Advertisement

National Electronics Holdings' (HKG:213) Dividend Will Be Reduced To HK$0.018

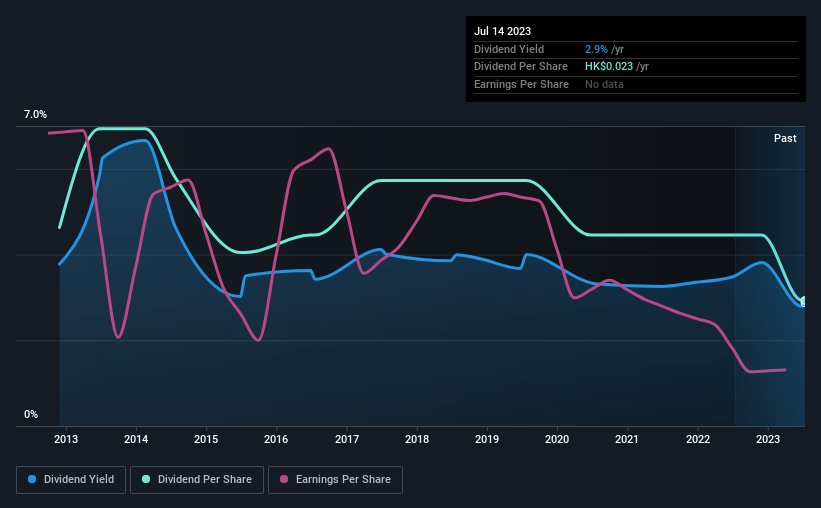

National Electronics Holdings Limited (HKG:213) has announced that on 20th of September, it will be paying a dividend ofHK$0.018, which a reduction from last year's comparable dividend. The dividend yield will be in the average range for the industry at 2.9%.

Check out our latest analysis for National Electronics Holdings

National Electronics Holdings' Payment Has Solid Earnings Coverage

We aren't too impressed by dividend yields unless they can be sustained over time. Based on the last payment, National Electronics Holdings was quite comfortably earning enough to cover the dividend. This means that a large portion of its earnings are being retained to grow the business.

Unless the company can turn things around, EPS could fall by 24.4% over the next year. If the dividend continues along recent trends, we estimate the payout ratio could be 57%, which we consider to be quite comfortable, with most of the company's earnings left over to grow the business in the future.

Dividend Volatility

The company has a long dividend track record, but it doesn't look great with cuts in the past. The dividend has gone from an annual total of HK$0.0364 in 2013 to the most recent total annual payment of HK$0.023. Doing the maths, this is a decline of about 4.5% per year. A company that decreases its dividend over time generally isn't what we are looking for.

Dividend Growth Potential Is Shaky

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. Over the past five years, it looks as though National Electronics Holdings' EPS has declined at around 24% a year. This steep decline can indicate that the business is going through a tough time, which could constrain its ability to pay a larger dividend each year in the future.

Our Thoughts On National Electronics Holdings' Dividend

Overall, the dividend looks like it may have been a bit high, which explains why it has now been cut. In the past, the payments have been unstable, but over the short term the dividend could be reliable, with the company generating enough cash to cover it. We would probably look elsewhere for an income investment.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. Case in point: We've spotted 5 warning signs for National Electronics Holdings (of which 2 are potentially serious!) you should know about. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if National Electronics Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:213

National Electronics Holdings

An investment holding company, manufactures, assembles, and sells electronic watches and watch parts in the People’s Republic of China, Hong Kong, North America, Europe, and internationally.

Slight risk with acceptable track record.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor