Advertisement

- United Kingdom

- /

- Software

- /

- LSE:PINE

UK Stocks With Estimated Discounts Between 12.1% And 46.5% Offering Intriguing Investment Opportunities

Simply Wall St

Reviewed by Simply Wall St

The UK stock market has been under pressure recently, with the FTSE 100 experiencing declines due to weak trade data from China and falling commodity prices. Amid these challenges, identifying undervalued stocks can be a strategic approach for investors seeking potential opportunities in the current economic landscape.

Top 10 Undervalued Stocks Based On Cash Flows In The United Kingdom

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Pinewood Technologies Group (LSE:PINE) | £4.195 | £7.83 | 46.5% |

| PageGroup (LSE:PAGE) | £2.29 | £4.43 | 48.3% |

| On the Beach Group (LSE:OTB) | £2.19 | £4.23 | 48.2% |

| Mincon Group (AIM:MCON) | £0.42 | £0.78 | 46.2% |

| Likewise Group (AIM:LIKE) | £0.276 | £0.52 | 47.4% |

| Hollywood Bowl Group (LSE:BOWL) | £2.52 | £4.87 | 48.2% |

| Gym Group (LSE:GYM) | £1.476 | £2.93 | 49.6% |

| Gooch & Housego (AIM:GHH) | £5.70 | £10.87 | 47.5% |

| Begbies Traynor Group (AIM:BEG) | £1.16 | £2.21 | 47.4% |

| Advanced Medical Solutions Group (AIM:AMS) | £2.20 | £4.37 | 49.7% |

We'll examine a selection from our screener results.

Brickability Group (AIM:BRCK)

Overview: Brickability Group Plc, with a market cap of £187.49 million, distributes specialist products and services to the construction industry in the UK through its Bricks and Building Materials, Importing, Distribution, and Contracting segments.

Operations: The company's revenue is derived from four segments: Bricks and Building Materials (£426.12 million), Contracting (£98.59 million), Importing (£69.90 million), and Distribution (£68.75 million).

Estimated Discount To Fair Value: 36.1%

Brickability Group is trading at £0.58, significantly below its estimated fair value of £0.91, suggesting it is undervalued based on discounted cash flow analysis. Despite a forecasted revenue growth of 4.8% annually, which lags behind the desired 20%, earnings are expected to grow significantly at 42.2% per year, outpacing the UK market's average growth rate. However, the company's profit margins have decreased from last year and its dividend coverage remains weak despite recent increases in payouts.

- Our earnings growth report unveils the potential for significant increases in Brickability Group's future results.

- Click here to discover the nuances of Brickability Group with our detailed financial health report.

DFS Furniture (LSE:DFS)

Overview: DFS Furniture plc designs, manufactures, delivers, installs, and retails upholstered furniture in the United Kingdom and the Republic of Ireland with a market cap of £348.34 million.

Operations: The company generates revenue primarily from its DFS segment (£804.60 million) and Sofology segment (£225.70 million).

Estimated Discount To Fair Value: 12.1%

DFS Furniture is trading at £1.51, below its estimated fair value of £1.72, indicating it is undervalued based on cash flow analysis. The company has returned to profitability with a net income of £24.2 million and earnings per share of £0.105 for the fiscal year 2025. While revenue growth is modest at 4.3% annually, earnings are expected to grow significantly at 27.1% per year, outpacing the UK market average growth rate of 14%.

- Insights from our recent growth report point to a promising forecast for DFS Furniture's business outlook.

- Click to explore a detailed breakdown of our findings in DFS Furniture's balance sheet health report.

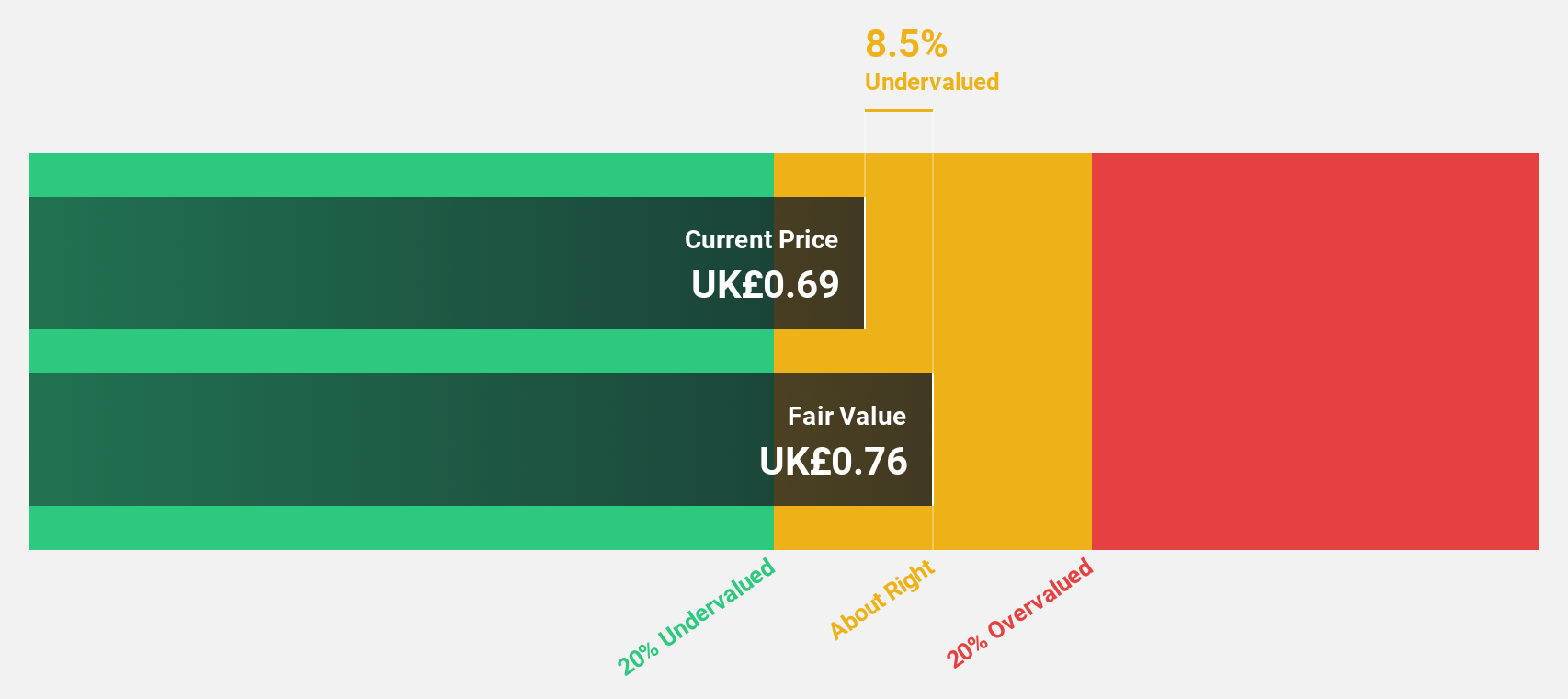

Pinewood Technologies Group (LSE:PINE)

Overview: Pinewood Technologies Group PLC is a cloud-based dealer management software provider operating in the UK, Europe, Africa, Asia, the Middle East, and internationally with a market cap of £421.75 million.

Operations: Pinewood Technologies Group PLC generates revenue through its cloud-based dealer management software solutions across the UK, Europe, Africa, Asia, the Middle East, and other international markets.

Estimated Discount To Fair Value: 46.5%

Pinewood Technologies Group is trading at £4.2, significantly below its estimated fair value of £7.83, highlighting its undervaluation based on cash flow analysis. Despite a recent net loss of £0.7 million for the half-year ending June 2025, earnings are forecast to grow substantially at 49.21% annually, surpassing the UK market average growth rate of 14%. Revenue is also expected to increase by 28.7% per year, indicating strong future cash flow potential despite current challenges.

- Our expertly prepared growth report on Pinewood Technologies Group implies its future financial outlook may be stronger than recent results.

- Take a closer look at Pinewood Technologies Group's balance sheet health here in our report.

Seize The Opportunity

- Take a closer look at our Undervalued UK Stocks Based On Cash Flows list of 54 companies by clicking here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:PINE

Pinewood Technologies Group

Operates as a cloud-based dealer management software provider in the United Kingdom, rest of Europe, Africa, Asia, the Middle East, and internationally.

Flawless balance sheet with high growth potential.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor