Advertisement

Here's Why Shareholders May Want To Be Cautious With Increasing Tristate Holdings Limited's (HKG:458) CEO Pay Packet

Key Insights

- Tristate Holdings will host its Annual General Meeting on 24th of June

- Total pay for CEO Peter Wang includes HK$5.48m salary

- The total compensation is 359% higher than the average for the industry

- Over the past three years, Tristate Holdings' EPS grew by 122% and over the past three years, the total shareholder return was 200%

CEO Peter Wang has done a decent job of delivering relatively good performance at Tristate Holdings Limited (HKG:458) recently. This is something shareholders will keep in mind as they cast their votes on company resolutions such as executive remuneration in the upcoming AGM on 24th of June. However, some shareholders will still be cautious of paying the CEO excessively.

View our latest analysis for Tristate Holdings

Comparing Tristate Holdings Limited's CEO Compensation With The Industry

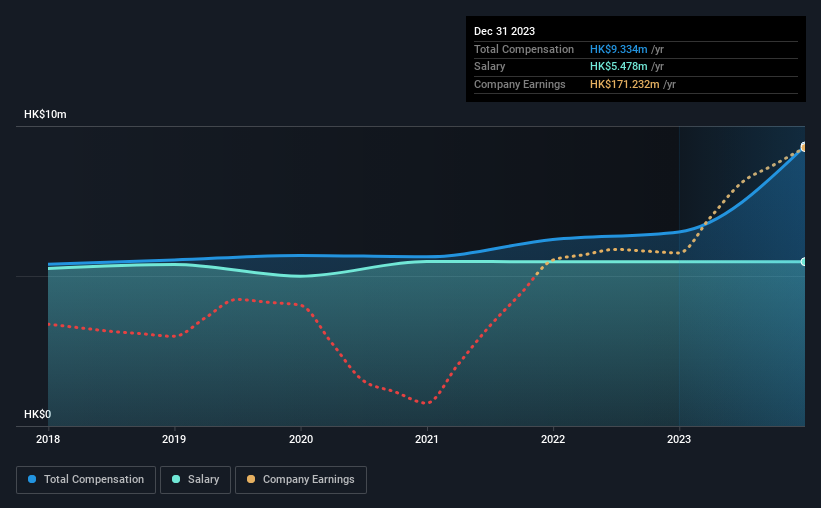

According to our data, Tristate Holdings Limited has a market capitalization of HK$751m, and paid its CEO total annual compensation worth HK$9.3m over the year to December 2023. Notably, that's an increase of 44% over the year before. We note that the salary of HK$5.48m makes up a sizeable portion of the total compensation received by the CEO.

On comparing similar-sized companies in the Hong Kong Luxury industry with market capitalizations below HK$1.6b, we found that the median total CEO compensation was HK$2.0m. Accordingly, our analysis reveals that Tristate Holdings Limited pays Peter Wang north of the industry median. What's more, Peter Wang holds HK$504m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | HK$5.5m | HK$5.5m | 59% |

| Other | HK$3.9m | HK$993k | 41% |

| Total Compensation | HK$9.3m | HK$6.5m | 100% |

Speaking on an industry level, nearly 94% of total compensation represents salary, while the remainder of 6% is other remuneration. In Tristate Holdings' case, non-salary compensation represents a greater slice of total remuneration, in comparison to the broader industry. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

Tristate Holdings Limited's Growth

Tristate Holdings Limited's earnings per share (EPS) grew 122% per year over the last three years. It achieved revenue growth of 13% over the last year.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. This sort of respectable year-on-year revenue growth is often seen at a healthy, growing business. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Tristate Holdings Limited Been A Good Investment?

We think that the total shareholder return of 200%, over three years, would leave most Tristate Holdings Limited shareholders smiling. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

To Conclude...

The company's decent performance might have made most shareholders happy, possibly making CEO remuneration the least of the concerns to be discussed in the upcoming AGM. However, if the board proposes to increase the compensation, some shareholders might have questions given that the CEO is already being paid higher than the industry.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. That's why we did some digging and identified 2 warning signs for Tristate Holdings that you should be aware of before investing.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

Valuation is complex, but we're here to simplify it.

Discover if Tristate Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:458

Tristate Holdings

An investment holding company, engages in the garment manufacturing business in the People’s Republic of China, the United Kingdom, Italy, Singapore, Canada, and internationally.

Flawless balance sheet and good value.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6928.0% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8149.5% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AU

AuCA on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d will expect a 11.2% revenue boost driving future growth

Fair Value:€20916.3% undervalued

23 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3404.9% undervalued

134 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

82 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7923.6% undervalued

919 followersusers have followed this narrative

5 commentsusers have commented on this narrative

21 likesusers have liked this narrative