year-over-year, DPC Dash is expected to turn profitable within three years, aligning with an aggressive growth trajectory but faces challenges with a forecasted low return on equity of 14%.

- Navigate through the intricacies of DPC Dash with our comprehensive analyst estimates report here.

- Our comprehensive valuation report raises the possibility that DPC Dash is priced higher than what may be justified by its financials.

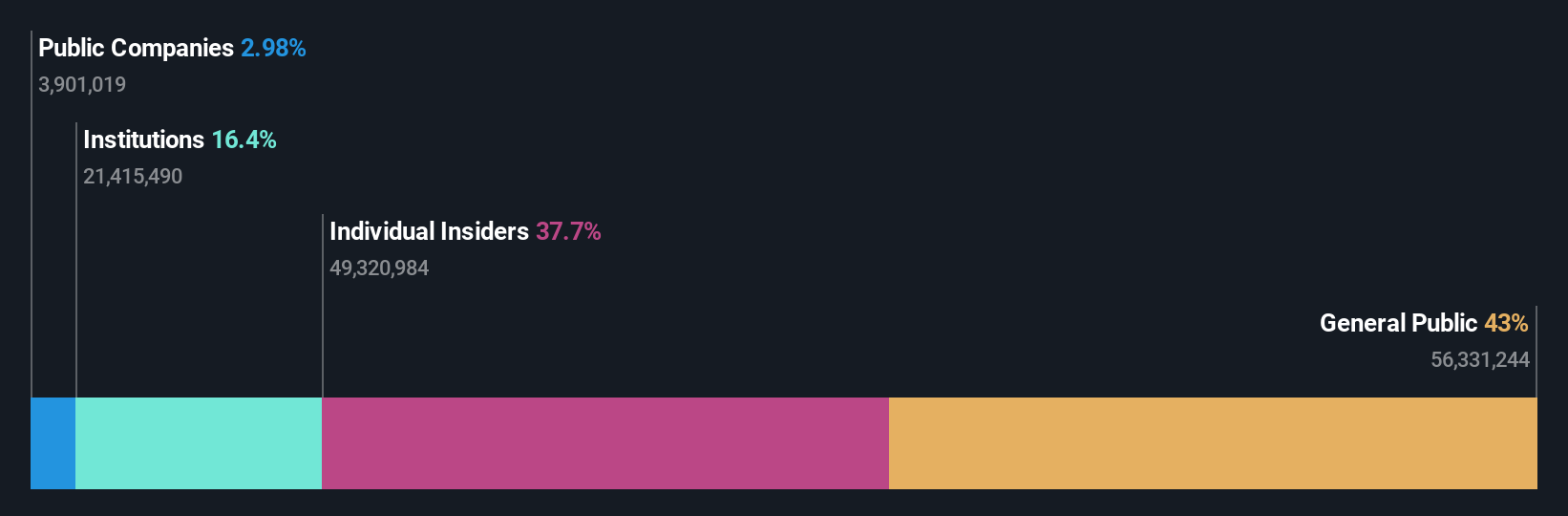

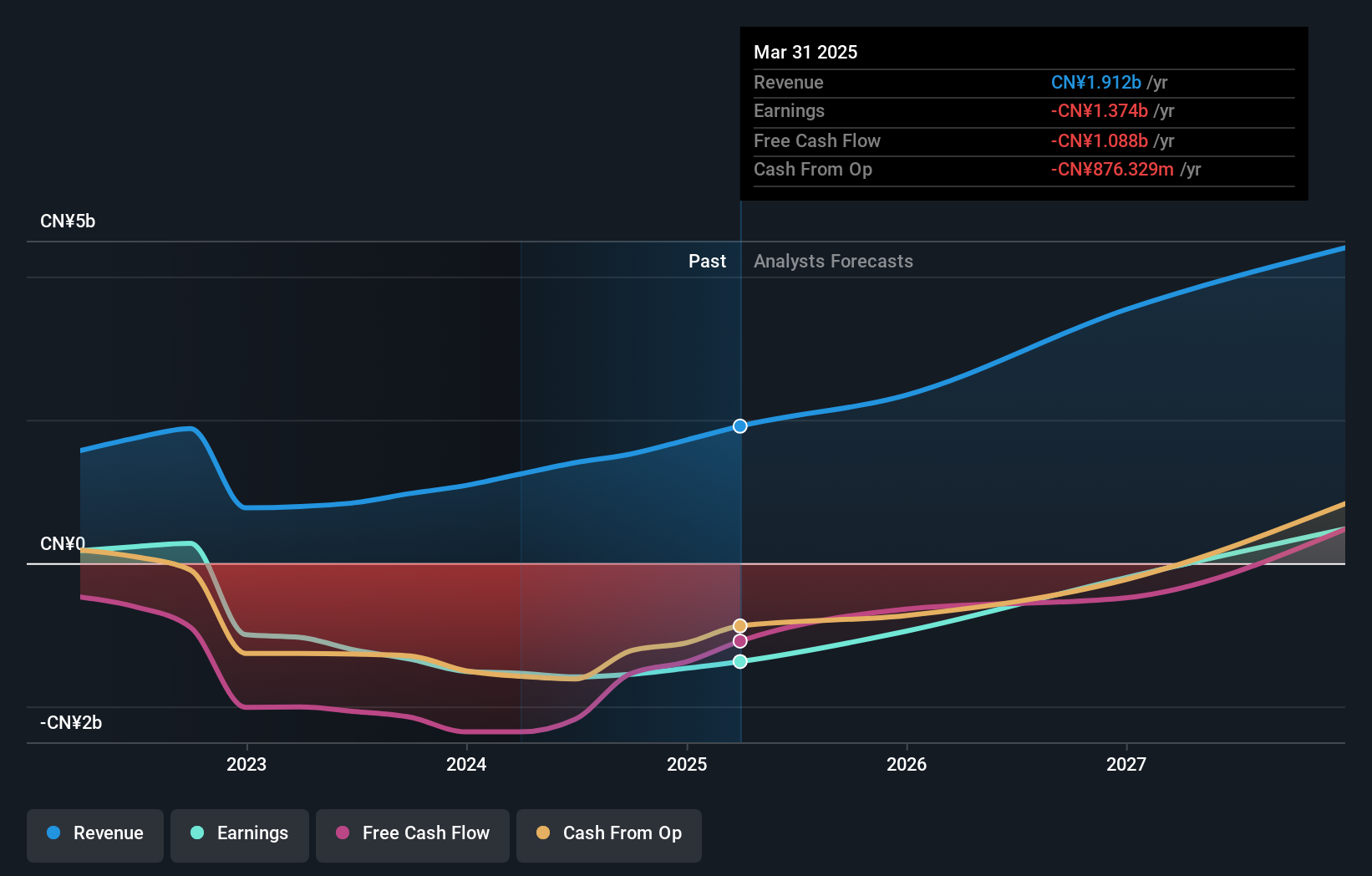

Adicon Holdings (SEHK:9860)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Adicon Holdings Limited, operating medical laboratories in the People’s Republic of China, has a market capitalization of approximately HK$7.11 billion.

Operations: The company generates revenue primarily from its healthcare facilities and services segment, totaling CN¥3.30 billion.

Insider Ownership: 22.3%

Earnings Growth Forecast: 28.3% p.a.

Adicon Holdings, amidst a challenging financial year with revenues and net income significantly down from the previous year, has initiated a substantial share repurchase program, signaling confidence by the management. The appointment of Mr. Zhou Mintao as chairman of the strategy committee could bring fresh perspectives to bolster strategic initiatives. Analysts expect Adicon’s earnings to grow faster than the market average, although revenue growth predictions remain below some high-growth benchmarks in Hong Kong’s competitive landscape.

- Take a closer look at Adicon Holdings' potential here in our earnings growth report.

- Our valuation report here indicates Adicon Holdings may be overvalued.

RemeGen (SEHK:9995)

Simply Wall St Growth Rating: ★★★★★☆

Overview: RemeGen Co., Ltd. is a biopharmaceutical company focused on developing biologics for autoimmune, oncology, and ophthalmic diseases in Mainland China and the United States, with a market capitalization of approximately HK$22.14 billion.

Operations: The company generates revenue primarily through its biopharmaceutical research, service, production, and sales segment, which amounted to CN¥1.25 billion.

Insider Ownership: 16.2%

Earnings Growth Forecast: 54.9% p.a.

RemeGen, a biotech firm in Hong Kong, is trading at 72.1% below its estimated fair value, indicating potential undervaluation. Despite a challenging financial position with less than one year of cash runway and current unprofitability, RemeGen is expected to grow earnings by 54.91% annually over the next three years and become profitable within that timeframe. Recent successful Phase III trials for its breast cancer treatment Disitamab Vedotin signal promising developments, enhancing its growth trajectory amidst high insider ownership concerns due to lack of recent buying or selling information.

- Click to explore a detailed breakdown of our findings in RemeGen's earnings growth report.

- The valuation report we've compiled suggests that RemeGen's current price could be inflated.

Where To Now?

- Embark on your investment journey to our 53 Fast Growing SEHK Companies With High Insider Ownership selection here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:9860

Adicon Holdings

Operates medical laboratories in the People’s Republic of China.

Reasonable growth potential with adequate balance sheet.