Stock Analysis

Three Stocks Estimated To Be Trading With Intrinsic Discounts Between 35.9% And 49.7%

Reviewed by Simply Wall St

As global markets exhibit mixed signals with the S&P 500 reaching record highs amid cooling labor markets and easing inflation pressures, investors are navigating a complex landscape. In such an environment, identifying stocks that are trading below their intrinsic value could present opportunities for discerning investors looking to potentially enhance their portfolios.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Bewith (TSE:9216) | ¥2080.00 | ¥4143.20 | 49.8% |

| Victory Capital Holdings (NasdaqGS:VCTR) | US$50.22 | US$100.02 | 49.8% |

| MaxiPARTS (ASX:MXI) | A$1.98 | A$3.93 | 49.7% |

| Afry (OM:AFRY) | SEK199.20 | SEK396.20 | 49.7% |

| BayCurrent Consulting (TSE:6532) | ¥4323.00 | ¥8596.27 | 49.7% |

| DO & CO (WBAG:DOC) | €166.60 | €331.08 | 49.7% |

| West China Cement (SEHK:2233) | HK$1.08 | HK$2.15 | 49.8% |

| Harvard Bioscience (NasdaqGM:HBIO) | US$3.28 | US$6.55 | 49.9% |

| Wolftank-Adisa Holding (XTRA:WAH) | €11.30 | €22.46 | 49.7% |

| Levima Advanced Materials (SZSE:003022) | CN¥13.88 | CN¥27.68 | 49.9% |

Let's take a closer look at a couple of our picks from the screened companies.

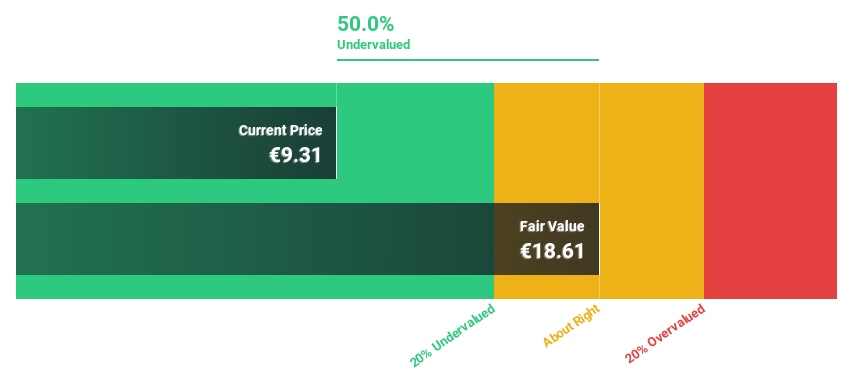

Grifols (BME:GRF)

Overview: Grifols, S.A. is a global plasma therapeutic company based in Spain, with operations spanning the United States, Canada, and other countries, and it has a market capitalization of approximately €6.33 billion.

Operations: The company generates revenue primarily through its Biopharma segment, which brought in €5.66 billion, followed by the Diagnostic and Bio Supplies segments with revenues of €0.65 billion and €0.15 billion respectively.

Estimated Discount To Fair Value: 41.5%

Grifols, trading at €10.03, is significantly undervalued with a fair value estimate of €17.13, reflecting a 41.5% discount. Despite its high earnings growth forecast at 27.2% annually, surpassing the Spanish market's 9.6%, and revenue expected to increase by 6% annually, challenges persist due to its highly volatile share price and earnings impacted by large one-off items. Recent M&A discussions could lead to delisting if Brookfield and family shareholders' potential joint takeover proceeds.

- The growth report we've compiled suggests that Grifols' future prospects could be on the up.

- Click here and access our complete balance sheet health report to understand the dynamics of Grifols.

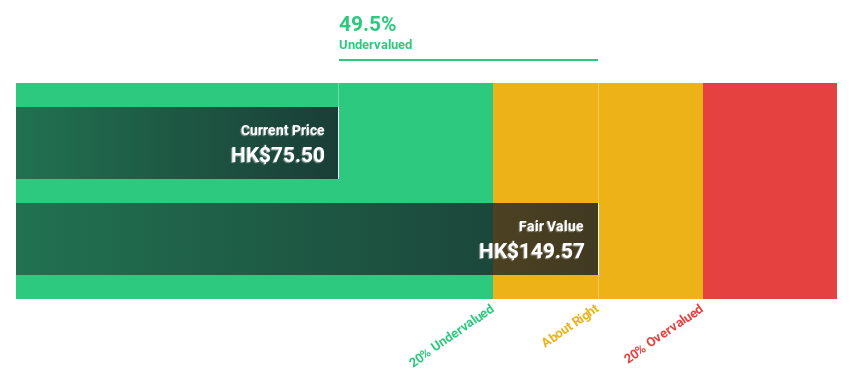

ANTA Sports Products (SEHK:2020)

Overview: ANTA Sports Products Limited operates in the design, manufacturing, and marketing of footwear, apparel, and accessories across Mainland China, Hong Kong, Macao, and internationally, with a market capitalization of approximately HK$203.38 billion.

Operations: The company's revenue is primarily generated from the ANTA brand, which contributed CN¥30.31 billion, followed by the FILA brand at CN¥25.10 billion, and all other brands collectively adding CN¥6.95 billion.

Estimated Discount To Fair Value: 35.9%

ANTA Sports Products, priced at HK$76.15, is valued well below its estimated fair value of HK$118.8, suggesting a significant undervaluation based on cash flow analysis. The company's earnings are expected to grow by 12.7% annually, outpacing the Hong Kong market's growth rate of 11.5%. Recent sales results show positive growth across all brands, with non-newly joined branded products seeing up to 45% growth in Q2 2024 compared to the previous year, indicating robust business performance despite not exceeding a very high annual earnings growth threshold.

- Insights from our recent growth report point to a promising forecast for ANTA Sports Products' business outlook.

- Dive into the specifics of ANTA Sports Products here with our thorough financial health report.

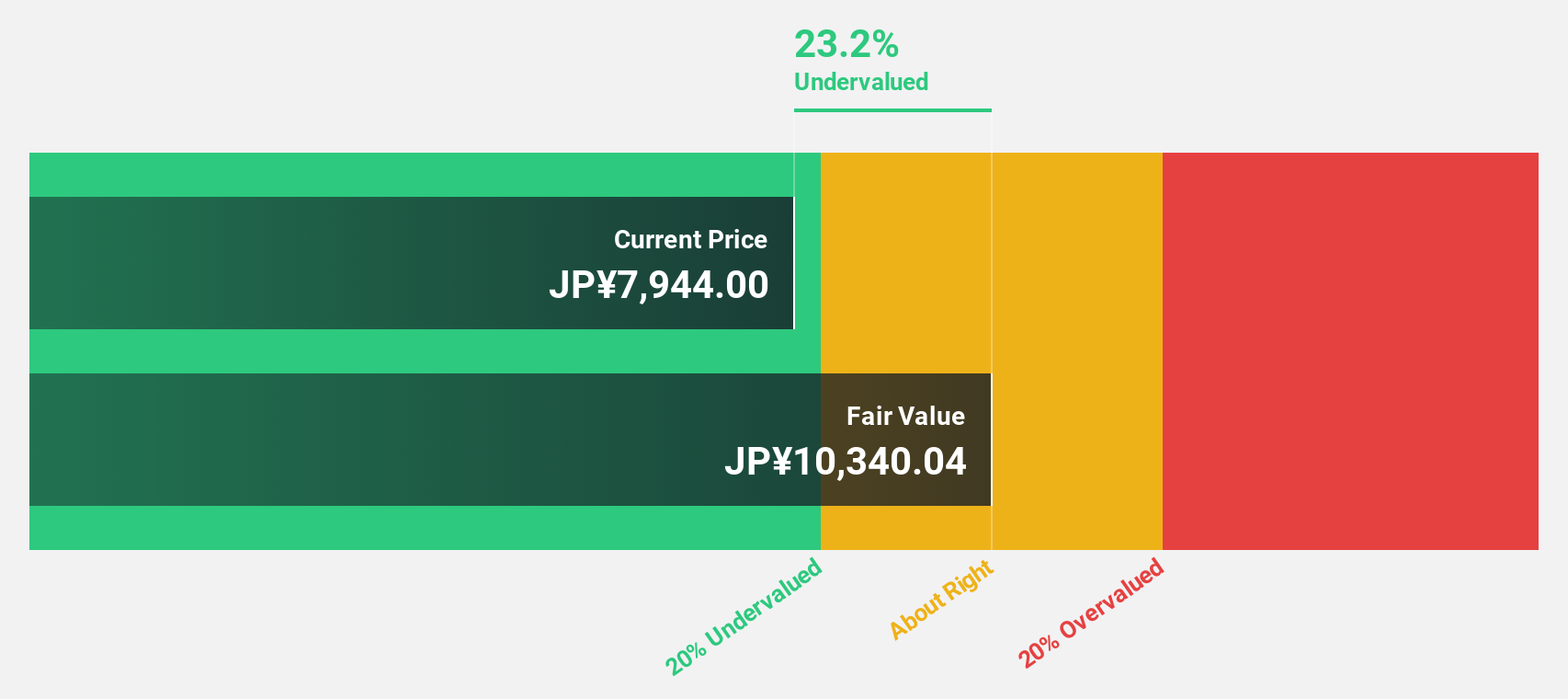

BayCurrent Consulting (TSE:6532)

Overview: BayCurrent Consulting, Inc., a company based in Japan, offers consulting services and has a market capitalization of approximately ¥549.69 billion.

Operations: The firm specializes in consulting services within Japan.

Estimated Discount To Fair Value: 49.7%

BayCurrent Consulting, trading at ¥4323, appears undervalued with a fair value estimate of ¥8596.27 based on DCF analysis, indicating a significant discount. Forecasted earnings growth of 18.4% per year surpasses the Japanese market's 9%, while expected revenue growth is also robust at 17.3% annually. However, its share price has shown high volatility recently. The firm completed a share repurchase program in May 2024 for ¥3,599.77 million to enhance shareholder value, reflecting active management engagement in capital efficiency initiatives.

- Our earnings growth report unveils the potential for significant increases in BayCurrent Consulting's future results.

- Delve into the full analysis health report here for a deeper understanding of BayCurrent Consulting.

Key Takeaways

- Get an in-depth perspective on all 949 Undervalued Stocks Based On Cash Flows by using our screener here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:2020

ANTA Sports Products

Engages in the research and development, design, manufacturing, and marketing of shoes, apparel, and accessories in the Mainland of China, Hong Kong, Macao, and internationally.

Outstanding track record with excellent balance sheet.