Advertisement

- Hong Kong

- /

- Construction

- /

- SEHK:1865

Pipeline Engineering Holdings (HKG:1865) Has Debt But No Earnings; Should You Worry?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Pipeline Engineering Holdings Limited (HKG:1865) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Pipeline Engineering Holdings

What Is Pipeline Engineering Holdings's Net Debt?

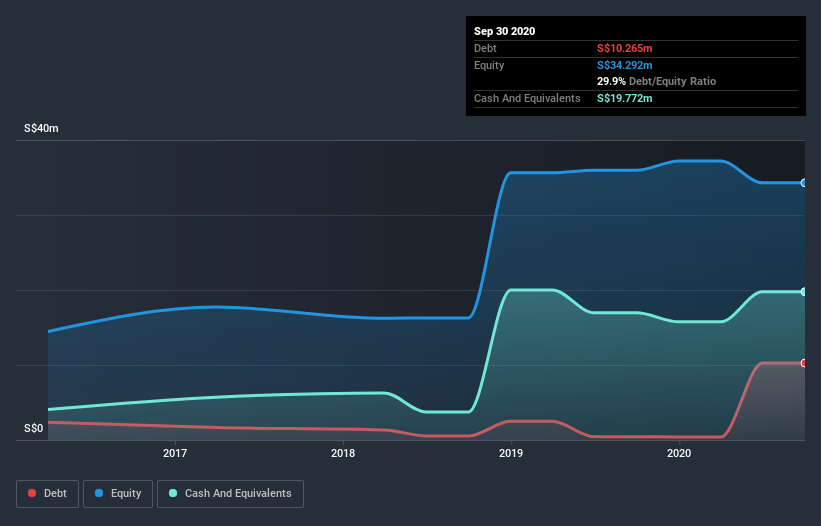

As you can see below, at the end of September 2020, Pipeline Engineering Holdings had S$10.3m of debt, up from S$444.0k a year ago. Click the image for more detail. But it also has S$19.8m in cash to offset that, meaning it has S$9.51m net cash.

How Strong Is Pipeline Engineering Holdings' Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Pipeline Engineering Holdings had liabilities of S$5.96m due within 12 months and liabilities of S$15.6m due beyond that. On the other hand, it had cash of S$19.8m and S$7.15m worth of receivables due within a year. So it can boast S$5.35m more liquid assets than total liabilities.

This surplus suggests that Pipeline Engineering Holdings has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Succinctly put, Pipeline Engineering Holdings boasts net cash, so it's fair to say it does not have a heavy debt load! The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Pipeline Engineering Holdings will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Pipeline Engineering Holdings had a loss before interest and tax, and actually shrunk its revenue by 24%, to S$22m. To be frank that doesn't bode well.

So How Risky Is Pipeline Engineering Holdings?

While Pipeline Engineering Holdings lost money on an earnings before interest and tax (EBIT) level, it actually generated positive free cash flow S$8.8m. So taking that on face value, and considering the net cash situation, we don't think that the stock is too risky in the near term. With mediocre revenue growth in the last year, we're don't find the investment opportunity particularly compelling. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Consider for instance, the ever-present spectre of investment risk. We've identified 4 warning signs with Pipeline Engineering Holdings (at least 1 which can't be ignored) , and understanding them should be part of your investment process.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you’re looking to trade Pipeline Engineering Holdings, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:1865

Pengo Holdings Group

An investment holding company, provides infrastructural pipeline construction and related engineering services for gas, water, telecommunications, and power industries in Singapore and the People’s Republic of China.

Excellent balance sheet with very low risk.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor