Advertisement

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Papoutsanis S.A. (ATH:PAP) does have debt on its balance sheet. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Papoutsanis's Net Debt?

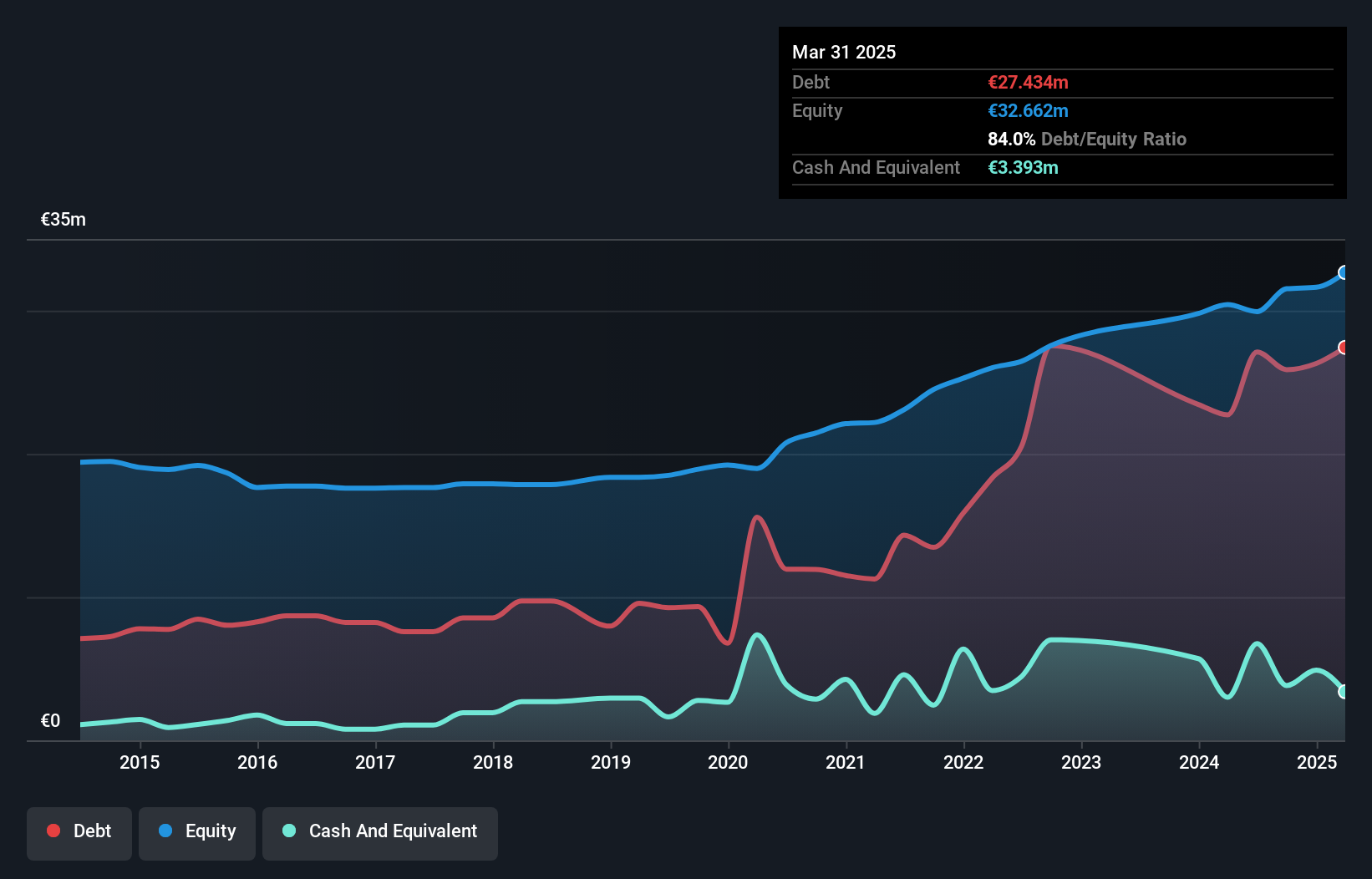

You can click the graphic below for the historical numbers, but it shows that as of March 2025 Papoutsanis had €27.4m of debt, an increase on €22.7m, over one year. However, it also had €3.39m in cash, and so its net debt is €24.0m.

How Healthy Is Papoutsanis' Balance Sheet?

The latest balance sheet data shows that Papoutsanis had liabilities of €23.6m due within a year, and liabilities of €29.8m falling due after that. Offsetting this, it had €3.39m in cash and €13.1m in receivables that were due within 12 months. So its liabilities total €36.9m more than the combination of its cash and short-term receivables.

Papoutsanis has a market capitalization of €81.6m, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

See our latest analysis for Papoutsanis

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Papoutsanis has a debt to EBITDA ratio of 2.5 and its EBIT covered its interest expense 5.5 times. This suggests that while the debt levels are significant, we'd stop short of calling them problematic. One way Papoutsanis could vanquish its debt would be if it stops borrowing more but continues to grow EBIT at around 17%, as it did over the last year. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Papoutsanis can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the last three years, Papoutsanis barely recorded positive free cash flow, in total. Some might say that's a concern, when it comes considering how easily it would be for it to down debt.

Our View

Papoutsanis's conversion of EBIT to free cash flow was a real negative on this analysis, although the other factors we considered cast it in a significantly better light. But on the bright side, its ability to to grow its EBIT isn't too shabby at all. Looking at all the angles mentioned above, it does seem to us that Papoutsanis is a somewhat risky investment as a result of its debt. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 2 warning signs with Papoutsanis (at least 1 which is significant) , and understanding them should be part of your investment process.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ATSE:PAP

Papoutsanis

Engages in the production and sale of soaps and liquid cosmetics in Greece.

Undervalued with solid track record.

Market Insights

Advertisement

Community Narratives

A Quality Compounder Marked Down on Overblown Fears

Fair Value US$120.72|59.6% undervalued

BA

Community Contributor

Wyndham Continues Global Expansion with 19% Ancillary Revenue Growth

Fair Value US$105.80|20.8% undervalued

ZW

Community Contributor