- Hong Kong

- /

- Real Estate

- /

- SEHK:1972

SEHK's Hidden Value: Three Stocks That May Be Undervalued In September 2024

Reviewed by Simply Wall St

The Hong Kong stock market has experienced a notable surge, driven by China's recent robust stimulus measures aimed at revitalizing its economy. This positive sentiment has lifted the Hang Seng Index significantly, creating an opportune moment to explore potential undervalued stocks. In such a dynamic environment, identifying stocks that are trading below their intrinsic value can be particularly rewarding for investors looking to capitalize on market inefficiencies.

Top 10 Undervalued Stocks Based On Cash Flows In Hong Kong

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| FIT Hon Teng (SEHK:6088) | HK$2.37 | HK$4.31 | 45% |

| Bairong (SEHK:6608) | HK$8.74 | HK$16.78 | 47.9% |

| Shanghai INT Medical Instruments (SEHK:1501) | HK$28.70 | HK$56.47 | 49.2% |

| Akeso (SEHK:9926) | HK$67.40 | HK$134.25 | 49.8% |

| Digital China Holdings (SEHK:861) | HK$2.95 | HK$5.86 | 49.6% |

| Nayuki Holdings (SEHK:2150) | HK$1.82 | HK$3.38 | 46.1% |

| Hua Hong Semiconductor (SEHK:1347) | HK$19.02 | HK$37.14 | 48.8% |

| DPC Dash (SEHK:1405) | HK$76.45 | HK$136.57 | 44% |

| AK Medical Holdings (SEHK:1789) | HK$4.72 | HK$8.42 | 44% |

| Ming Yuan Cloud Group Holdings (SEHK:909) | HK$2.61 | HK$4.72 | 44.7% |

Let's review some notable picks from our screened stocks.

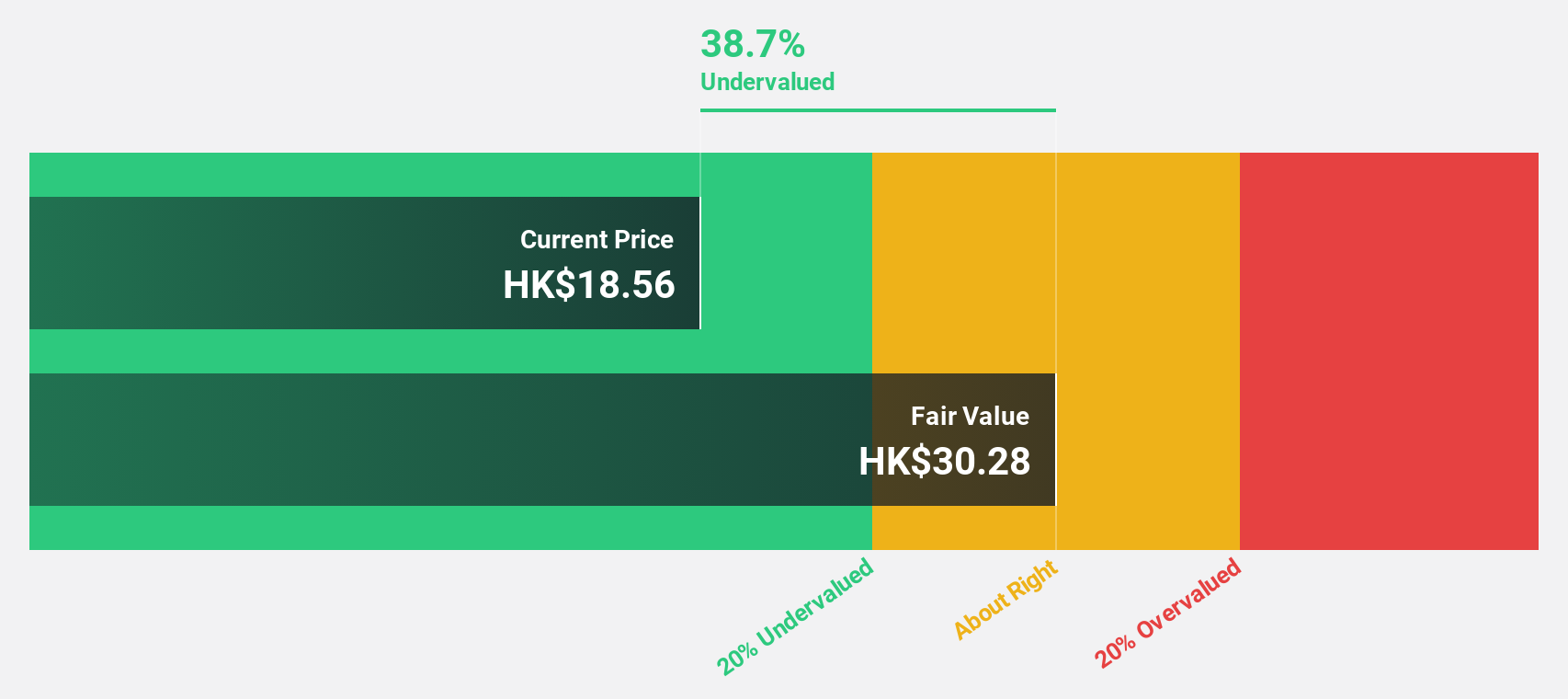

Hua Hong Semiconductor (SEHK:1347)

Overview: Hua Hong Semiconductor Limited is an investment holding company that manufactures and sells semiconductor products, with a market cap of HK$39.53 billion.

Operations: The company's revenue segments include the manufacturing and sale of semiconductor products.

Estimated Discount To Fair Value: 48.8%

Hua Hong Semiconductor is trading at HK$19.02, significantly below its estimated fair value of HK$37.14. Despite a decline in profit margins from 19.6% to 4.5% over the past year and lower net income for Q2 2024 (US$6.67 million), earnings are forecast to grow by 33.16% annually over the next three years, outpacing the Hong Kong market's growth rate of 12%. Revenue is expected to increase by around US$500 million to US$520 million in Q3 2024.

- Insights from our recent growth report point to a promising forecast for Hua Hong Semiconductor's business outlook.

- Navigate through the intricacies of Hua Hong Semiconductor with our comprehensive financial health report here.

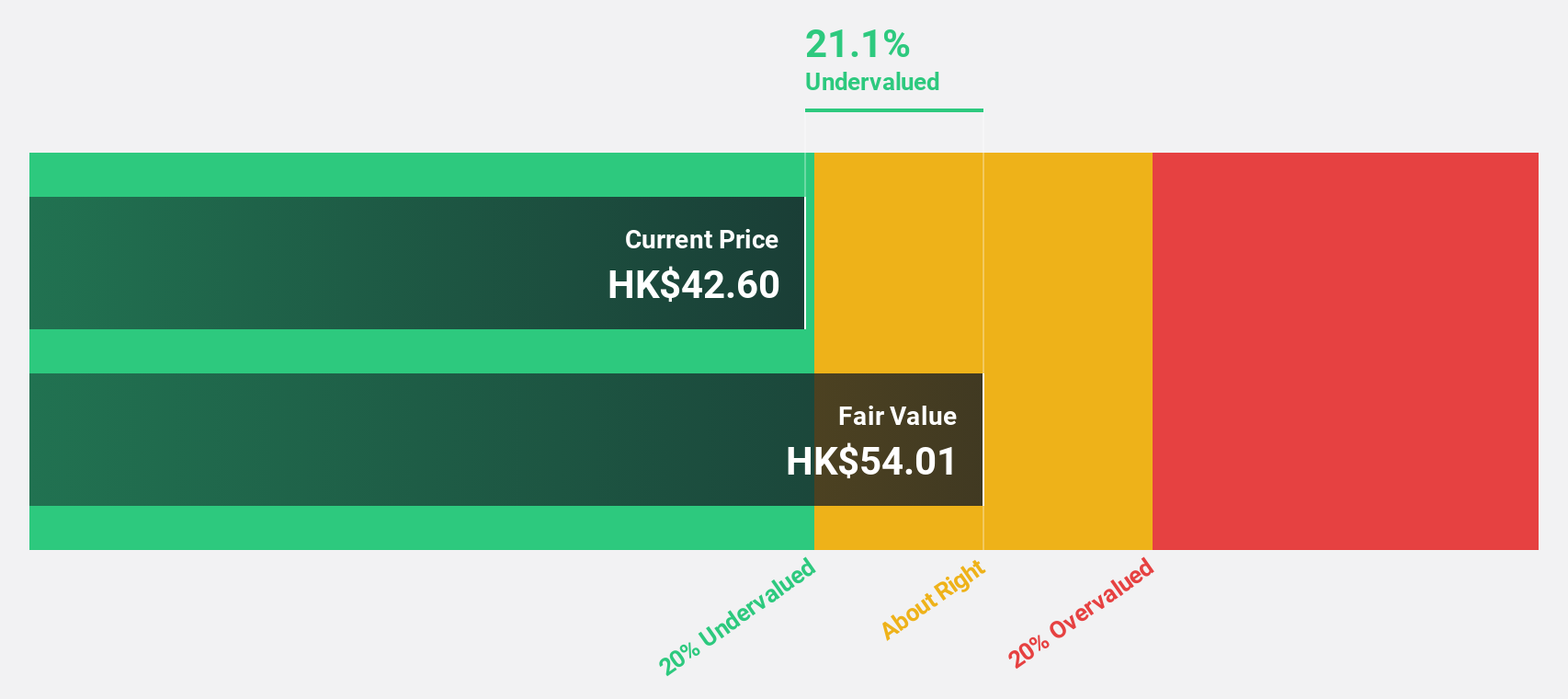

Swire Properties (SEHK:1972)

Overview: Swire Properties Limited, with a market cap of HK$92.15 billion, develops, owns, and operates mixed-use commercial properties in Hong Kong, Mainland China, the United States, and internationally through its subsidiaries.

Operations: Swire Properties Limited generates revenue from property investment (HK$14.39 billion), hotels (HK$945 million), and property trading (HK$119 million).

Estimated Discount To Fair Value: 15.4%

Swire Properties is trading at HK$15.78, below its estimated fair value of HK$18.66, indicating it may be undervalued based on cash flows. Recent share buybacks authorized up to 585 million shares could enhance net asset value and earnings per share. Despite a drop in net income from HK$2.22 billion to HK$1.80 billion for H1 2024, earnings are forecast to grow significantly by 25% annually over the next three years.

- The growth report we've compiled suggests that Swire Properties' future prospects could be on the up.

- Click here to discover the nuances of Swire Properties with our detailed financial health report.

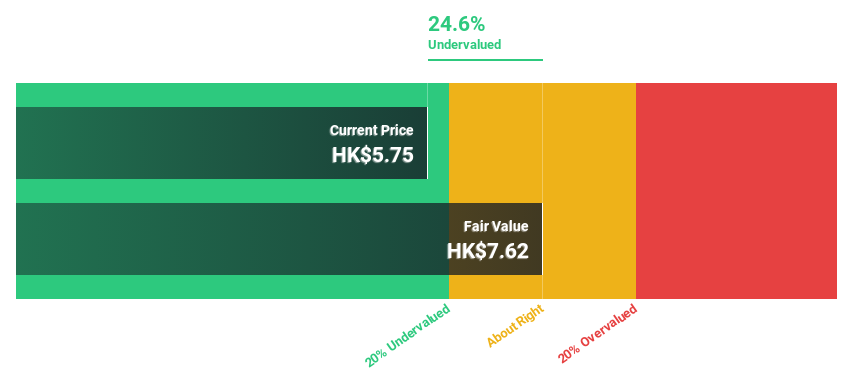

CIMC Enric Holdings (SEHK:3899)

Overview: CIMC Enric Holdings Limited offers transportation, storage, and processing equipment and services for the clean energy, chemicals, environmental, and liquid food sectors globally with a market cap of HK$13.59 billion.

Operations: The company's revenue segments are as follows: CN¥16.49 billion from Clean Energy, CN¥4.59 billion from Liquid Food, and CN¥3.31 billion from Chemical and Environmental sectors.

Estimated Discount To Fair Value: 13.9%

CIMC Enric Holdings is trading at HK$6.70, below its estimated fair value of HK$7.78, indicating it may be undervalued based on cash flows. Analysts forecast earnings to grow significantly by 20.9% annually over the next three years, outpacing the Hong Kong market's growth rate of 12%. Recent strategic alliances in hydrogen and LNG co-production projects underscore its commitment to sustainable development and could enhance future cash flows despite a slight dip in recent net income from CNY 568.67 million to CNY 486.14 million for H1 2024.

- In light of our recent growth report, it seems possible that CIMC Enric Holdings' financial performance will exceed current levels.

- Delve into the full analysis health report here for a deeper understanding of CIMC Enric Holdings.

Taking Advantage

- Investigate our full lineup of 36 Undervalued SEHK Stocks Based On Cash Flows right here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:1972

Swire Properties

Develops, owns, and operates mixed-use, primarily commercial properties in Hong Kong, Mainland China, the United States, and internationally.

Reasonable growth potential slight.