Advertisement

- United Kingdom

- /

- Software

- /

- AIM:TRCS

Tracsis plc (LON:TRCS) Shares Fly 27% But Investors Aren't Buying For Growth

Tracsis plc (LON:TRCS) shareholders would be excited to see that the share price has had a great month, posting a 27% gain and recovering from prior weakness. But the last month did very little to improve the 54% share price decline over the last year.

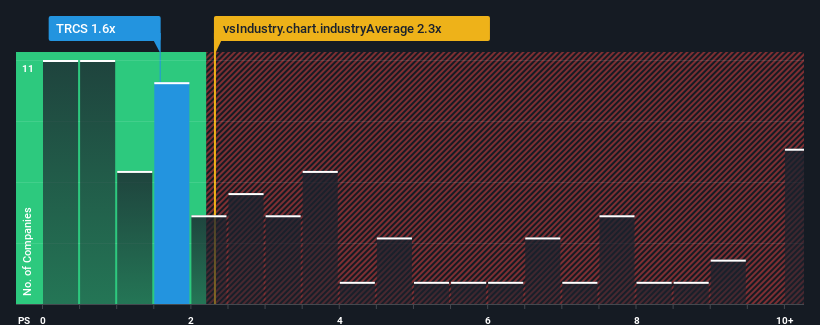

Although its price has surged higher, Tracsis may still be sending buy signals at present with its price-to-sales (or "P/S") ratio of 1.6x, considering almost half of all companies in the Software industry in the United Kingdom have P/S ratios greater than 2.3x and even P/S higher than 5x aren't out of the ordinary. However, the P/S might be low for a reason and it requires further investigation to determine if it's justified.

We've discovered 2 warning signs about Tracsis. View them for free.View our latest analysis for Tracsis

What Does Tracsis' Recent Performance Look Like?

Recent times haven't been great for Tracsis as its revenue has been rising slower than most other companies. It seems that many are expecting the uninspiring revenue performance to persist, which has repressed the growth of the P/S ratio. If you still like the company, you'd be hoping revenue doesn't get any worse and that you could pick up some stock while it's out of favour.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Tracsis.Do Revenue Forecasts Match The Low P/S Ratio?

In order to justify its P/S ratio, Tracsis would need to produce sluggish growth that's trailing the industry.

Taking a look back first, we see that there was hardly any revenue growth to speak of for the company over the past year. Although pleasingly revenue has lifted 41% in aggregate from three years ago, notwithstanding the last 12 months. Accordingly, shareholders will be pleased, but also have some questions to ponder about the last 12 months.

Looking ahead now, revenue is anticipated to climb by 0.6% during the coming year according to the three analysts following the company. That's shaping up to be materially lower than the 8.4% growth forecast for the broader industry.

In light of this, it's understandable that Tracsis' P/S sits below the majority of other companies. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Final Word

Despite Tracsis' share price climbing recently, its P/S still lags most other companies. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of Tracsis' analyst forecasts revealed that its inferior revenue outlook is contributing to its low P/S. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

It is also worth noting that we have found 2 warning signs for Tracsis (1 is potentially serious!) that you need to take into consideration.

If you're unsure about the strength of Tracsis' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Tracsis might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About AIM:TRCS

Tracsis

Provides software and hardware, data analytics/GIS services for the rail, traffic data, and transportation industries in the United Kingdom, Ireland, rest of Europe, Europe, North America, and internationally.

Very undervalued with flawless balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor