Advertisement

- Hong Kong

- /

- Food and Staples Retail

- /

- SEHK:8079

Most Shareholders Will Probably Find That The Compensation For Easy Repay Finance & Investment Limited's (HKG:8079) CEO Is Reasonable

Performance at Easy Repay Finance & Investment Limited (HKG:8079) has been rather uninspiring recently and shareholders may be wondering how CEO Clara Siu plans to fix this. At the next AGM coming up on 27 September 2022, they can influence managerial decision making through voting on resolutions, including executive remuneration. Voting on executive pay could be a powerful way to influence management, as studies have shown that the right compensation incentives impact company performance. In our opinion, CEO compensation does not look excessive and we discuss why.

Check out our latest analysis for Easy Repay Finance & Investment

Comparing Easy Repay Finance & Investment Limited's CEO Compensation With The Industry

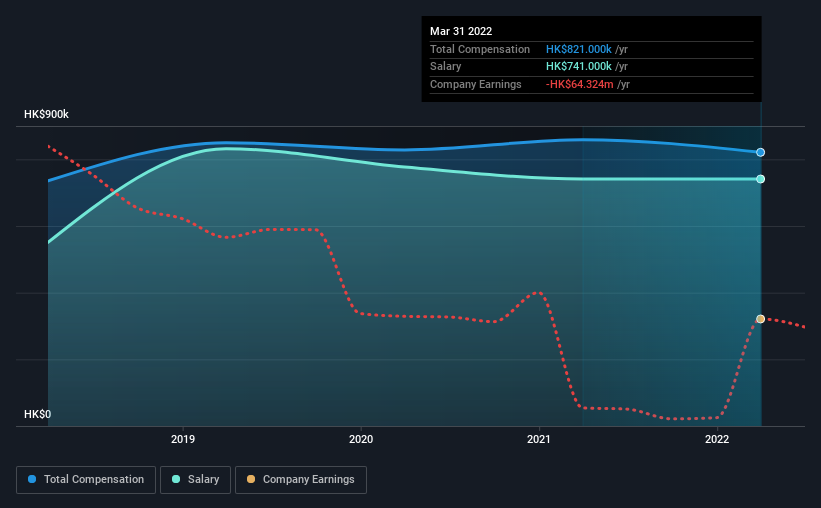

According to our data, Easy Repay Finance & Investment Limited has a market capitalization of HK$45m, and paid its CEO total annual compensation worth HK$821k over the year to March 2022. That's a slight decrease of 4.4% on the prior year. We note that the salary portion, which stands at HK$741.0k constitutes the majority of total compensation received by the CEO.

For comparison, other companies in the industry with market capitalizations below HK$1.6b, reported a median total CEO compensation of HK$2.1m. In other words, Easy Repay Finance & Investment pays its CEO lower than the industry median.

| Component | 2022 | 2021 | Proportion (2022) |

| Salary | HK$741k | HK$741k | 90% |

| Other | HK$80k | HK$118k | 10% |

| Total Compensation | HK$821k | HK$859k | 100% |

On an industry level, roughly 76% of total compensation represents salary and 24% is other remuneration. According to our research, Easy Repay Finance & Investment has allocated a higher percentage of pay to salary in comparison to the wider industry. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

Easy Repay Finance & Investment Limited's Growth

Easy Repay Finance & Investment Limited has reduced its earnings per share by 18% a year over the last three years. It saw its revenue drop 17% over the last year.

The decline in EPS is a bit concerning. This is compounded by the fact revenue is actually down on last year. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has Easy Repay Finance & Investment Limited Been A Good Investment?

Easy Repay Finance & Investment Limited has generated a total shareholder return of 15% over three years, so most shareholders would be reasonably content. But they probably wouldn't be so happy as to think the CEO should be paid more than is normal, for companies around this size.

In Summary...

While it's true that shareholders have seen decent returns, it's hard to overlook the lack of earnings growth and this makes us wonder if the current returns can continue. Shareholders might want to question the board about these concerns, and revisit their investment thesis for the company.

CEO compensation is a crucial aspect to keep your eyes on but investors also need to keep their eyes open for other issues related to business performance. We've identified 3 warning signs for Easy Repay Finance & Investment that investors should be aware of in a dynamic business environment.

Switching gears from Easy Repay Finance & Investment, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

Valuation is complex, but we're here to simplify it.

Discover if Wisdomcome Group Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:8079

Wisdomcome Group Holdings

Engages in the retail and wholesale of grocery products in Hong Kong.

Excellent balance sheet and good value.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|25.1% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.04% overvalued

LI

Community Contributor