Advertisement

- Greece

- /

- Metals and Mining

- /

- ATSE:LEBEK

N. Leventeris (ATH:LEBEK) Has Debt But No Earnings; Should You Worry?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, N. Leventeris S.A. (ATH:LEBEK) does carry debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for N. Leventeris

How Much Debt Does N. Leventeris Carry?

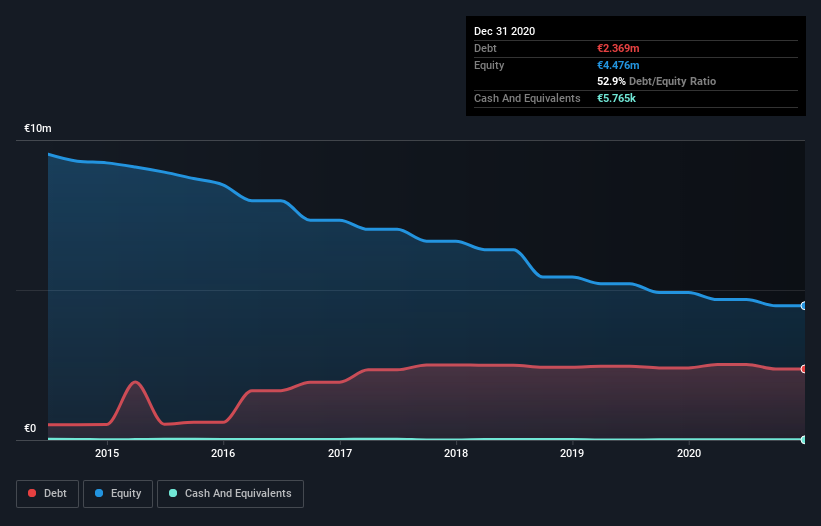

As you can see below, N. Leventeris had €2.37m of debt, at December 2020, which is about the same as the year before. You can click the chart for greater detail. And it doesn't have much cash, so its net debt is about the same.

How Strong Is N. Leventeris' Balance Sheet?

According to the last reported balance sheet, N. Leventeris had liabilities of €1.84m due within 12 months, and liabilities of €1.88m due beyond 12 months. Offsetting these obligations, it had cash of €5.8k as well as receivables valued at €277.7k due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by €3.43m.

This deficit casts a shadow over the €2.12m company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. At the end of the day, N. Leventeris would probably need a major re-capitalization if its creditors were to demand repayment. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since N. Leventeris will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year N. Leventeris wasn't profitable at an EBIT level, but managed to grow its revenue by 10%, to €1.3m. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

Caveat Emptor

Over the last twelve months N. Leventeris produced an earnings before interest and tax (EBIT) loss. Indeed, it lost a very considerable €354k at the EBIT level. Considering that alongside the liabilities mentioned above make us nervous about the company. We'd want to see some strong near-term improvements before getting too interested in the stock. Not least because it burned through €60k in negative free cash flow over the last year. So suffice it to say we consider the stock to be risky. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. We've identified 3 warning signs with N. Leventeris (at least 2 which make us uncomfortable) , and understanding them should be part of your investment process.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you’re looking to trade a wide range of investments, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if N. Leventeris might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ATSE:LEBEK

N. Leventeris

Engages in production, marketing, and sale of wires and cables in Greece and internationally.

Slight risk with worrying balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor